United States

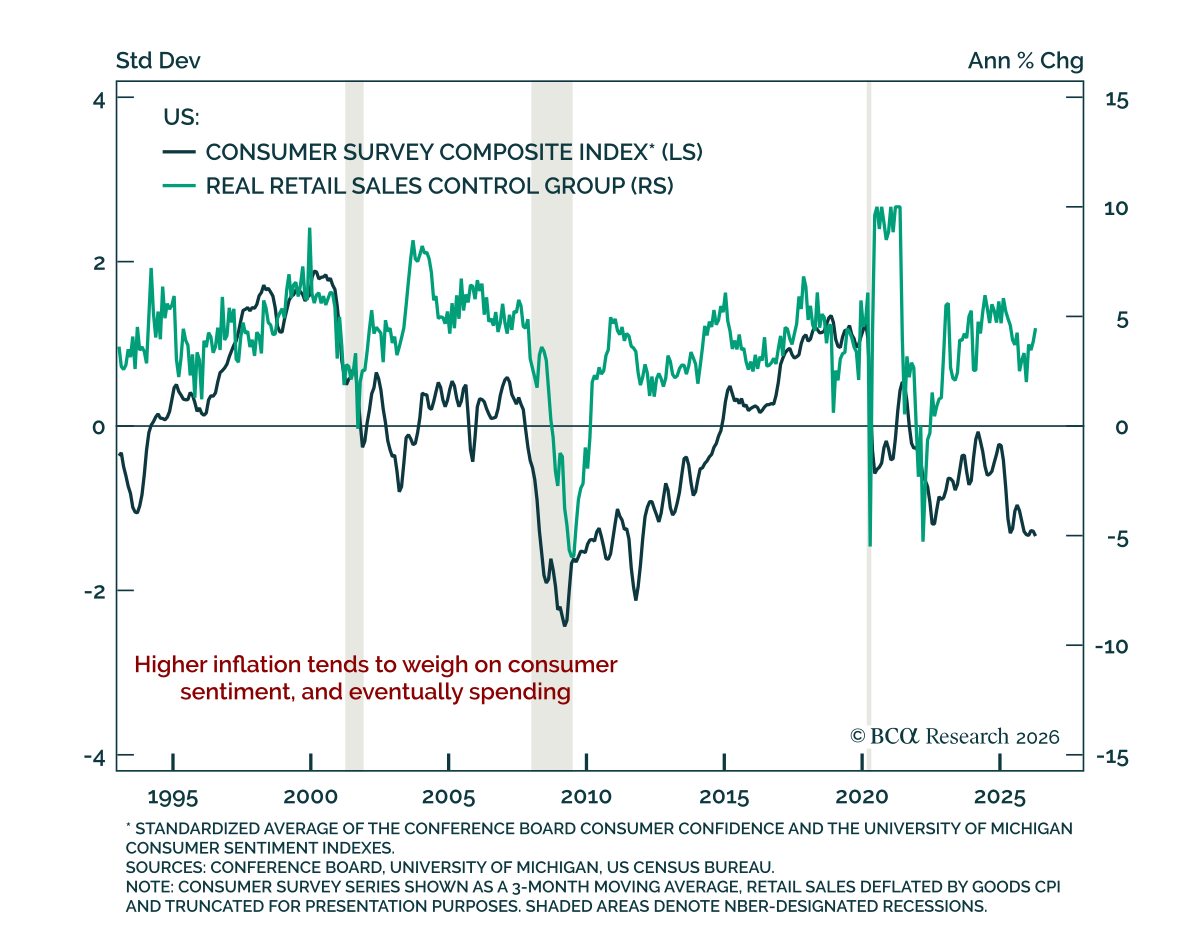

April US retail sales were roughly in line with estimates, but real spending likely stayed flat-to-negative. Headline sales slowed to 0.5% m/m from 1.6% a month prior. The core measure, which excludes autos and gas, and the control group, which feeds into…

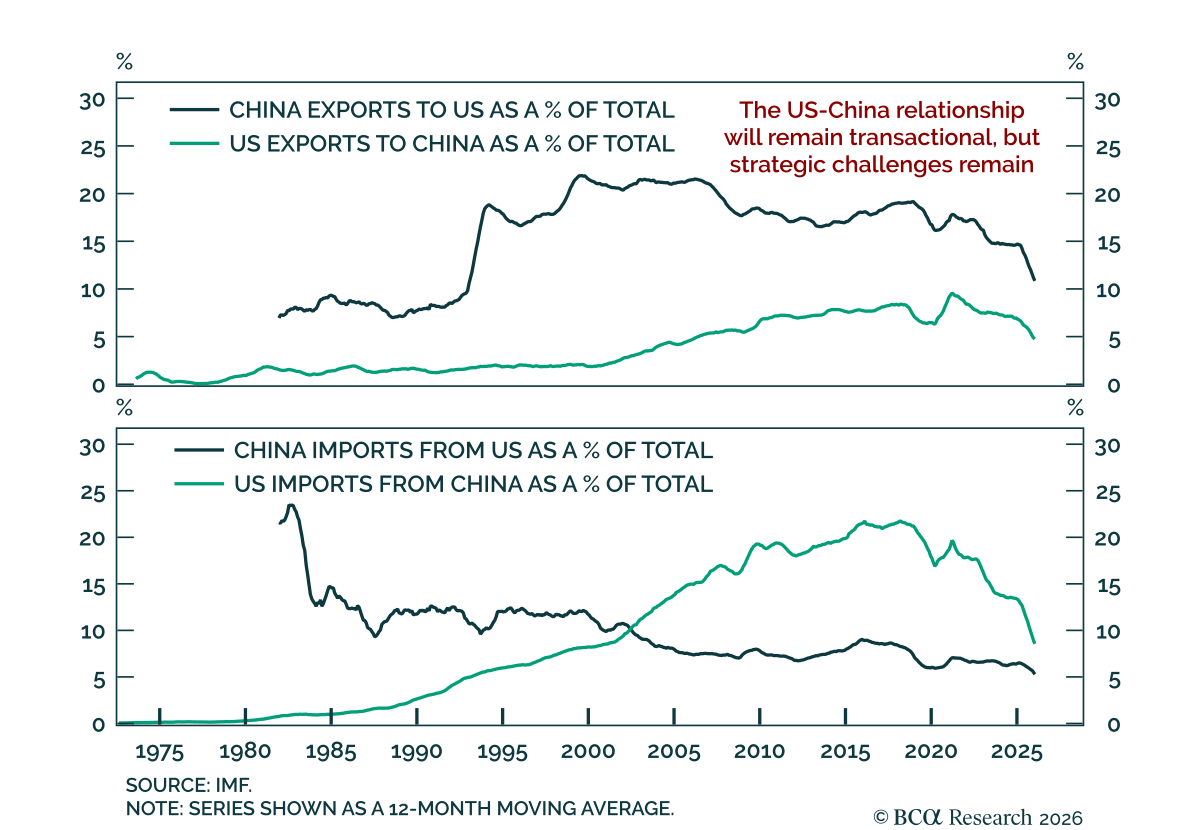

The Trump-Xi meeting was modestly positive, but it remained short on concrete commitments and did not amount to a strategic reset. Both sides still found room for limited trade de-escalation. President Trump may have lacked domestic and international leeway,…

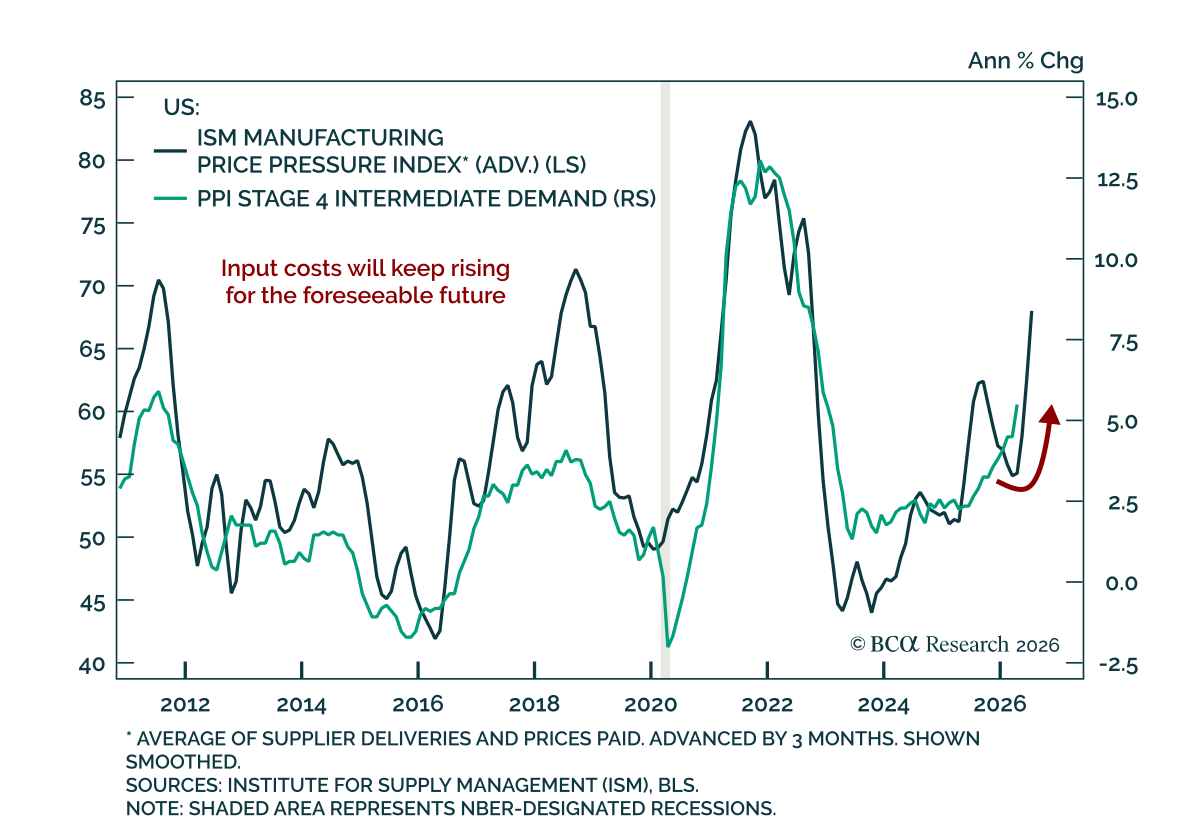

April PPI was hotter than expected, reinforcing the inflation message from CPI rather than changing it. Headline PPI for final demand rose 1.4% m/m, up from an upwardly revised 0.7% in March. The core measure, which excludes food, energy, and trade, rose 0.6%…

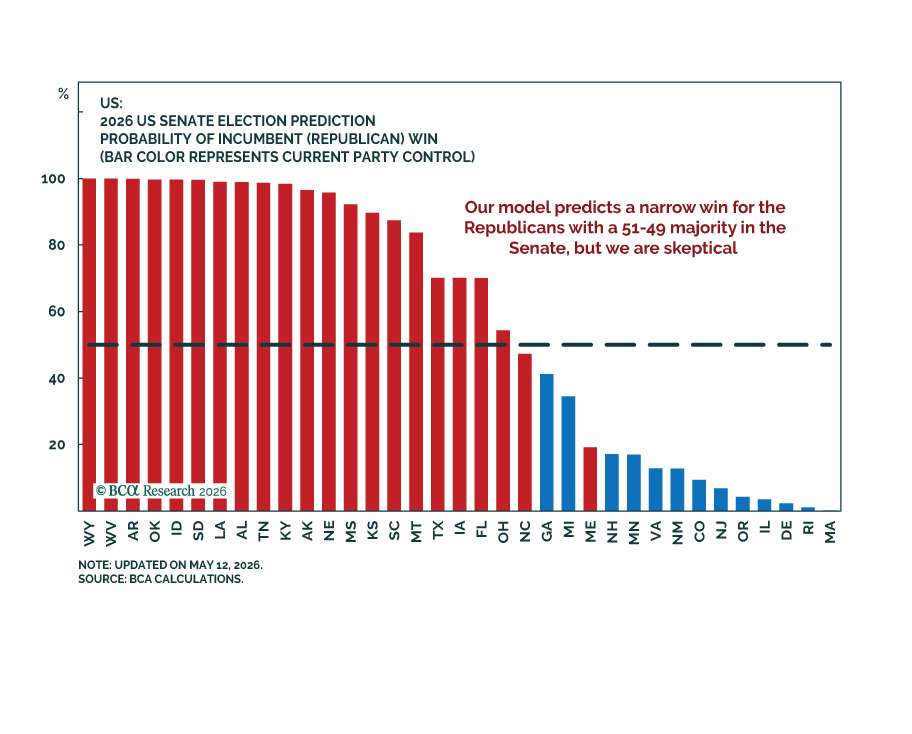

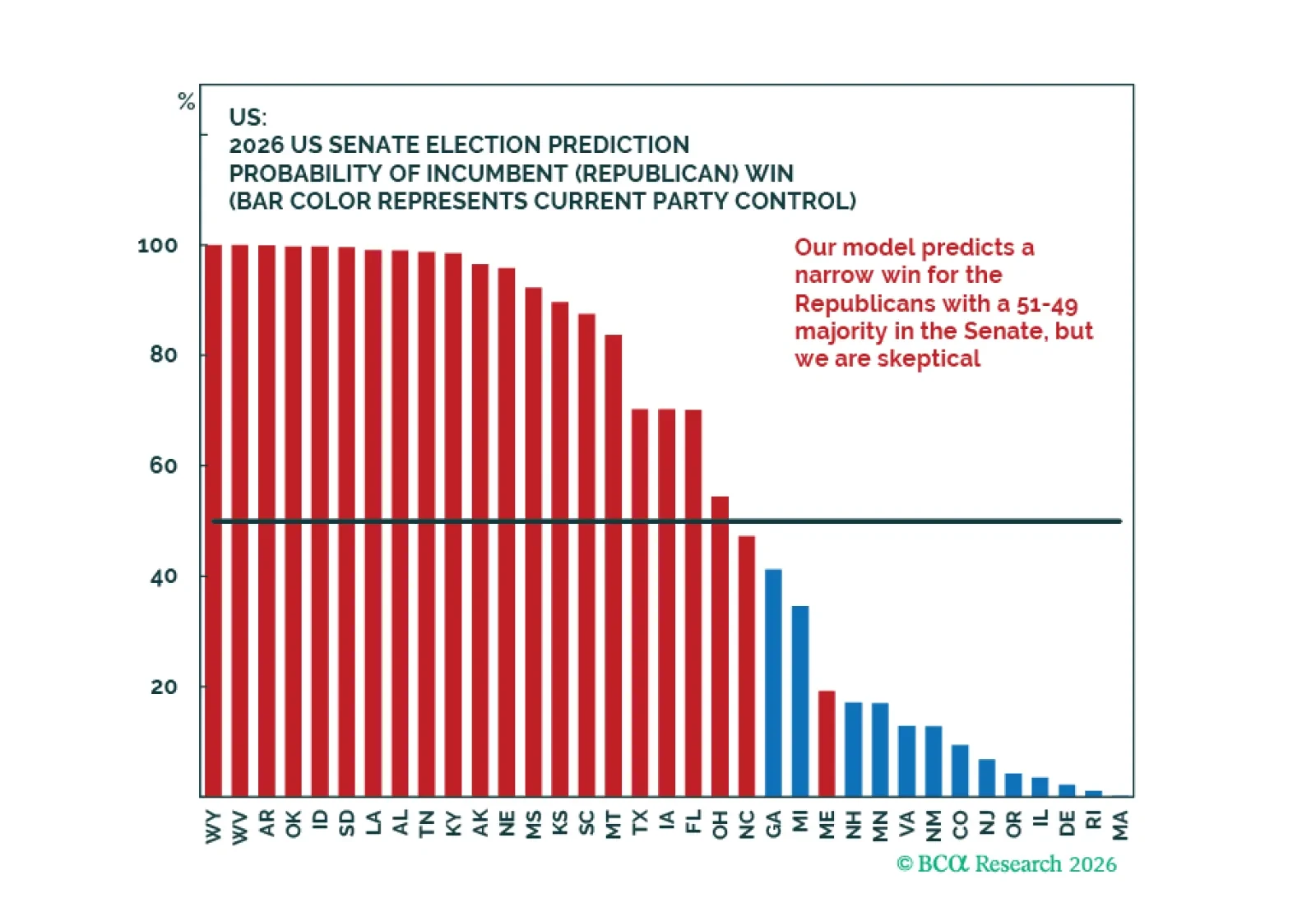

Our US Political and Geopolitical strategists expect Democrats to win the Senate in the 2026 midterms, despite an electoral map favorable to Republicans. While their quantitative model projects a narrow 51-49 Republican majority, our colleagues are skeptical.…

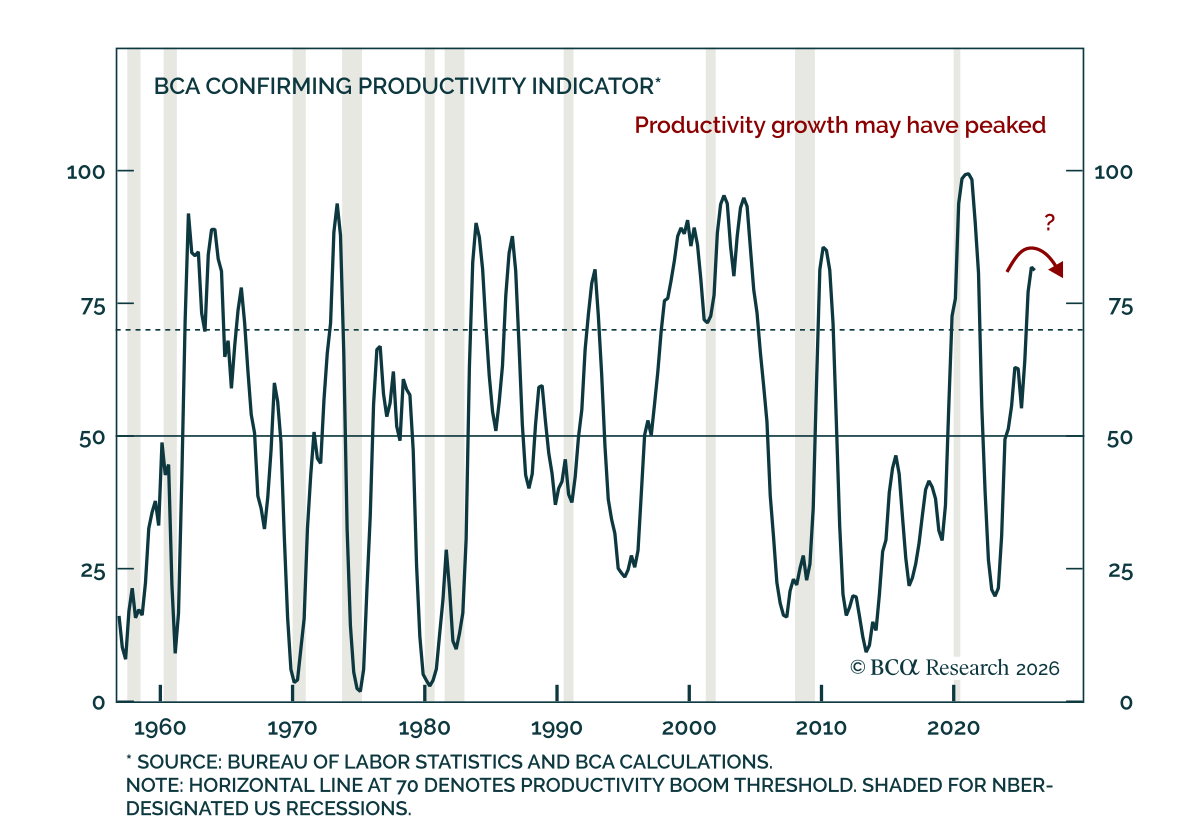

Q1 productivity data do not support the case for a broad, AI-driven productivity boom. We noted last week that US productivity growth in Q1 was lackluster. Our BCA Confirming Productivity Indicator, available on BCA’s new Artificial Intelligence Dashboard,…

Democrats are likely to win big in this year's midterm elections. Our new quant model still slightly favors Republicans for the Senate, but we expect the oil shock to deliver surprise Democratic victories.

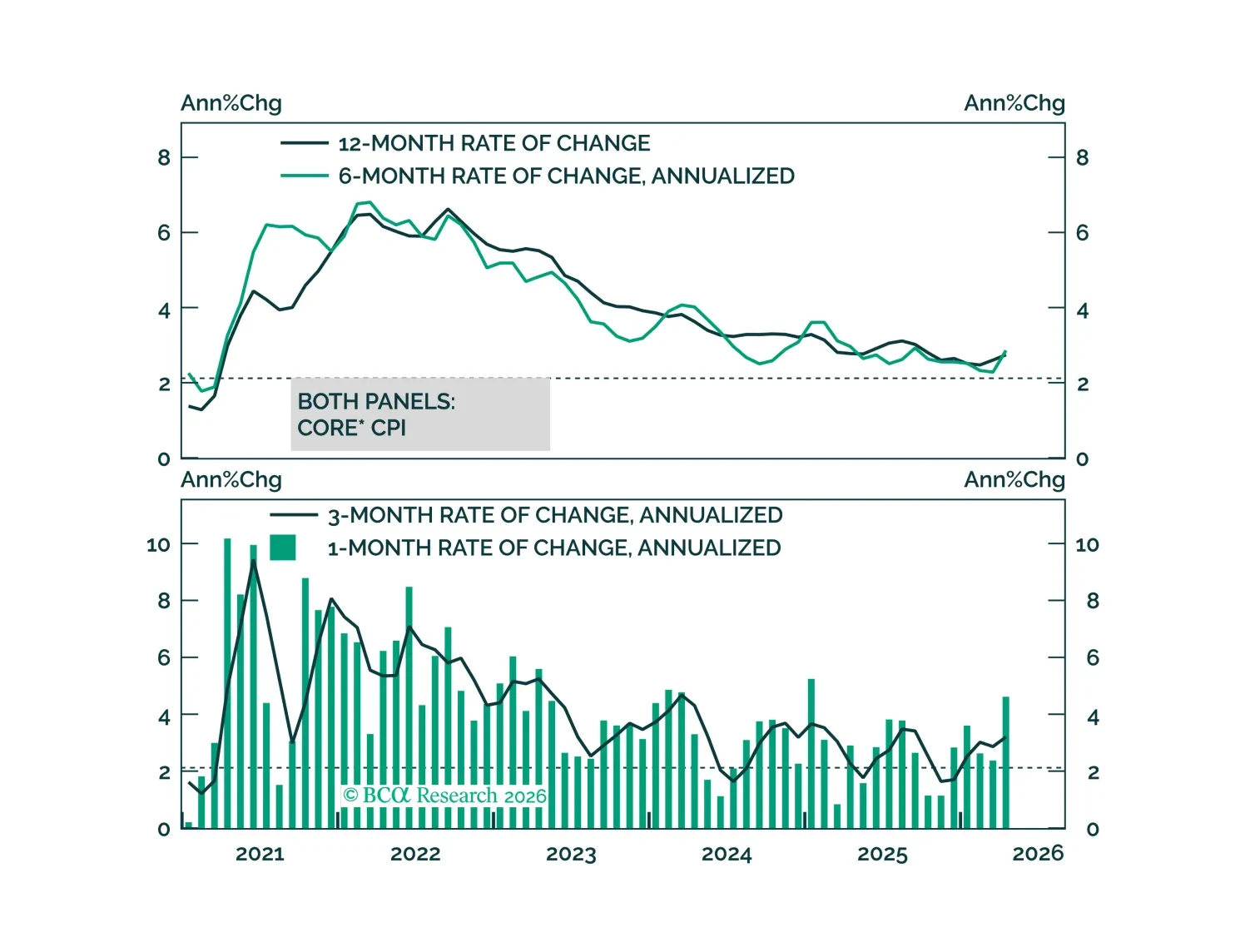

US April CPI was hotter than expected, keeping the Fed on hold as inflation risks remain tilted higher. Headline CPI rose 0.6% m/m and core 0.4%. While headline monthly inflation was below the prior month’s 0.9%, it remains too high to be consistent with the…

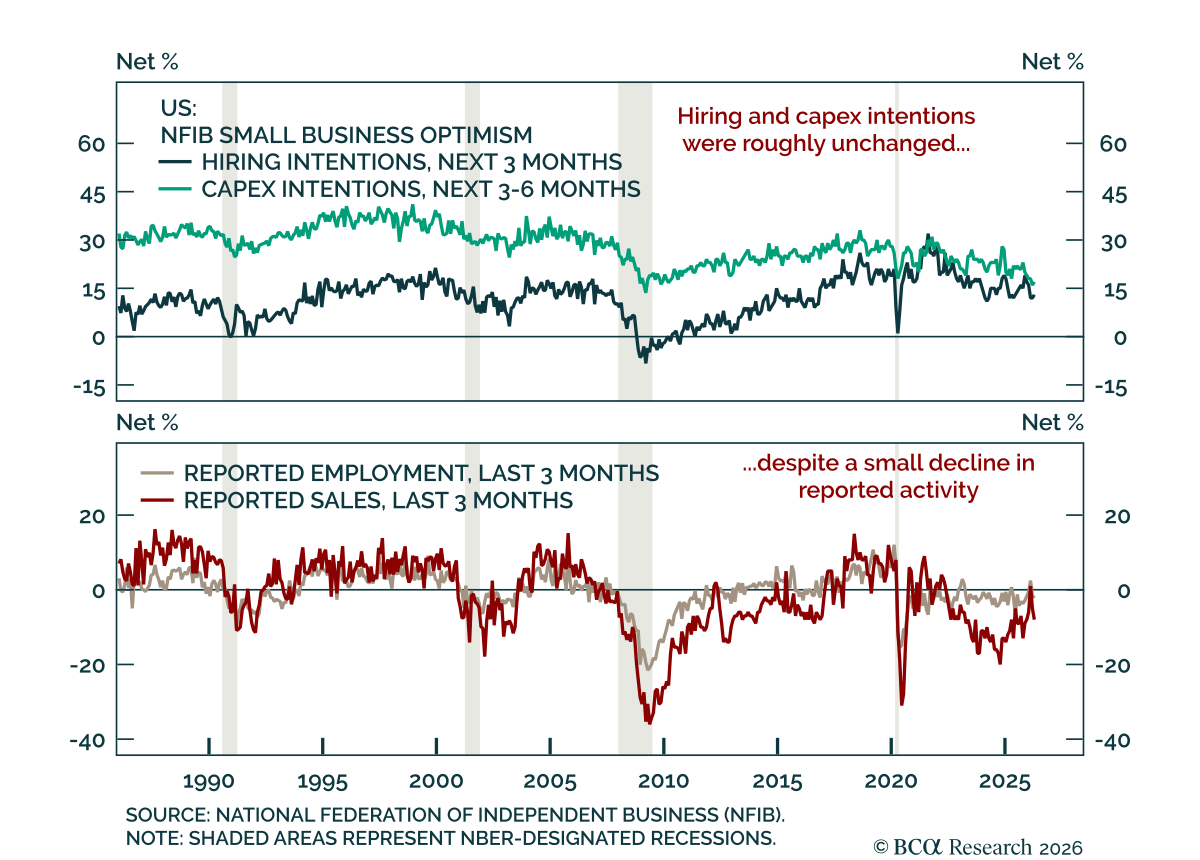

The April NFIB survey pointed to weaker growth, even as labor-market signals firmed at the margin. The index came in at 95.9, up slightly from 95.8 in March, but expectations deteriorated to 4% from 11%. More importantly, firms’ reported sales and employment…

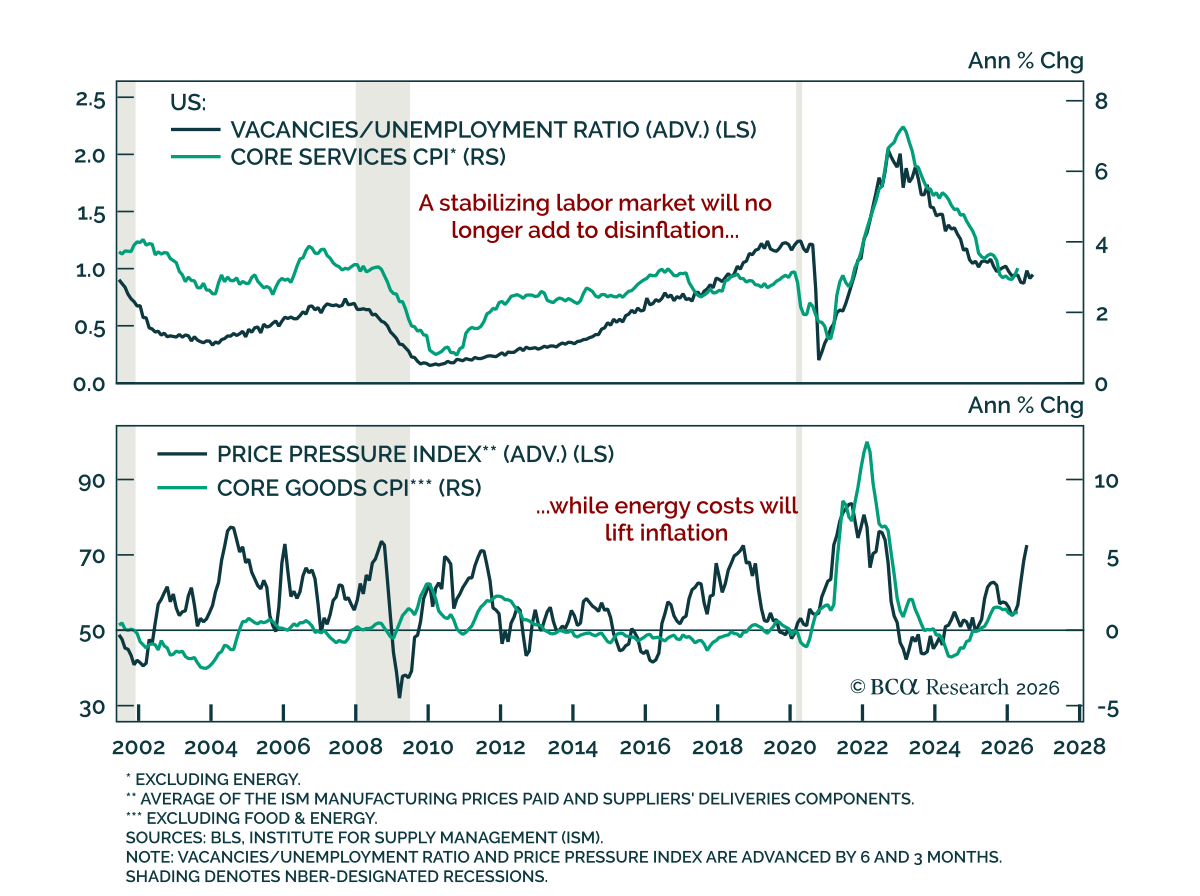

The April CPI report showed clear evidence of the direct effect of higher oil prices on inflation but, so far, limited evidence of passthrough to core.

The investment cycle remains firmly intact, driving equity prices and fundamentals, as confirmed by both Q1 data and corporate commentary. Upside surprises, expanding margins, and rising capex expectations point to resilient demand. Companies confirm that AI-related demand is broad and visible, while geopolitical and credit risks remain contained and not yet systemic.