United States

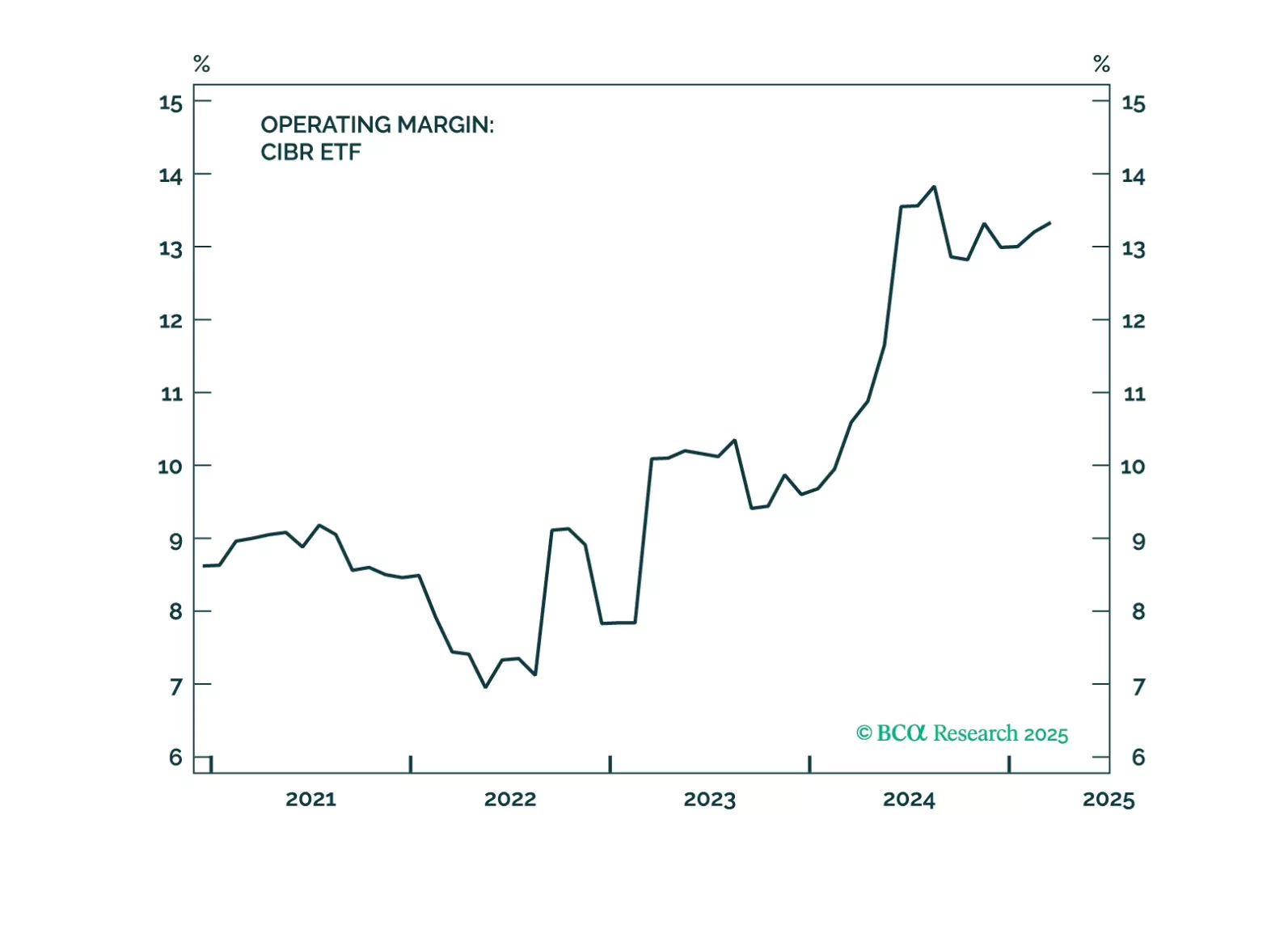

Cybersecurity is a strategic investment theme, which looks particularly interesting in light of the trade war and heightened geopolitical tensions. It is less exposed to tariffs than other industries and, if anything, benefits from geopolitical tensions as customers seek protection from international cyberattacks and cybercrime. The industry’s fundamentals are improving, while valuations are moderating. A recent pullback presents an attractive entry point into the theme.

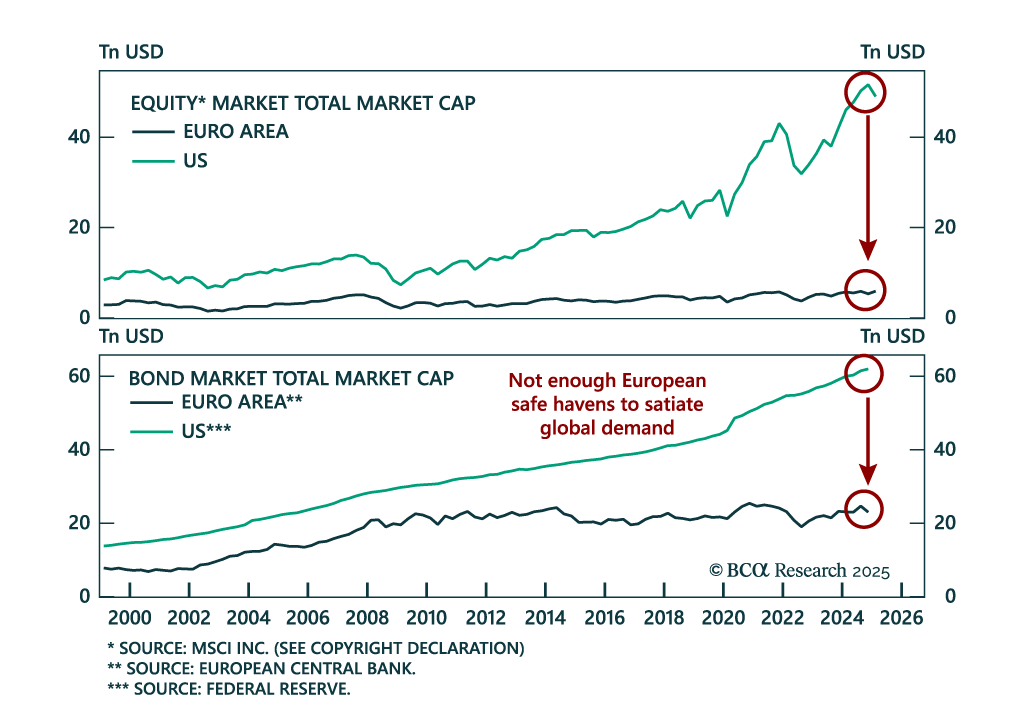

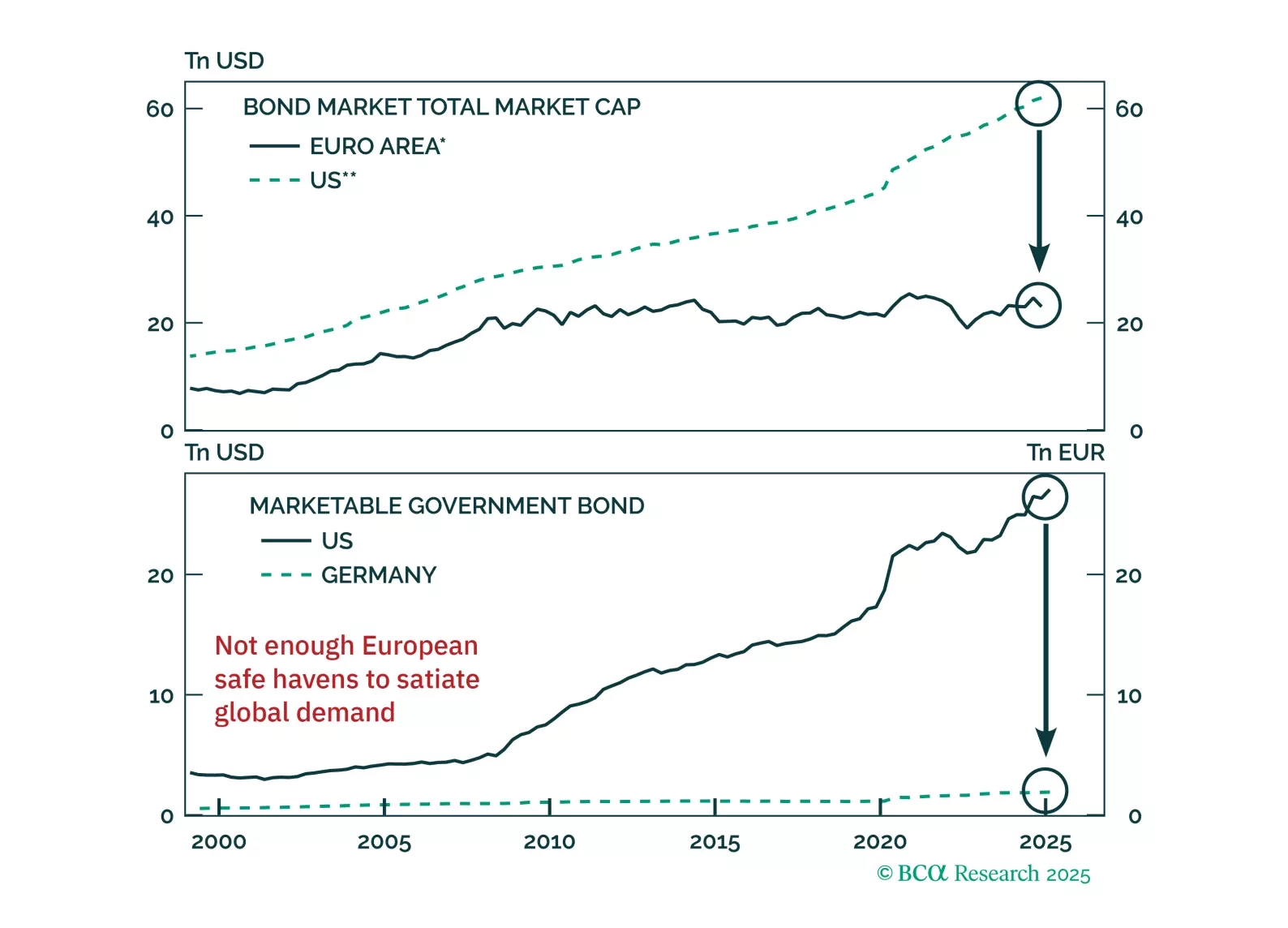

Are bunds the new Treasurys? The euro and German debt are gaining favor as safe havens, but markets may be overplaying the shift. Our latest report dissects what's durable, what's not, and how to trade the dislocation.

US Treasuries typically outperform both equities and global government bonds during downturns. Recent political shifts could lessen that outperformance this cycle, but we doubt it will disappear completely.

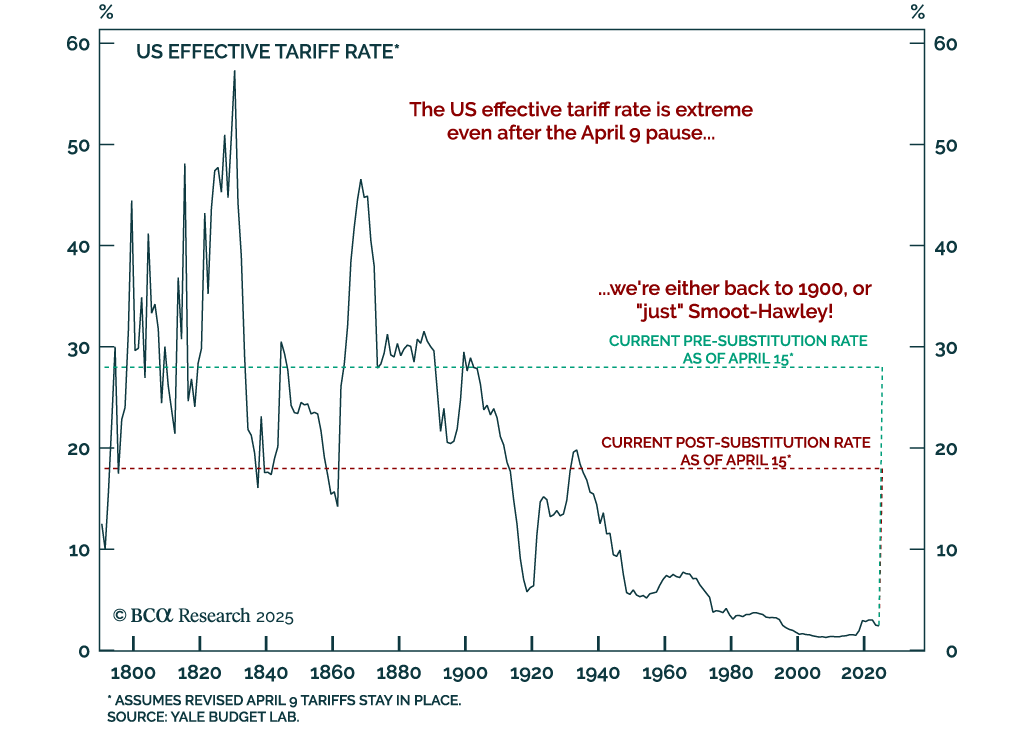

Do not play the bounce in US and global cyclical assets as Trump backpedals from the trade war. China will talk, but the pace will be slow and the outcome disappointing. Fiscal stimulus will surprise marginally in the EU, China, and even the US, but still may not rescue the business cycle.