United States

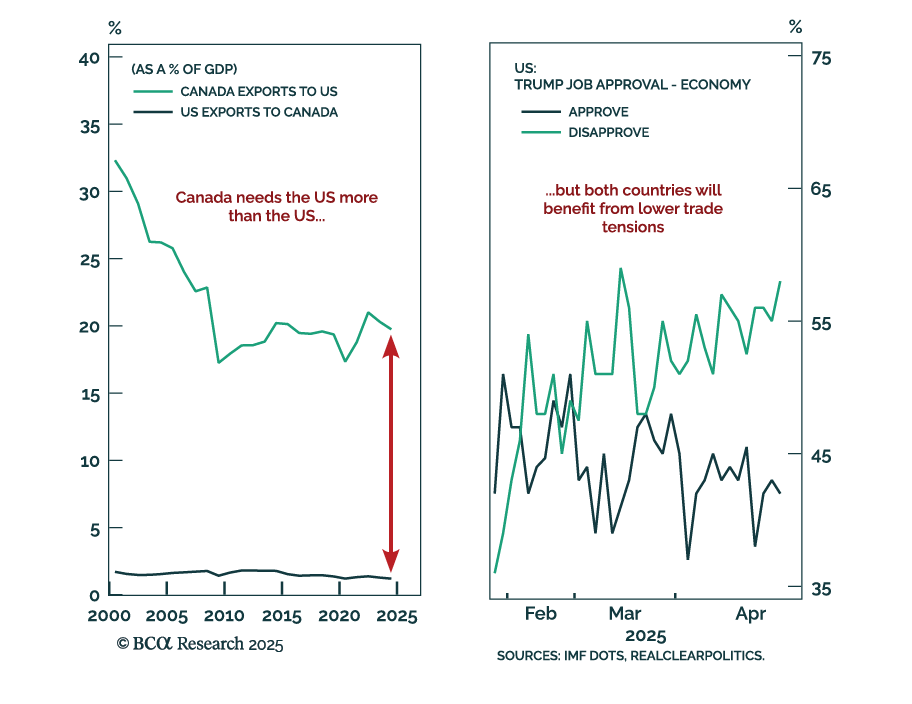

The Carney-Trump summit signals an early shift toward trade de-escalation, creating a tactical tailwind for risk assets. President Trump referred to the Canada-US relationship as a “wonderful marriage.” Moreover, both leaders acknowledged that the USMCA is “a…

Negotiations on trade, Iran, and Ukraine will prove critical this month. Markets will remain volatile because positive data surprises enable the White House to press its hawkish tariff hikes, while negative surprises force the White House to backpedal.

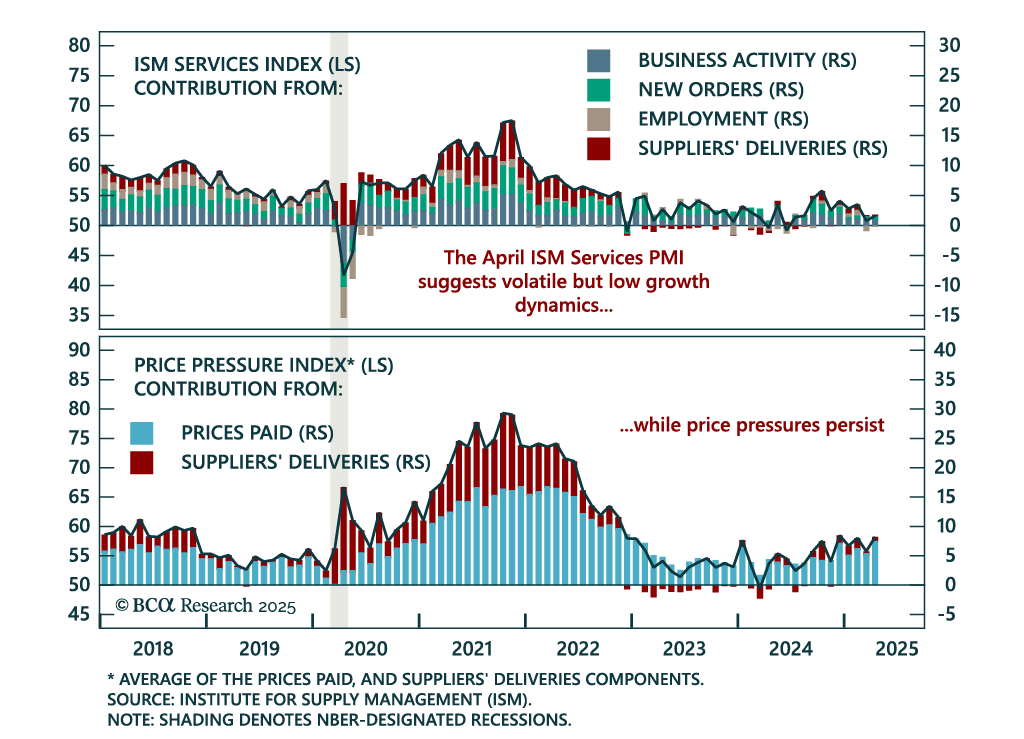

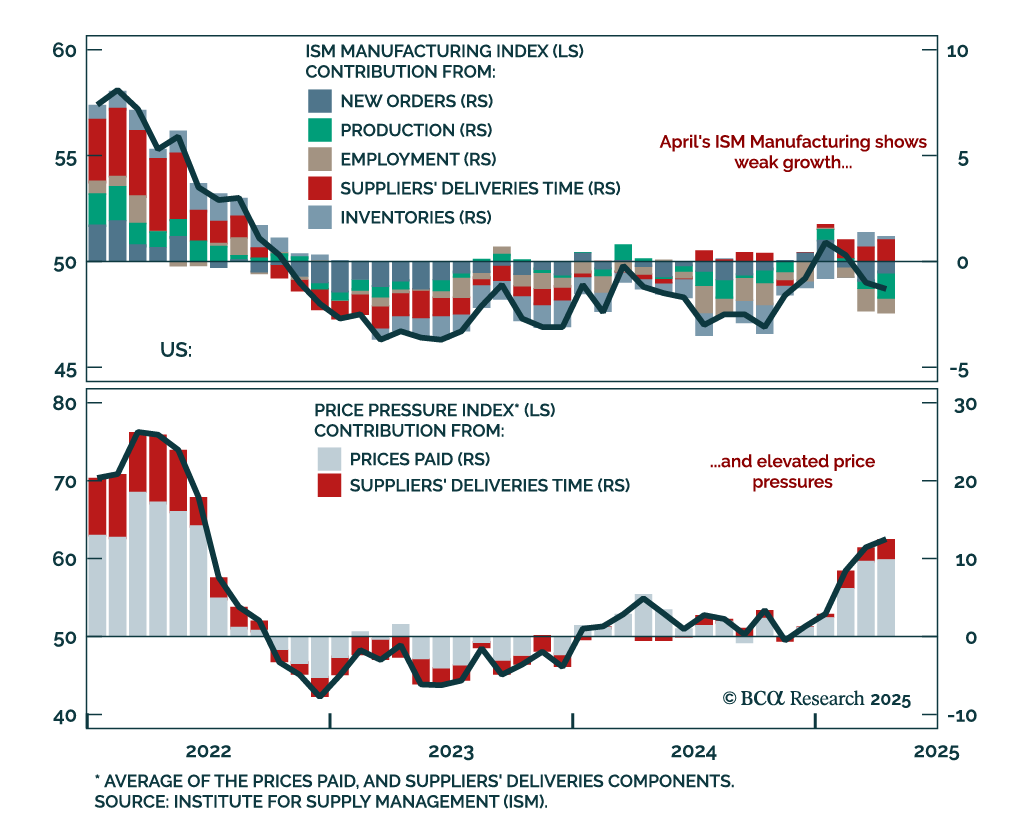

April’s ISM Services upside surprise does not shift our defensive stance, as its components show mixed momentum and rising price pressures. The headline index beat estimates, rising to 51.6 from 50.8. Business activity and new orders picked up, yet the…

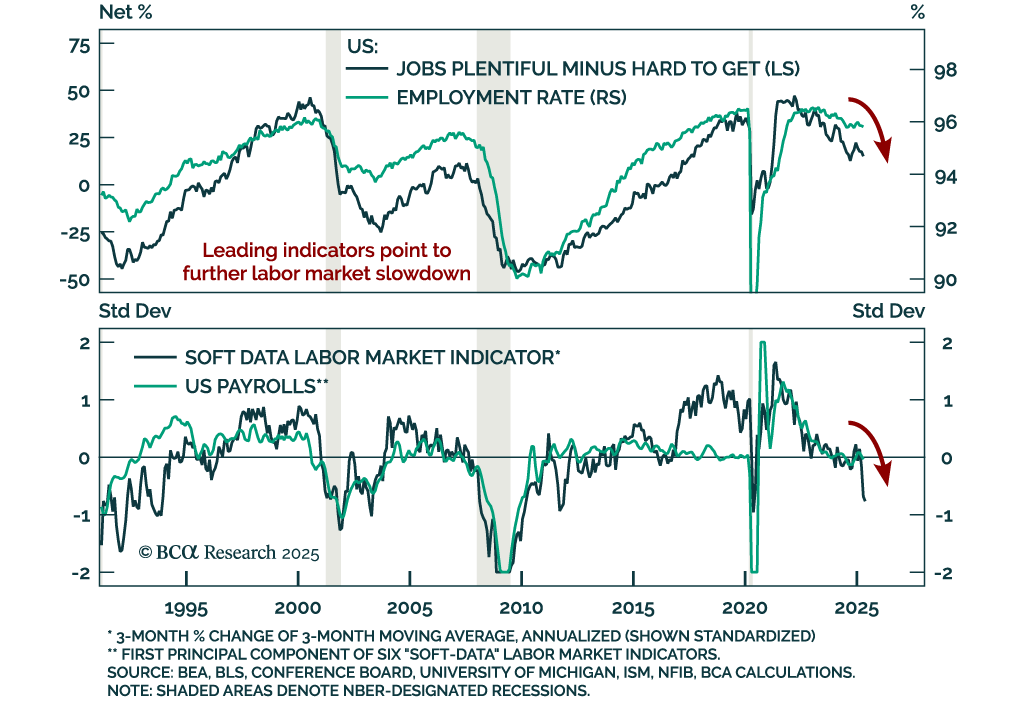

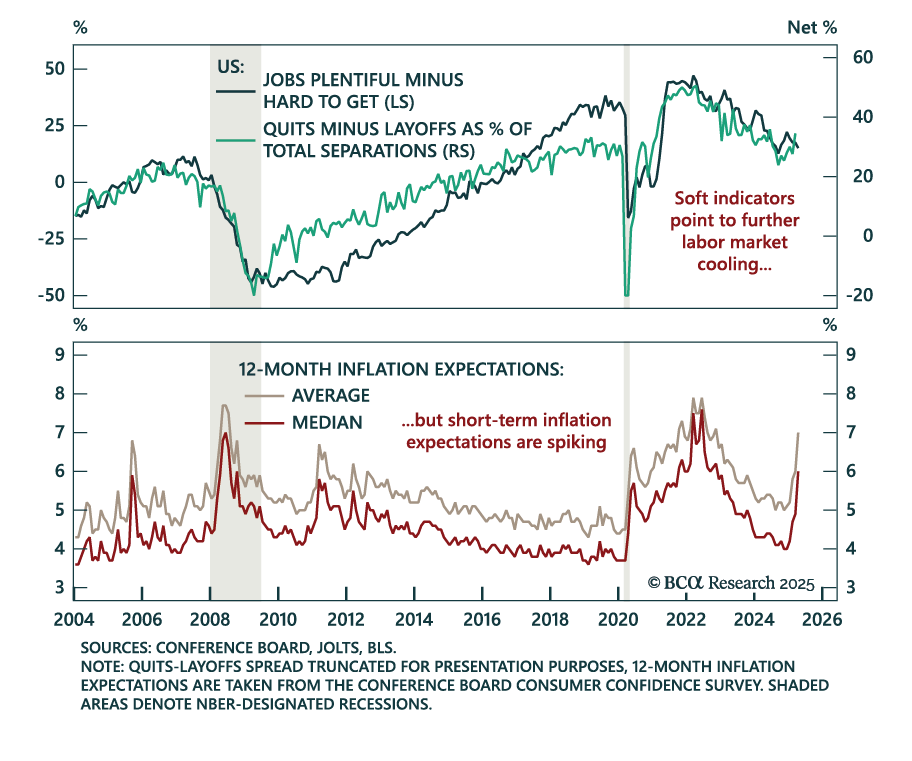

April’s stronger-than-expected US jobs report eased recession concerns, but underlying trends support our defensive positioning. Nonfarm payrolls rose 177k, but downward revisions to prior months totaled 58k, leaving the three-month average at 155k. The…

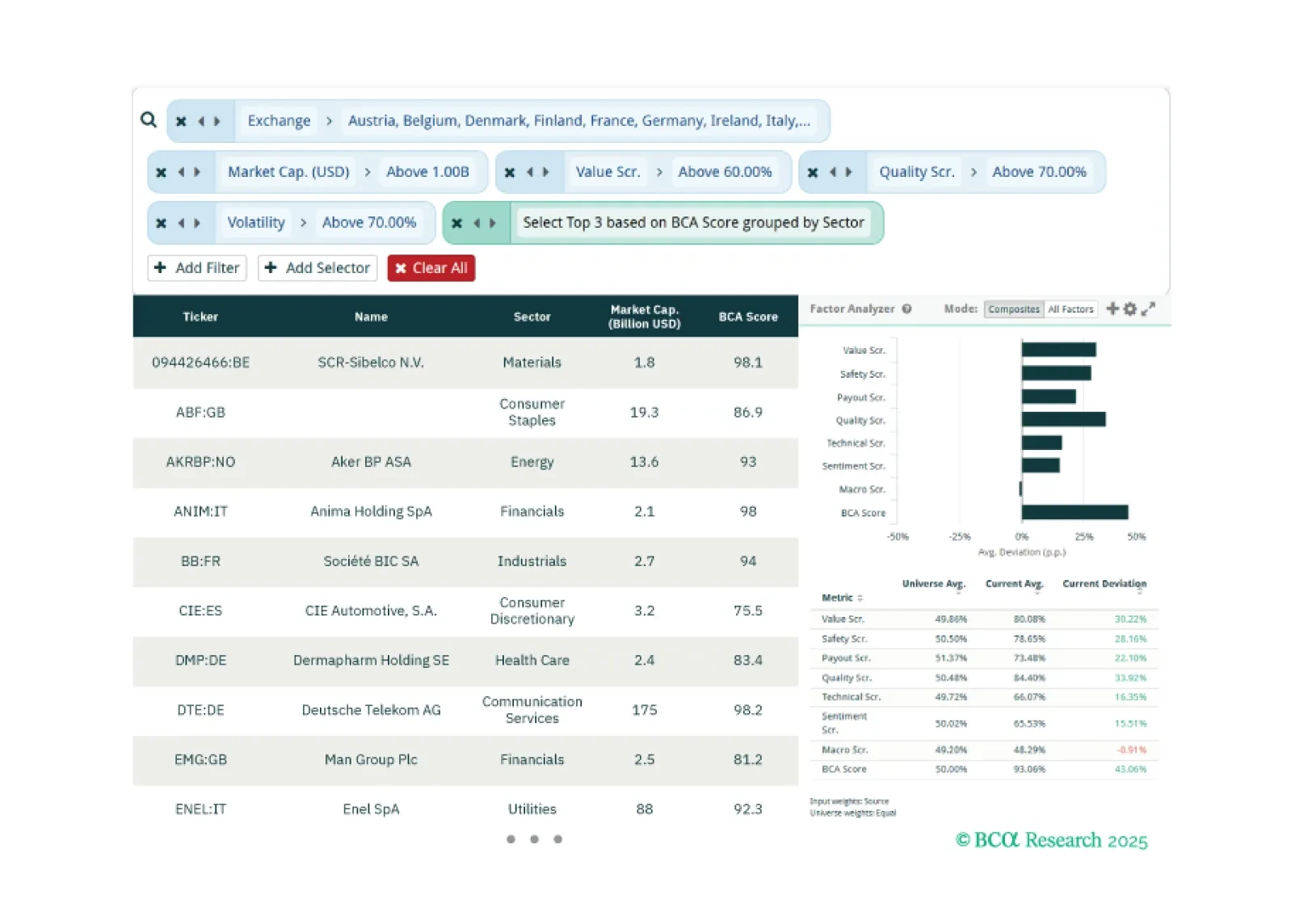

This week, our three screeners cover: Favoring European equities over US equities, cybersecurity stocks, and large caps with large moves in their BCA Score.

The April ISM Manufacturing adds to recession risks: Collapsing export orders and weak domestic momentum reinforce our defensive positioning. The index slipped to 48.7 from 49.0, with new orders still contracting and new export orders plunging to 43.1, a…

This year’s corporate bond sell off has hit high-yield more than investment grade, and high-yield spreads have turned relatively more attractive as a result.

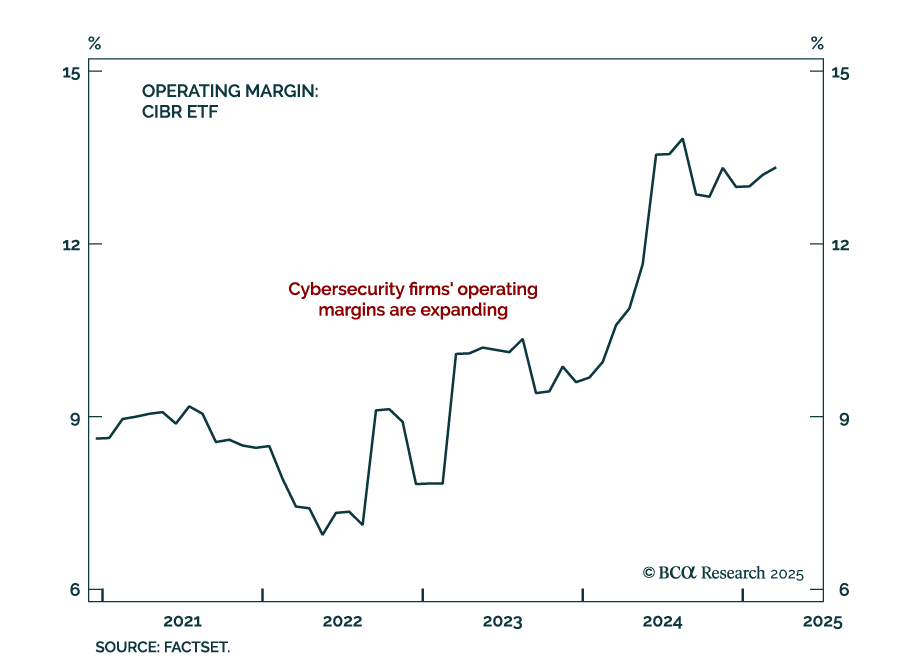

BCA’s US Equity strategists recommend building or adding to cybersecurity positions. The industry remains a strategic long-term theme with improving fundamentals and reduced valuation risk. The sector’s defensive characteristics, domestic focus, and…

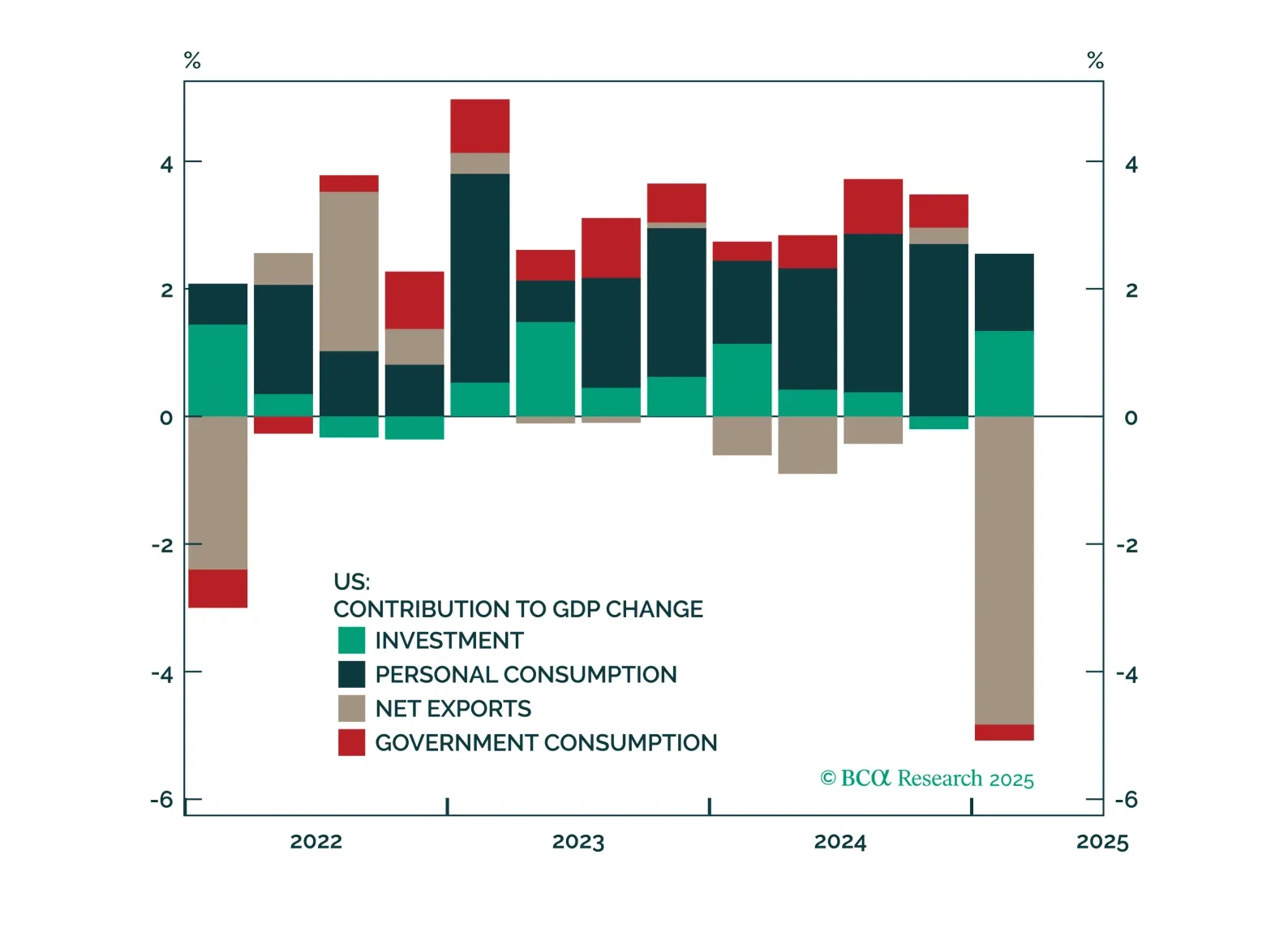

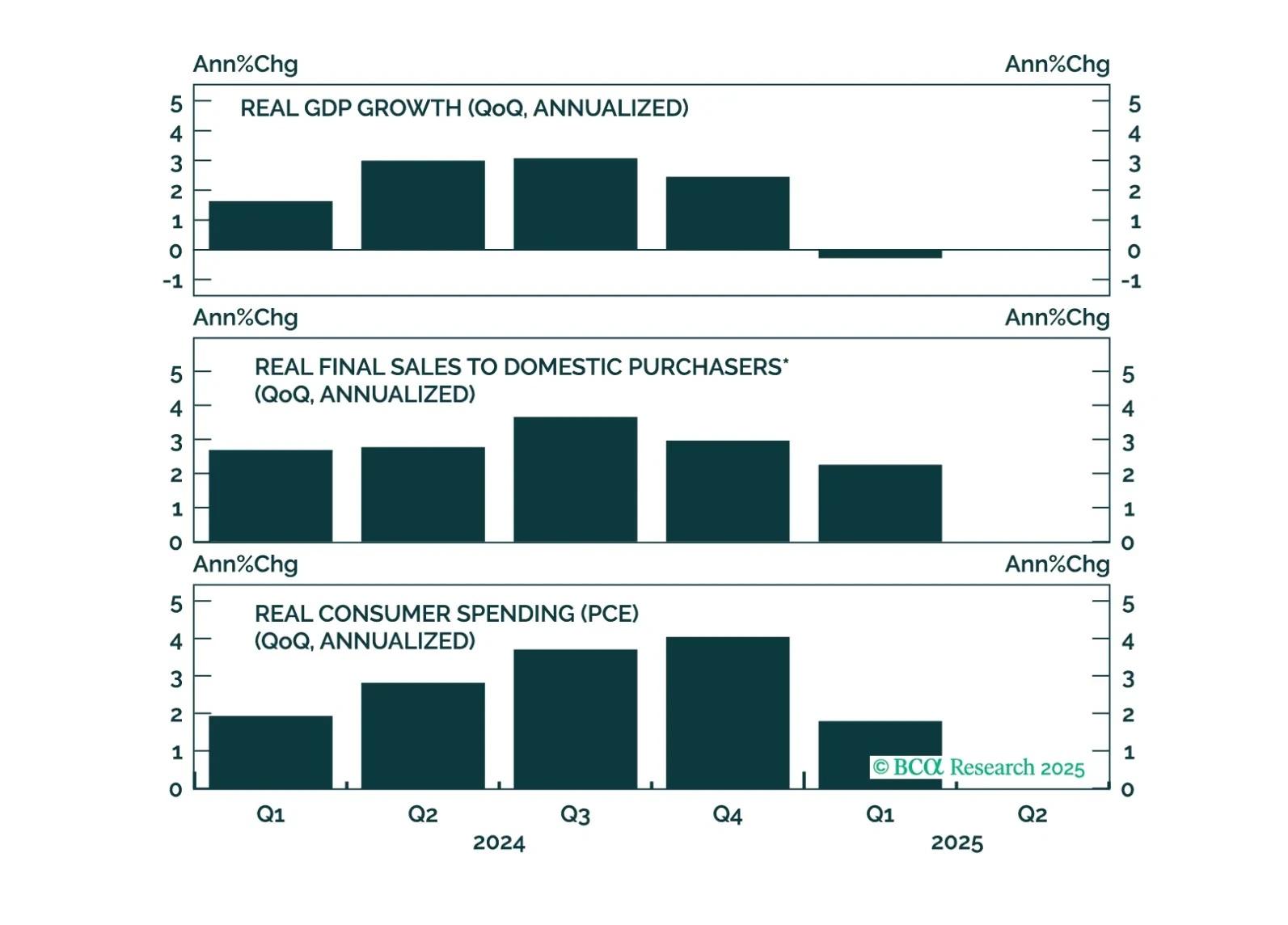

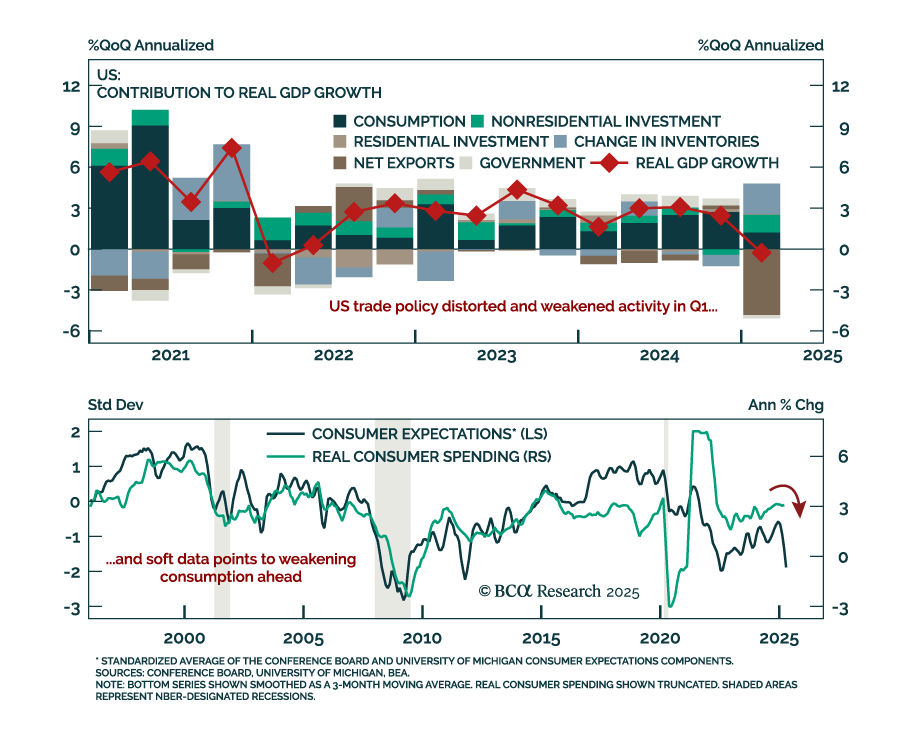

The Q1 US GDP contraction and inflation dynamics reinforce our defensive asset allocation. GDP missed estimates and contracted -0.3% annualized, led by a sharp slowdown in net exports. Consumption slid to 1.8% from 4.0%, reflecting falling consumer…

The April Conference Board survey adds to signs of labor market softening, reinforcing our defensive asset allocation. The Consumer Confidence index fell for the fifth consecutive month to 86.0 from 92.9. Expectations plunged to their lowest since 2011.…