United States

Banks face many challenges from a slower economy and tighter financial conditions, which offset benefits from rising rates and higher net interest income. It is likely that things will get worse, a sentiment supported by many banking executives. However, negative expectations have already been priced in. We will maintain our overweight for now but will fade this position after a bounce in the next bear market rally. The long-term outlook is negative. We prefer Regional Banks to Diversified Banks.

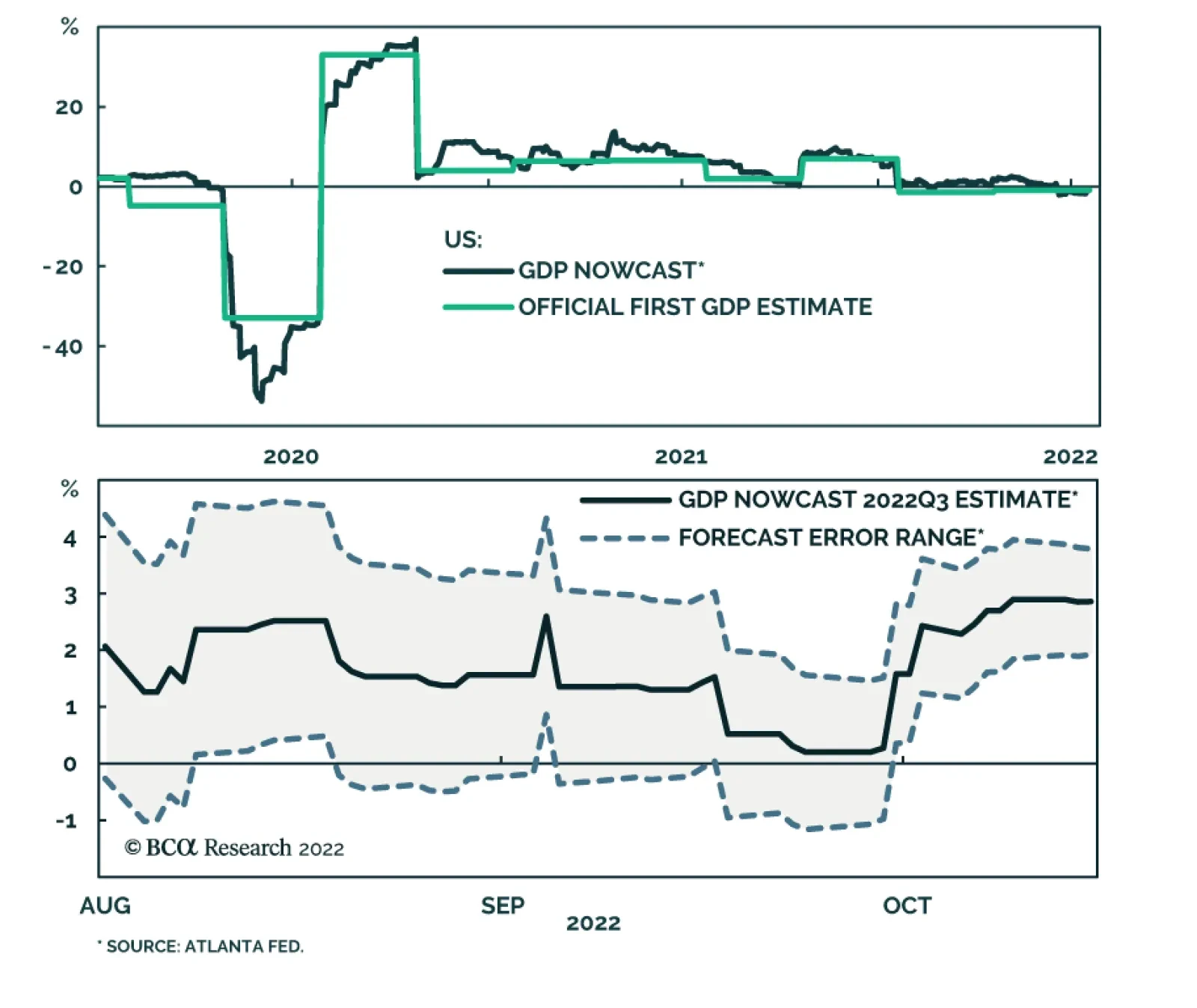

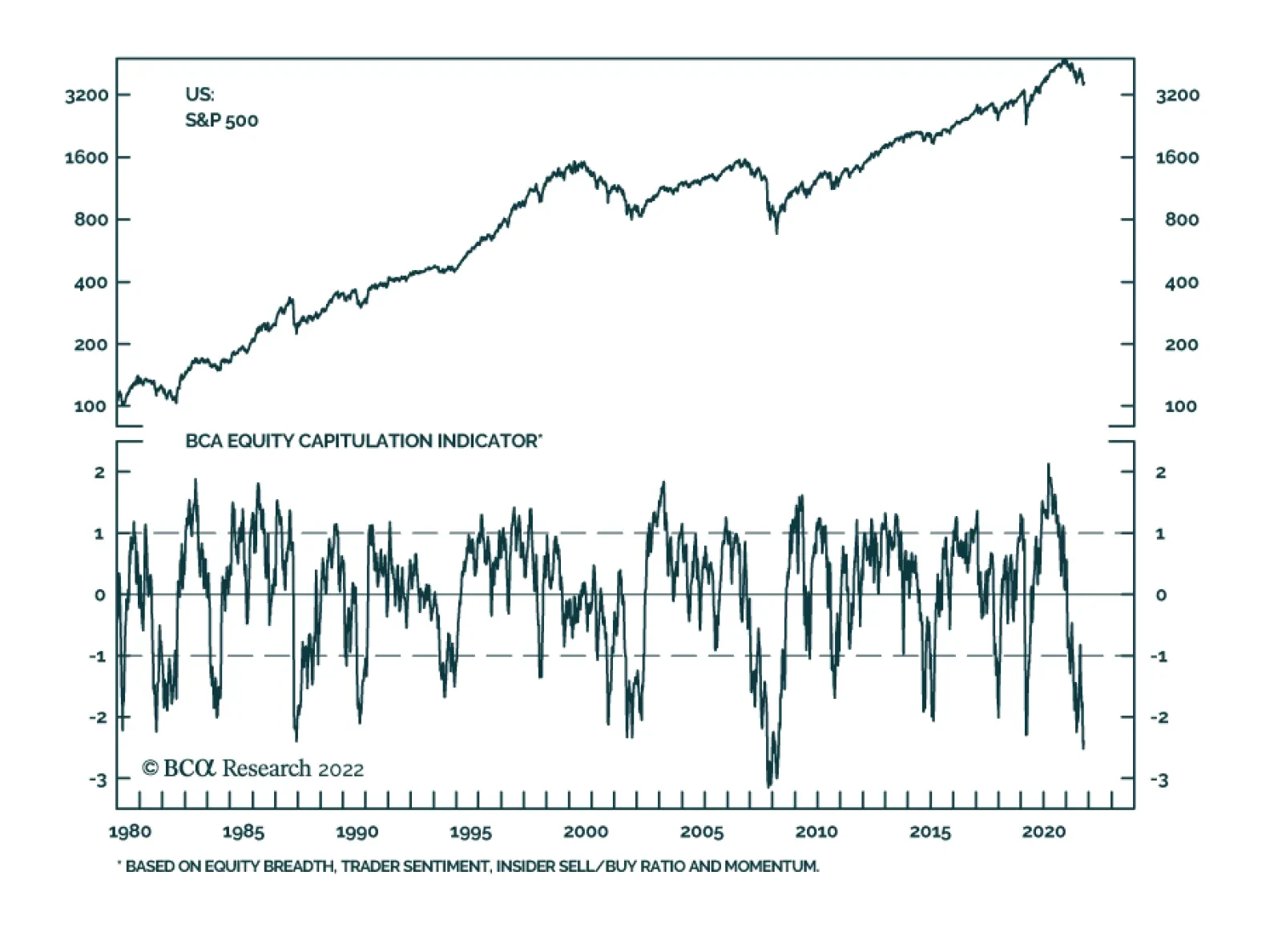

The September CPI report was disappointing, but we still see several signs pointing to a rapid decline in inflation. Our constructive near-term view on stocks and the economy remains intact.

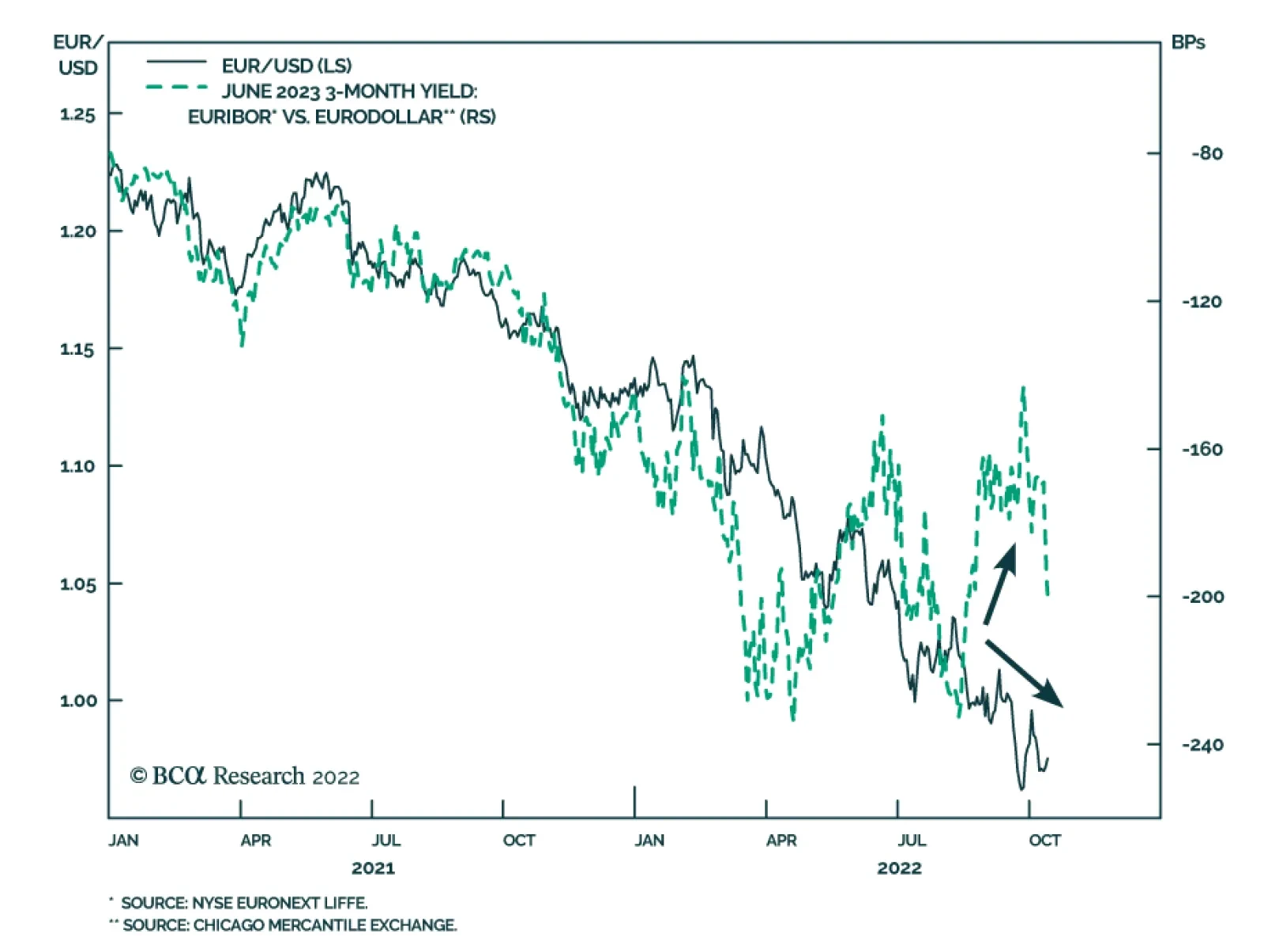

The ECB will continue to lift rates due to sticky inflation and a tight labor market. Will it be enough to push long-term German yields higher?

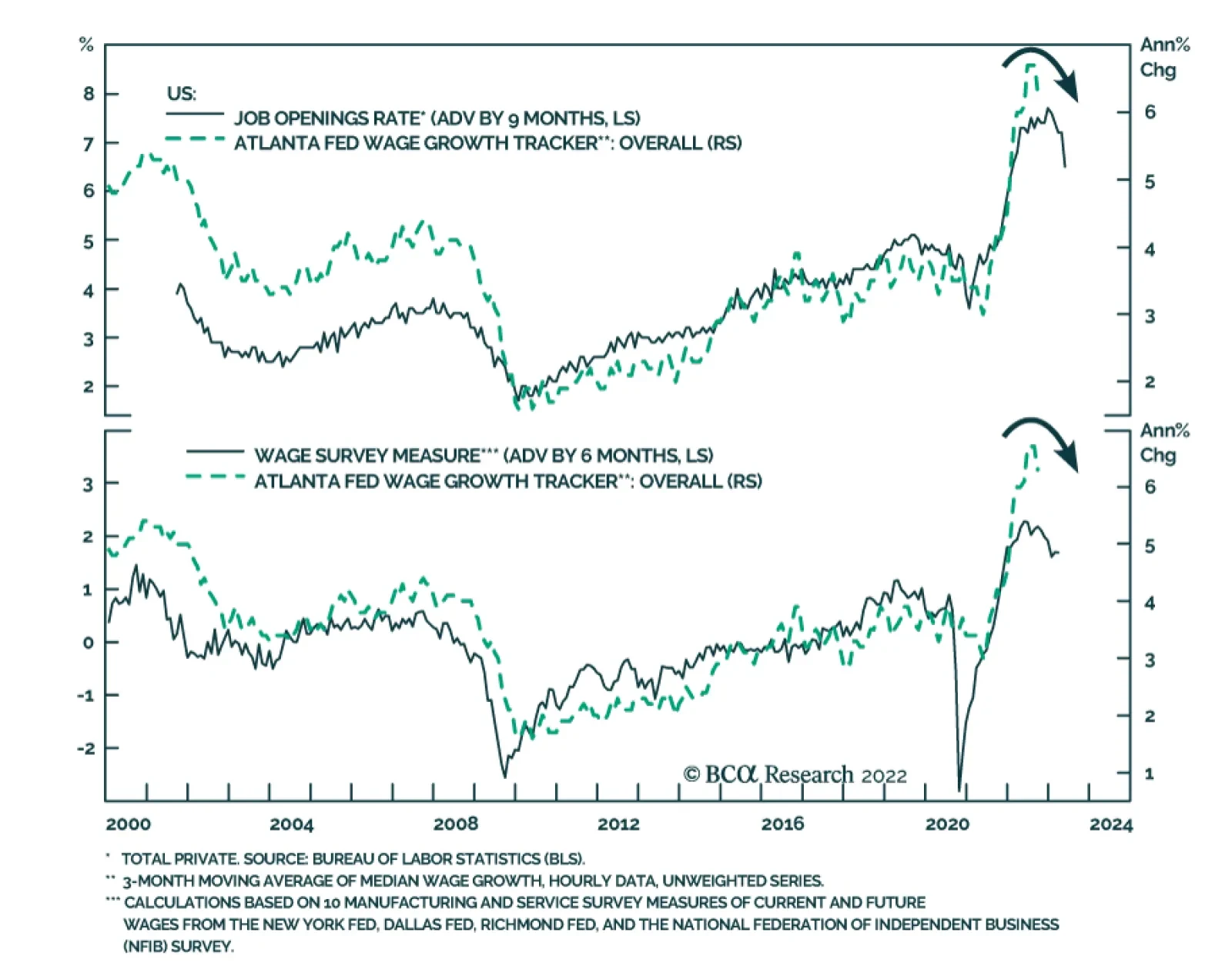

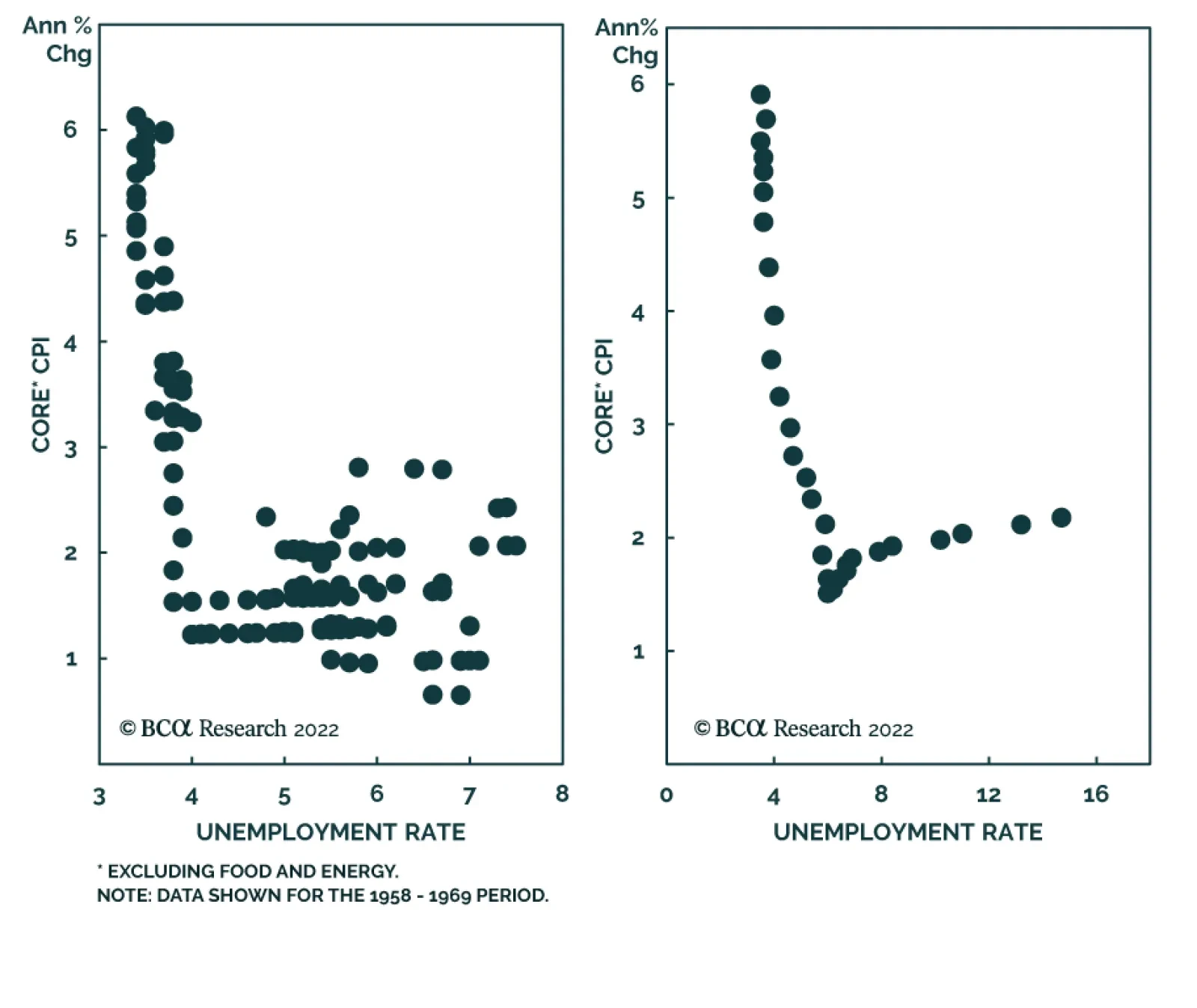

The kinked Phillips curve not only explains why inflation surged last year but makes a number of surprising predictions, chief of which is that inflation could fall significantly over the coming months without a major increase in the unemployment rate. In the near term, that is bullish for stocks.