United States

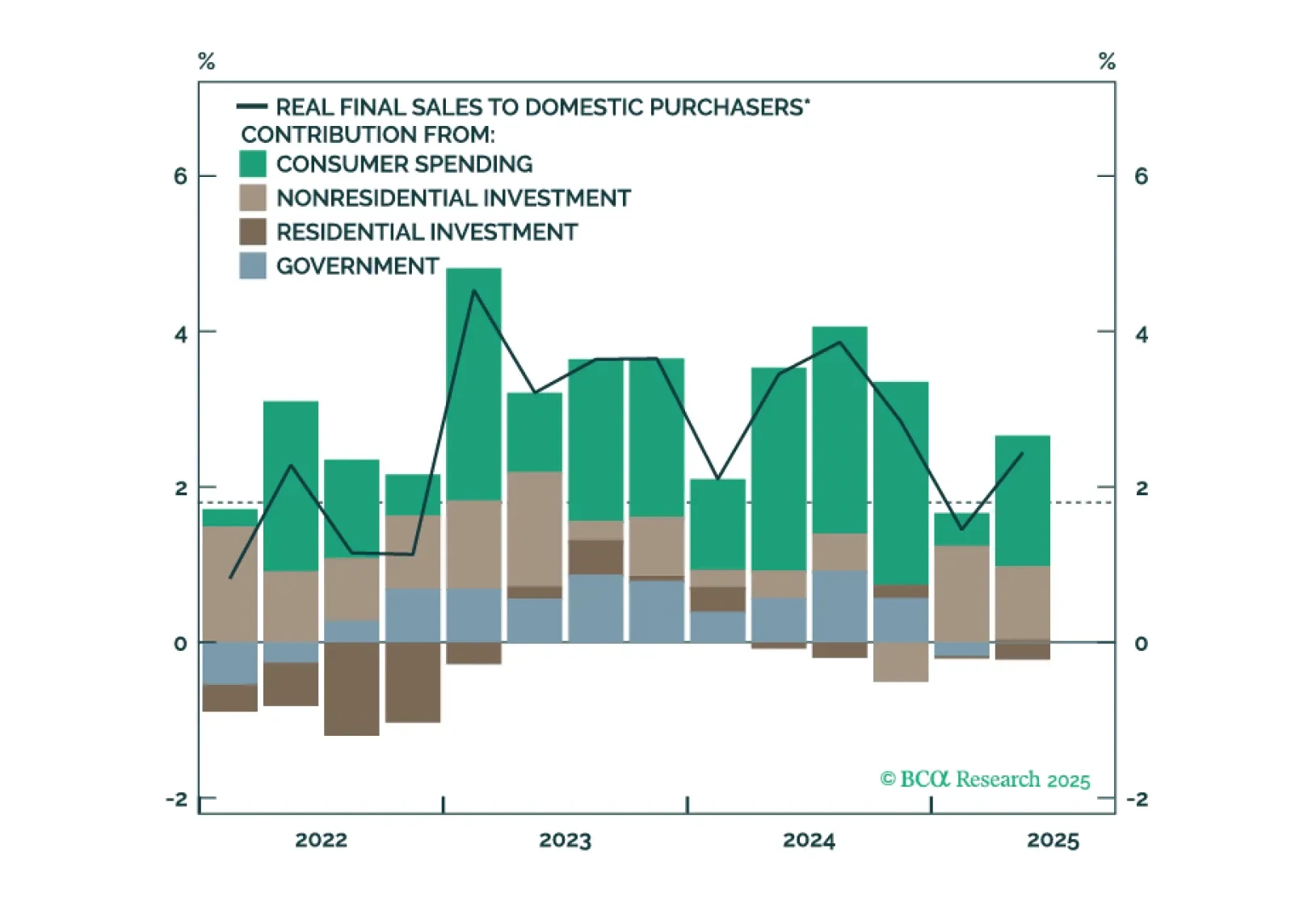

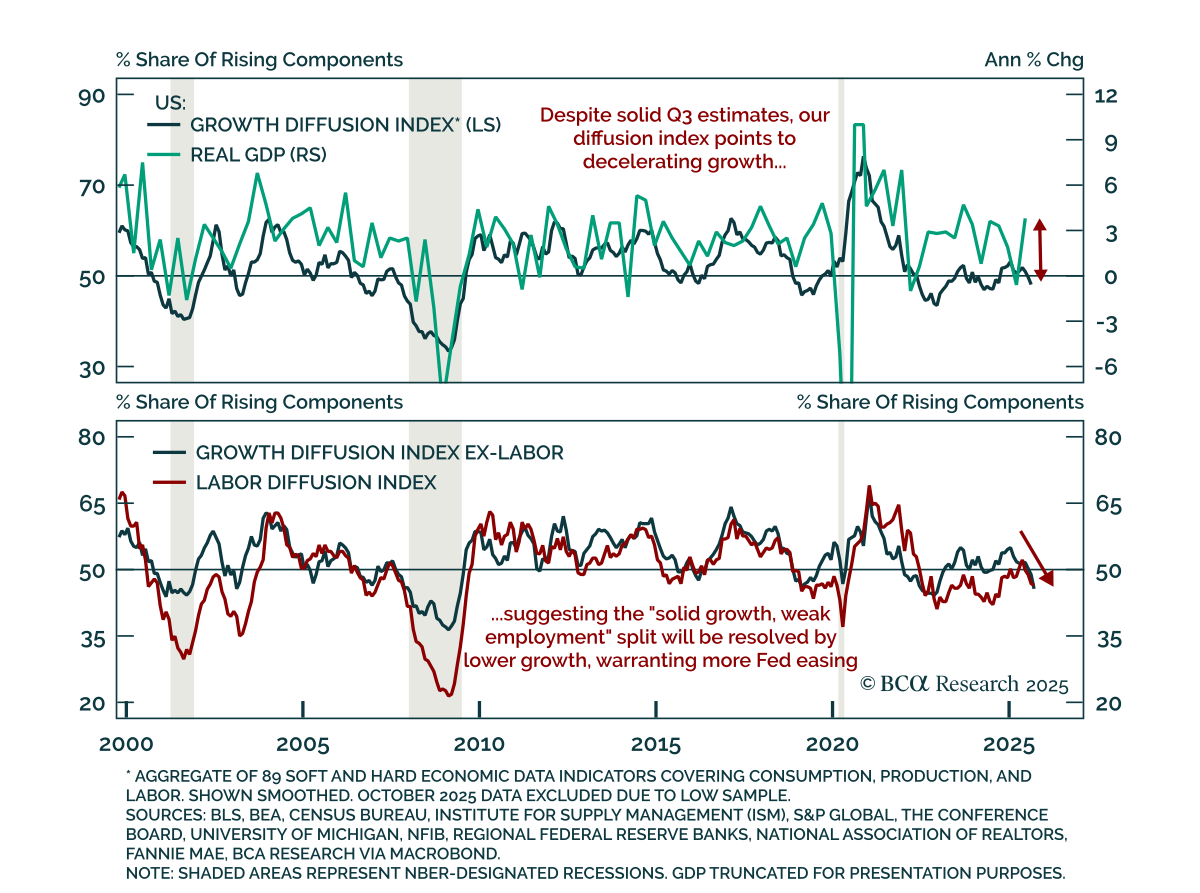

The Fed is poised to deliver a 25-basis-point rate cut this month, but a follow-up rate cut in December will depend on how the divergence between strong consumer spending and weak employment growth is resolved.

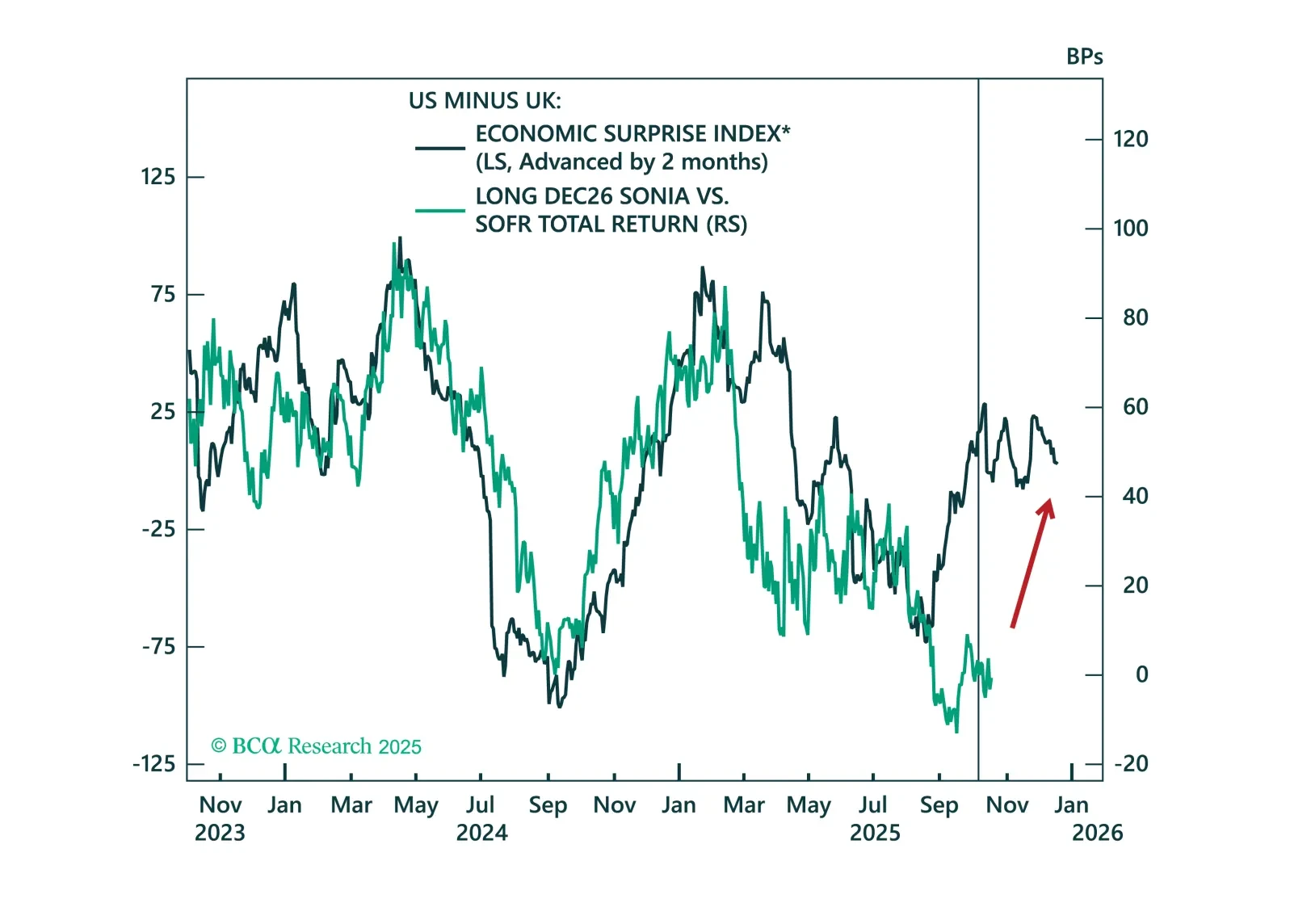

Same policy rate, very different expectations. We break down why policy convergence between the Fed and BoE is THE fixed income trade for year-end.

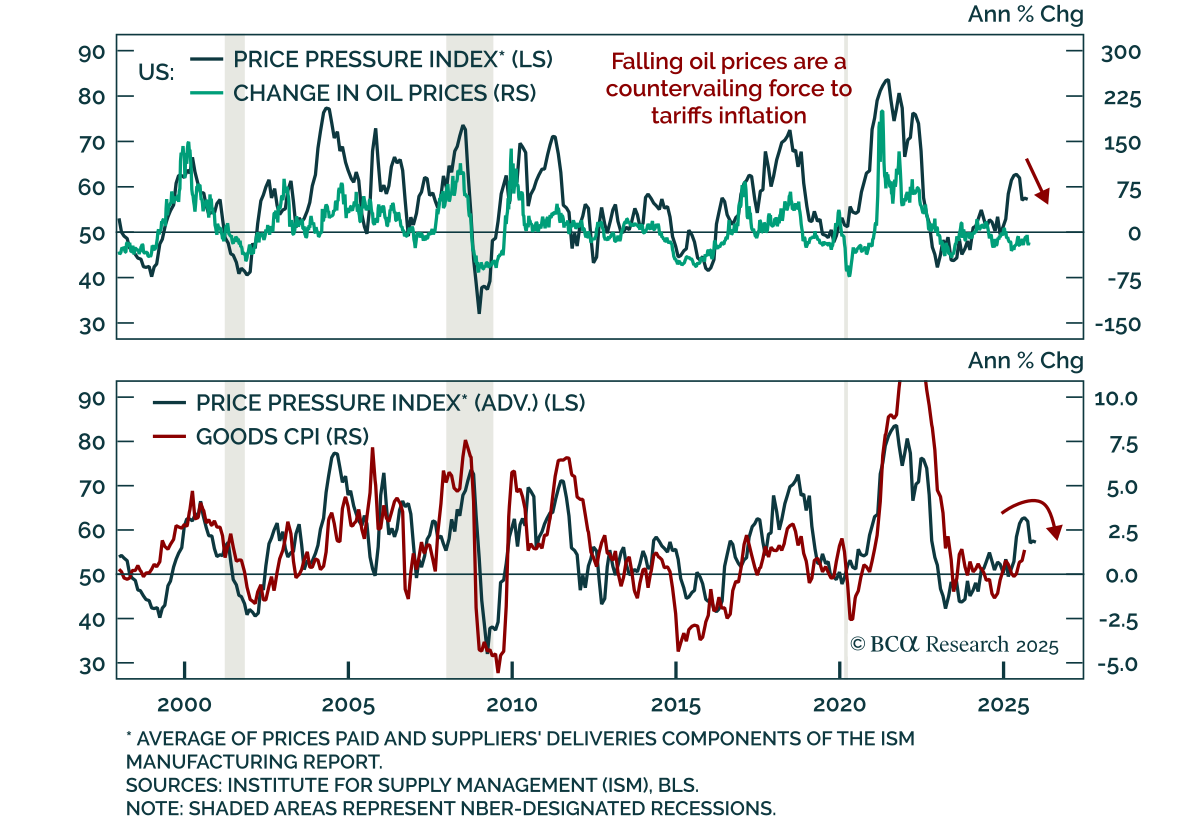

Falling oil prices are countering tariff-driven inflation which, along with a weakening labor market, is reinforcing a long duration stance. Brent crude broke below the $65/bbl support level held since June and WTI is now down 16% from a year ago. Falling oil…

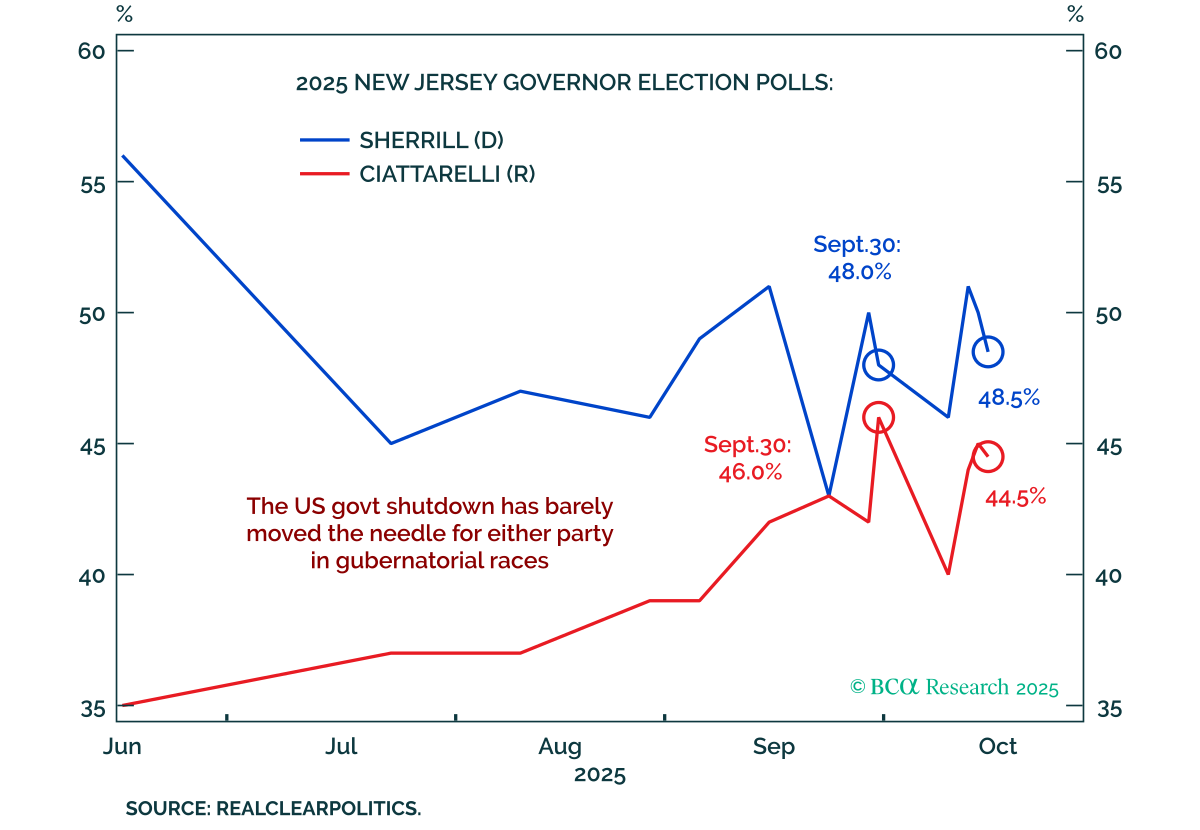

The shutdown can continue into November; only when the off-year elections and/or national opinion polls put more pressure on one or both parties will compromise start to come together to reopen the government. The US federal government shutdown continued for…

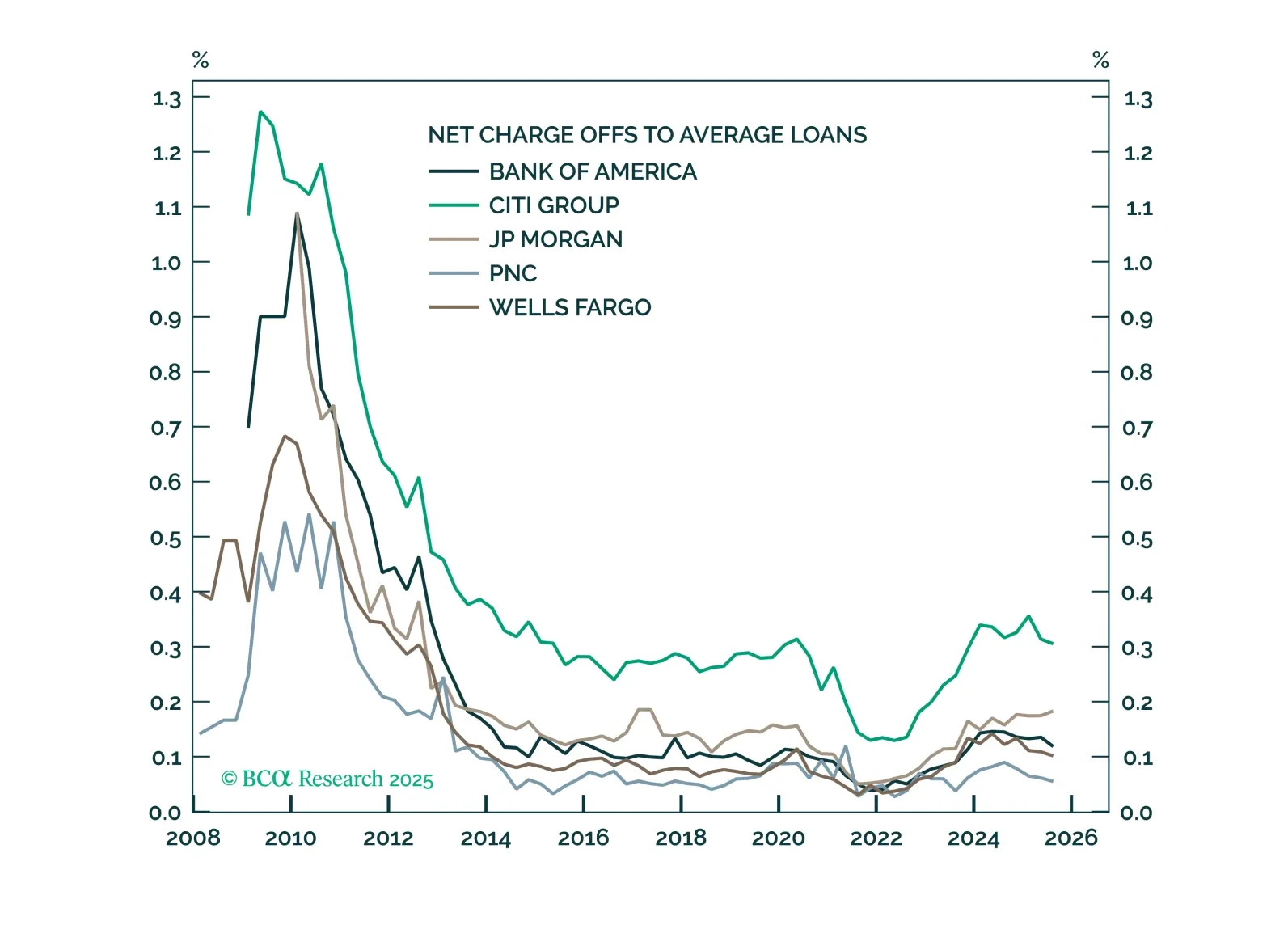

Strong results and constructive commentary from the US’s largest banks are encouraging: Consumers remain in solid shape, and the macro backdrop continues to favor equities. The outlook for the largest banks is positive, and they are unlikely to be affected by isolated credit events.

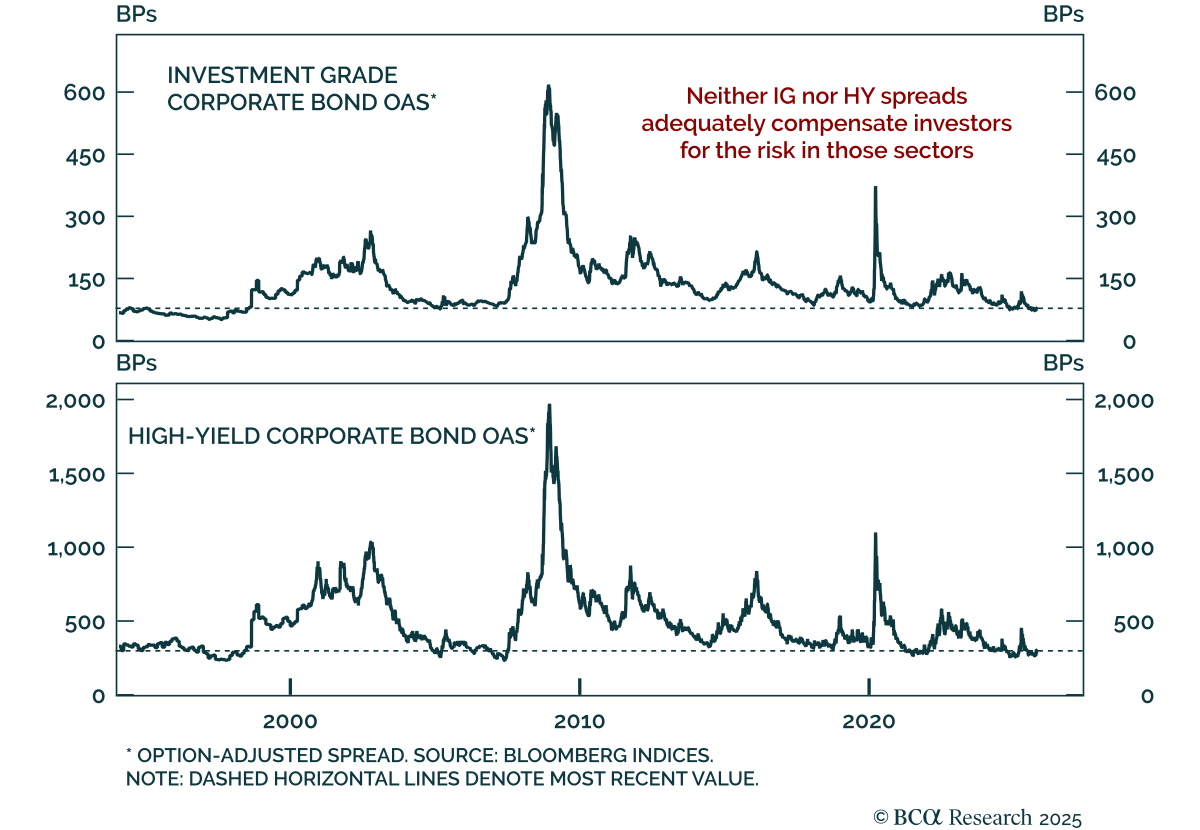

Our US Bond strategists find that neither IG nor HY spreads adequately compensate investors for risk, though the Ba credit tier offers the best relative trade-off. Expected excess returns across corporate credit are near multi-decade lows, with spreads for…

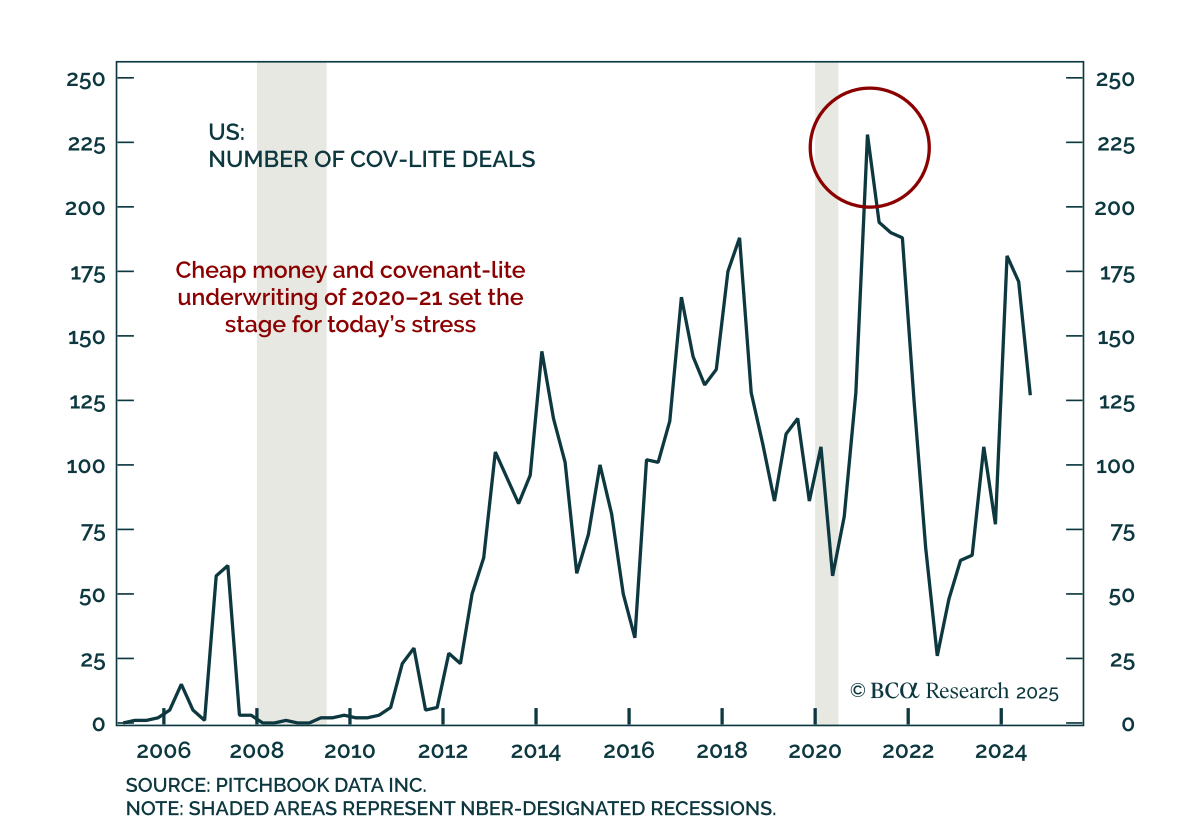

The unwind of 2020–21 froth is stressing floating-rate credit, with weak structures now meeting tighter funding. Our Chart Of The Week comes from Brian Payne, Chief Strategist for our Private Markets & Alternatives (PMA) service. Following…

We expect the divergence between resilient growth and weakening employment to be resolved by lower growth estimates, supporting long duration and steepeners. Economic activity and employment usually move together in a circular relationship: spending drives…

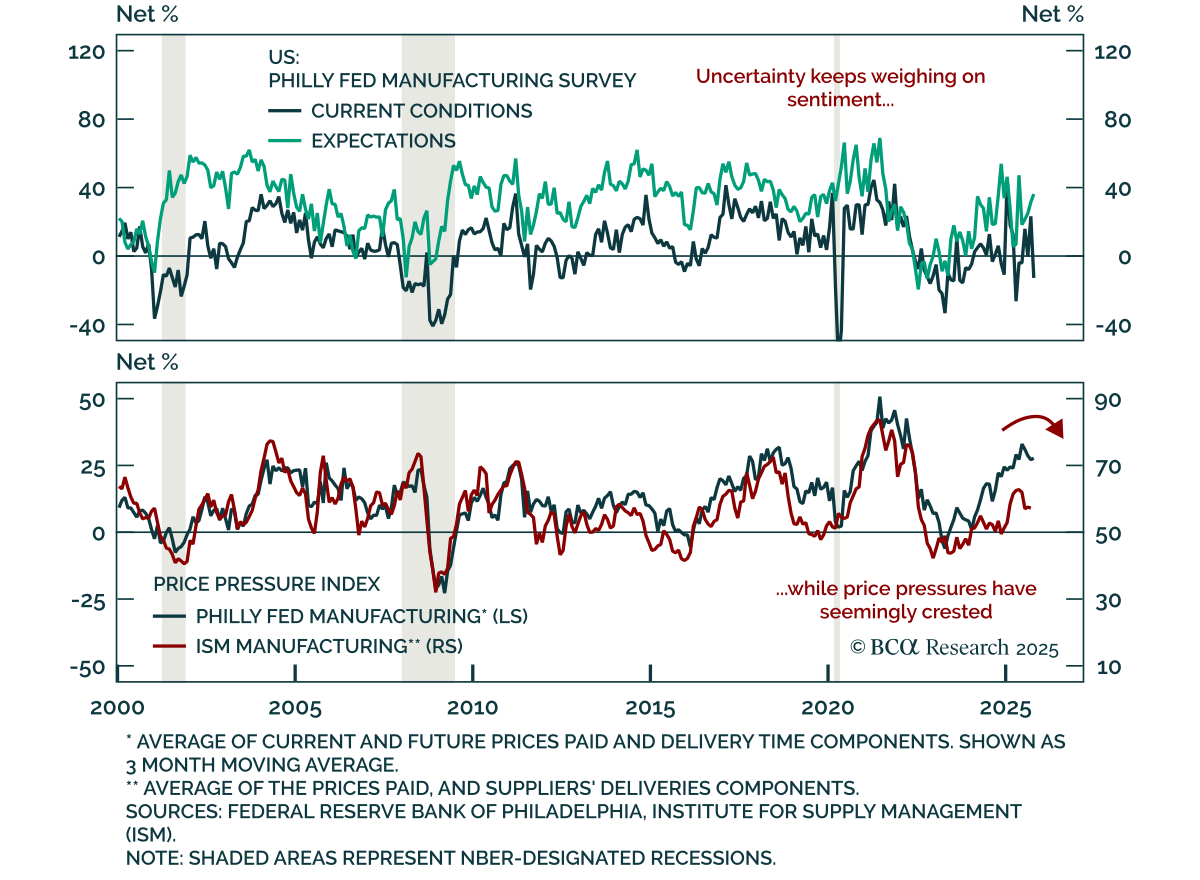

The October Philadelphia Fed manufacturing survey was mixed, showing weak headline data but steadier underlying components. The headline index fell to -12.8 from 23.2, the lowest level since April 2025. Underlying details were not as dire: shipments moderated…

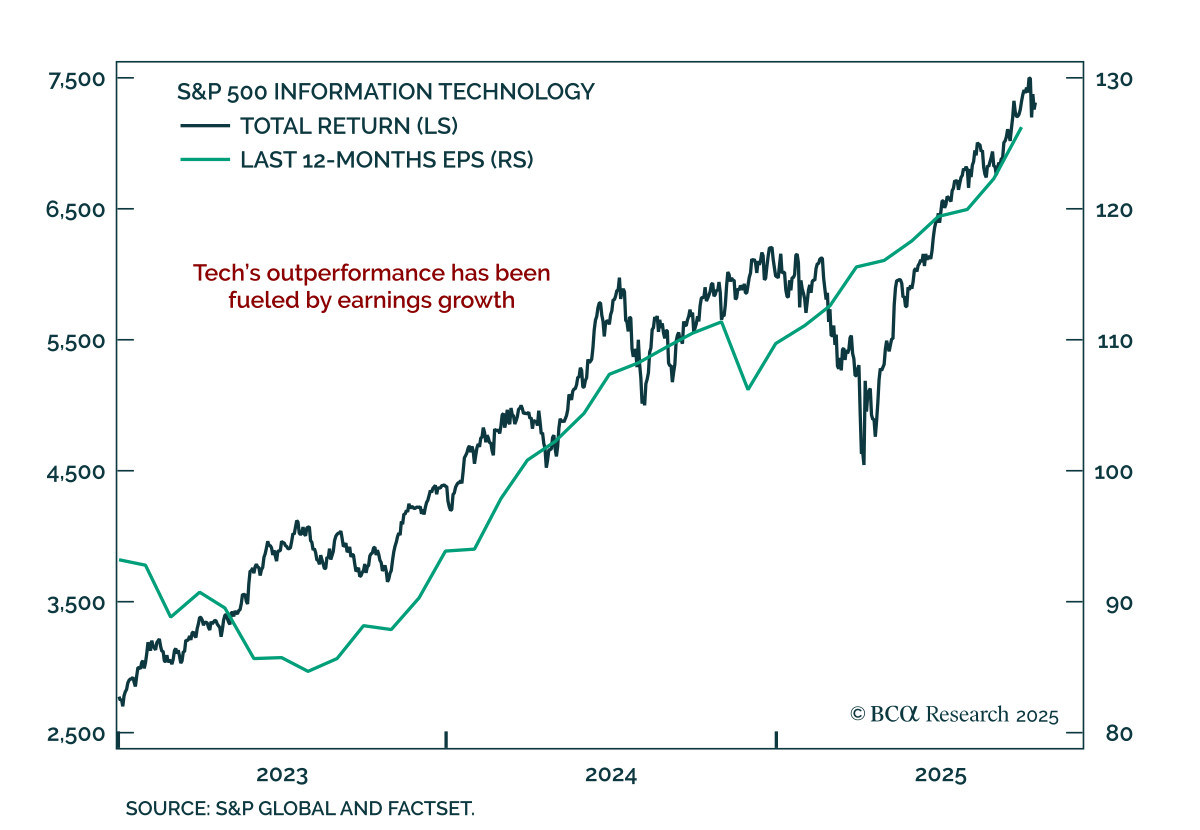

Our US Equity strategists see further room for the bull market to run, supported by solid GenAI-driven earnings growth, though a period of consolidation is likely. Broad adoption and monetization of GenAI, coupled with falling inference costs, should validate…