United States

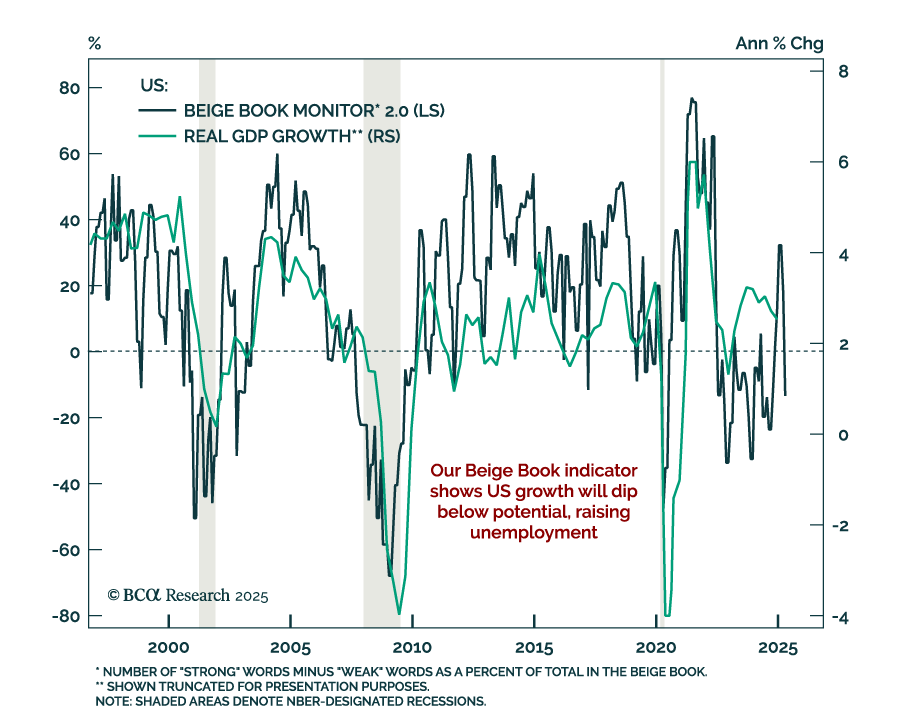

US stagflation is the main message from the April Fed Beige Book, reinforcing our underweight in risk assets and preference for gold. The report showed slowing growth, a softening labor market, and rising input costs. Our Beige Book Monitor mirrors this…

请于2025年4月24日星期四上午9:00 (北京/香港 时间) 加入BCA美国政治与地缘政治策略首席分析师Matt Gertken和美国政治与地缘政治副主编马语书的中文网络直播:《特朗普的百日新政:概览与展望》。

President Trump's pressure on Fed Chairman Powell is intensifying, but keeping Powell in place offers the administration political cover while keeping bond yields contained. Removing Powell would be legally difficult and risk unsettling markets, while his…

The policy-induced decline in consumer confidence has spread to businesses and investors, increasing the probability of a recession even if the administration reverses field on its aggressive tariff measures. We reiterate our defensive asset allocation recommendations.

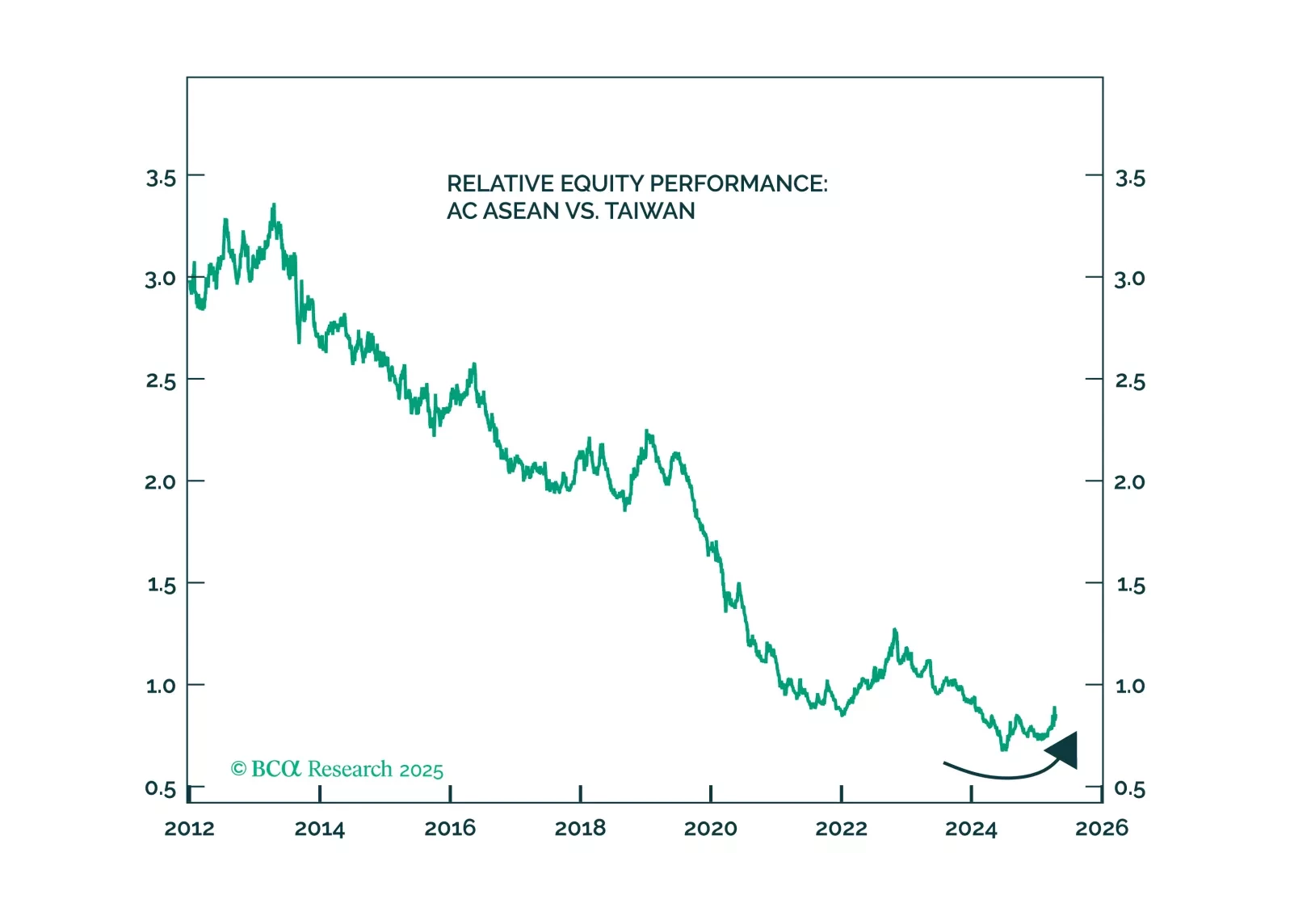

Upgrade the odds of a full-scale war in the Taiwan Strait from 5% to 10%. Rapid escalation of US-China economic war raises the probability of tensions spilling into the military-strategic domain. Investors should buy insurance against this tail risk while it is cheap. Meanwhile, use this year’s trade shock and equity volatility to increase allocation to EM manufacturing states.

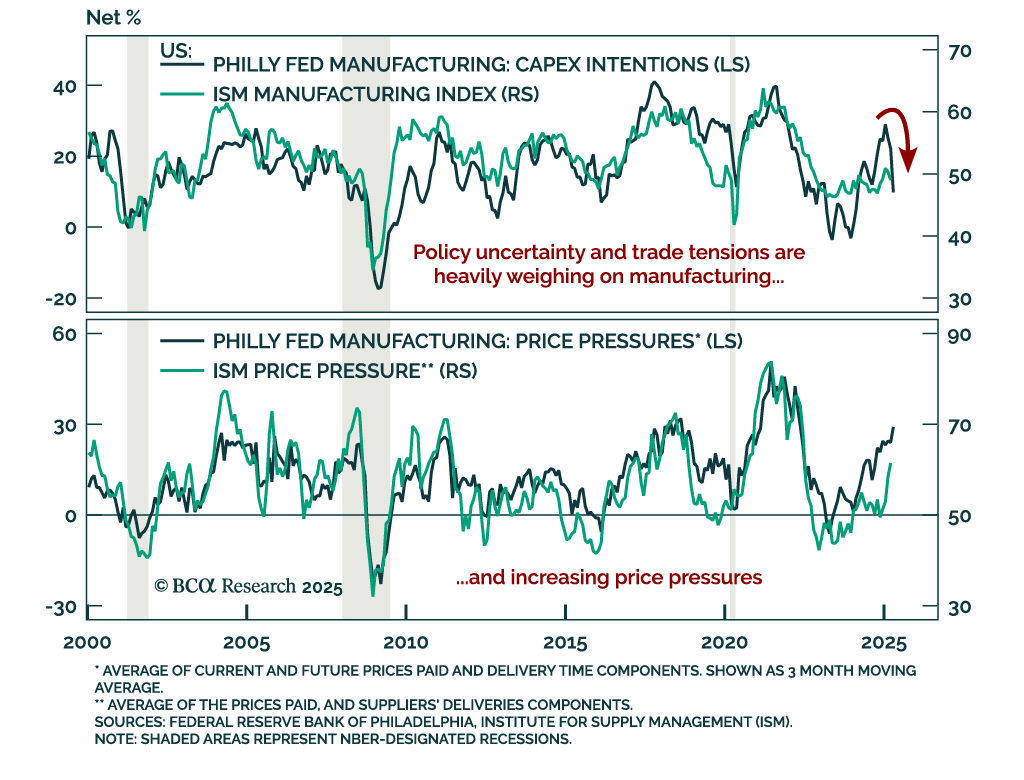

April’s Philadelphia Fed survey adds to recent stagflationary signals, reinforcing our defensive commodities positioning. The headline index collapsed to -26.4 from 12.5 in March, missing expectations and confirming the April deterioration seen in the Empire…

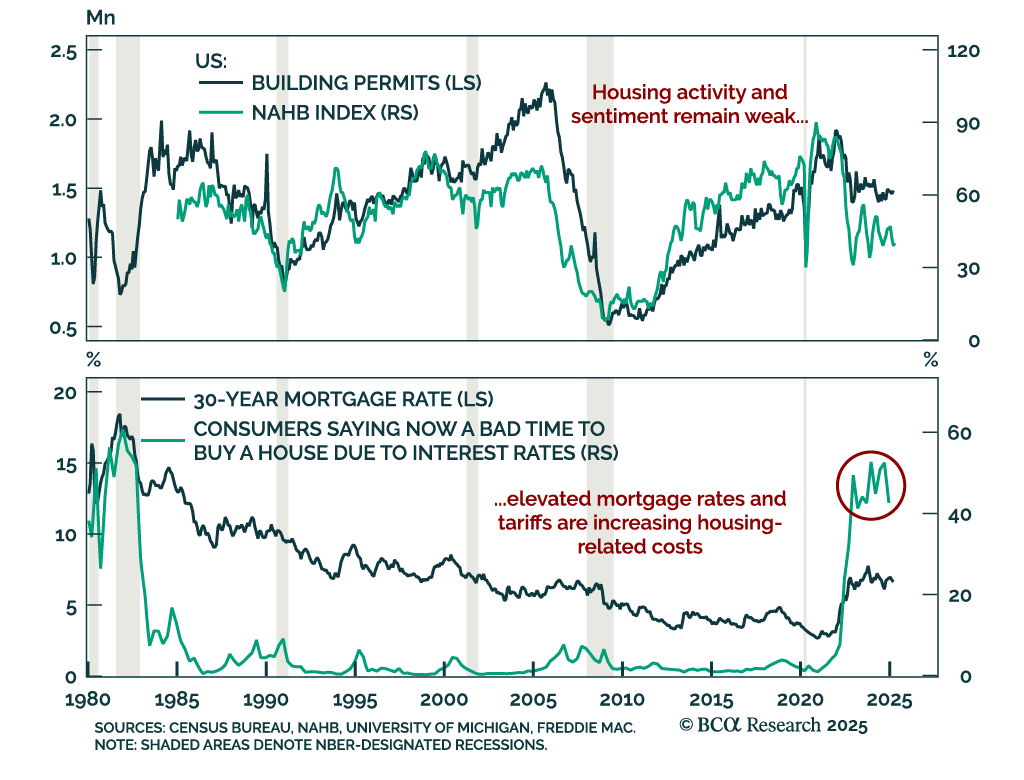

Weak housing data reinforces our defensive positioning, as recession odds remain underpriced in risk assets. US housing starts fell sharply, declining a larger-than-expected annualized rate of 11.4% in March after a 9.8% rebound in February, which was driven…

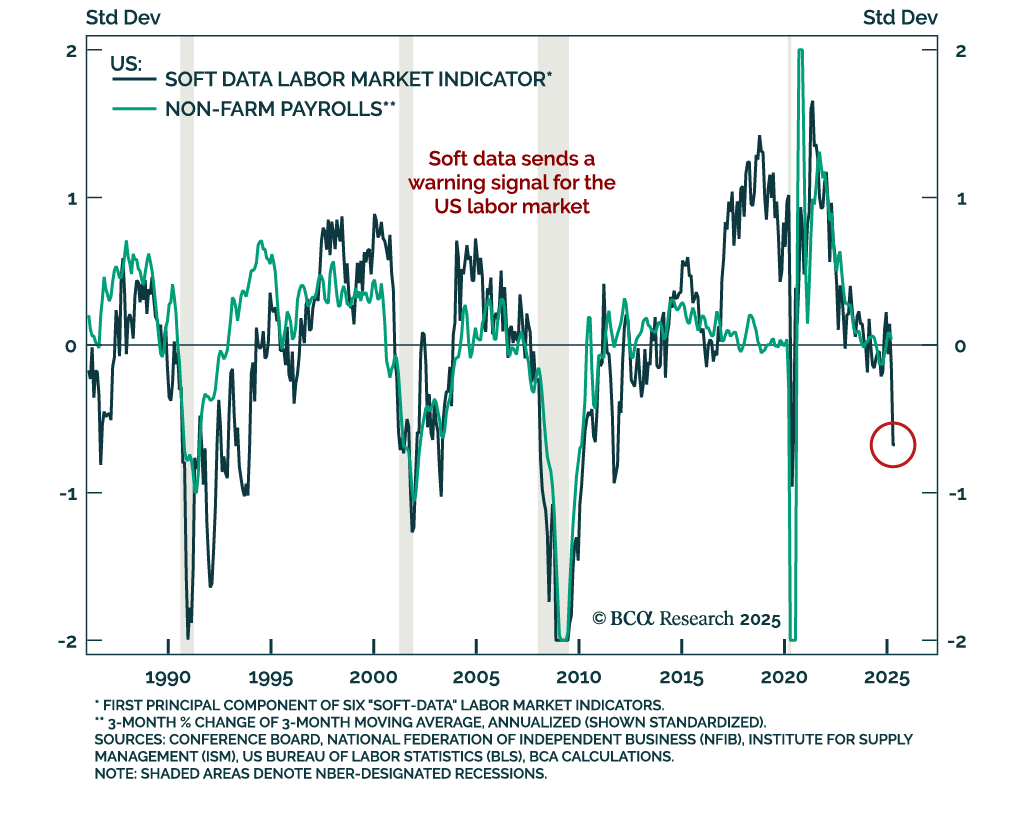

Soft data for the US labor market has turned sharply lower, reinforcing the case for a defensive asset allocation. Our Chart Of The Week comes from Miroslav Aradski from our Global Investment Strategy team. While it may take months for the tariff shock and…

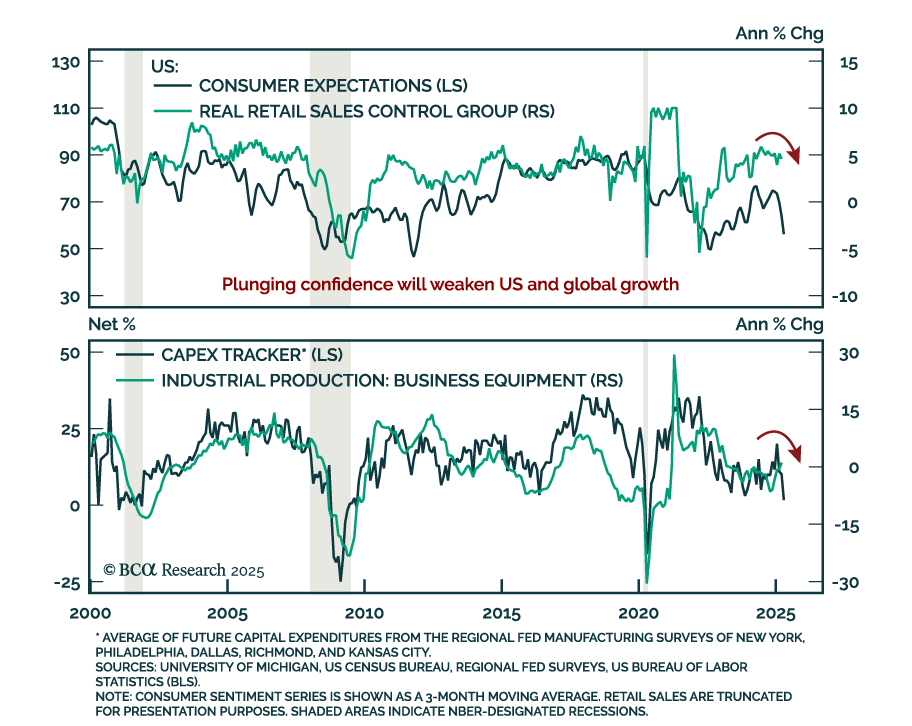

Soft data continues to deteriorate and hard data will soon follow, reinforcing our defensive asset allocation. Consumer and business confidence have plunged as policy uncertainty and inflation expectations rise, with spending, hiring and capex plans…

请于2025年4月17日星期四上午9:00(北京/香港/台北 时间)加入BCA全球资产配置高级策略师唐小莉的网络直播: 《聚焦宏观趋势,把握市场先机》。