United States

This report looks at the FX implications of the Trump tariffs, and the review of our Q1 trades.

This week, our three screeners cover: Equity plays in Low Vol & Low Beta outside the US; Chinese stocks; and stocks that are buys according to the PEG ratio.

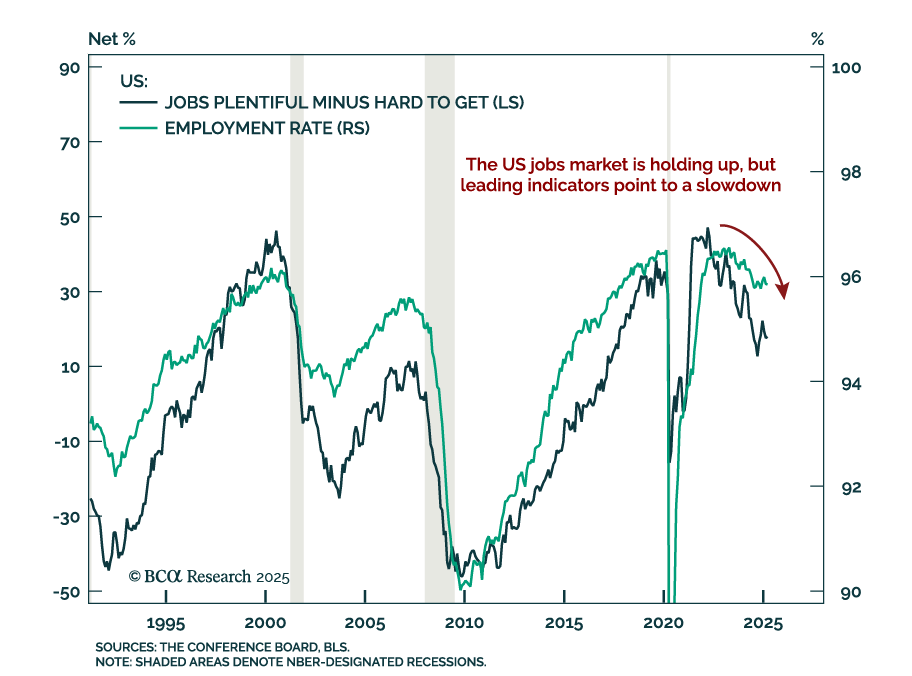

The March employment report showed strong job growth, but the labor market remains in a fragile state and the demand shock from tariffs could be the catalyst that tips it over the edge into recession.

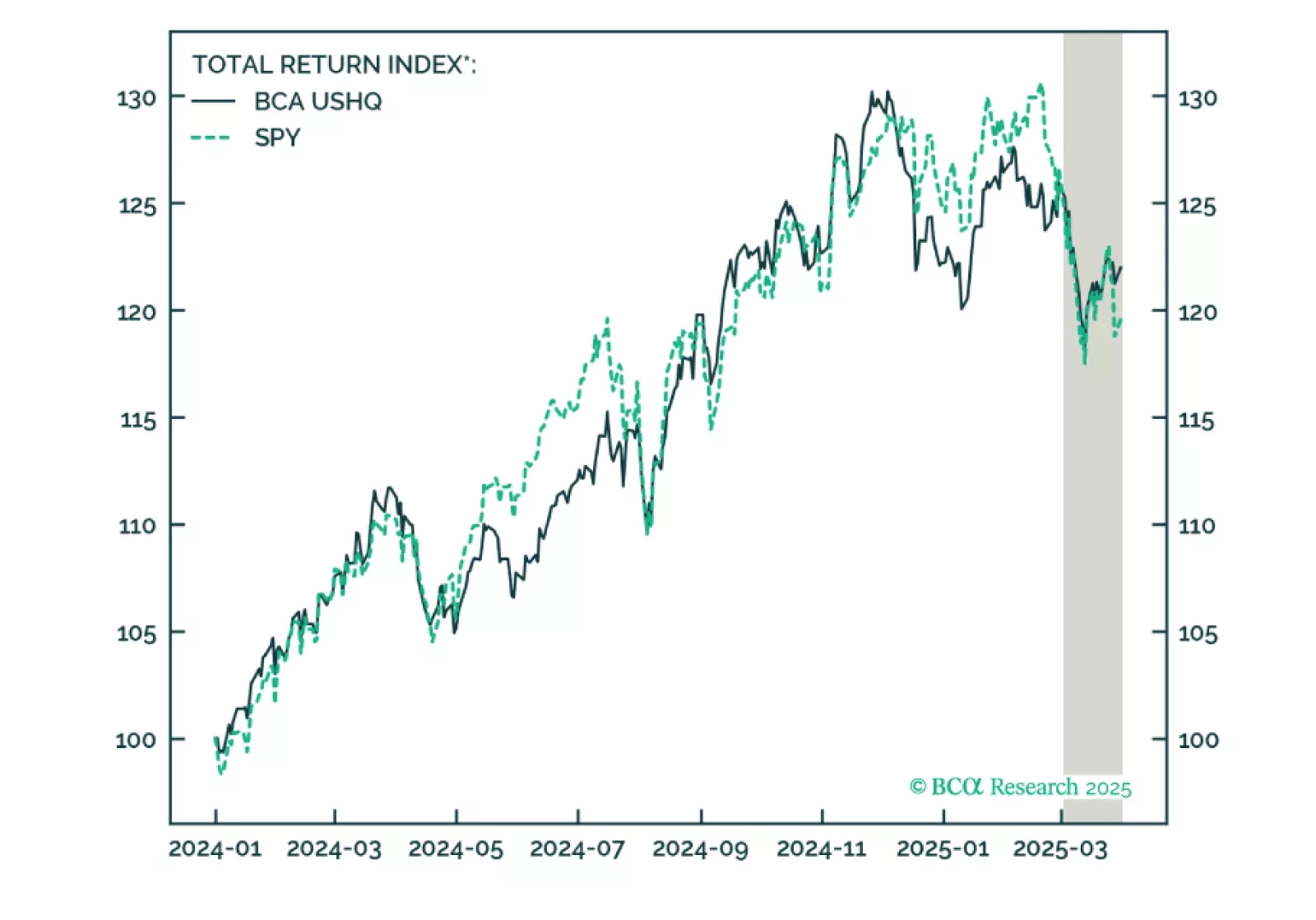

The US High Quality (USHQ) portfolio outperformed its benchmark in March, despite realizing a negative return. USHQ returned -2.6%, whilst its SPY benchmark returned -3.9%. Over a trailing-quarter basis, USHQ posted meaningful outperformance vs. benchmark, generating +230bps of excess return, while also exhibiting lower volatility and a smaller drawdown.

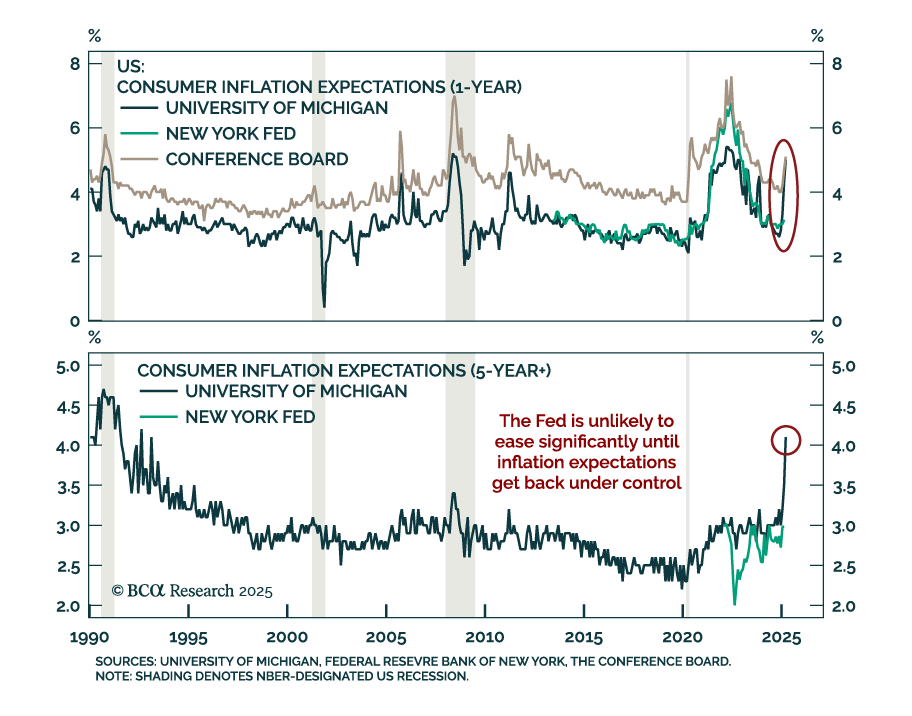

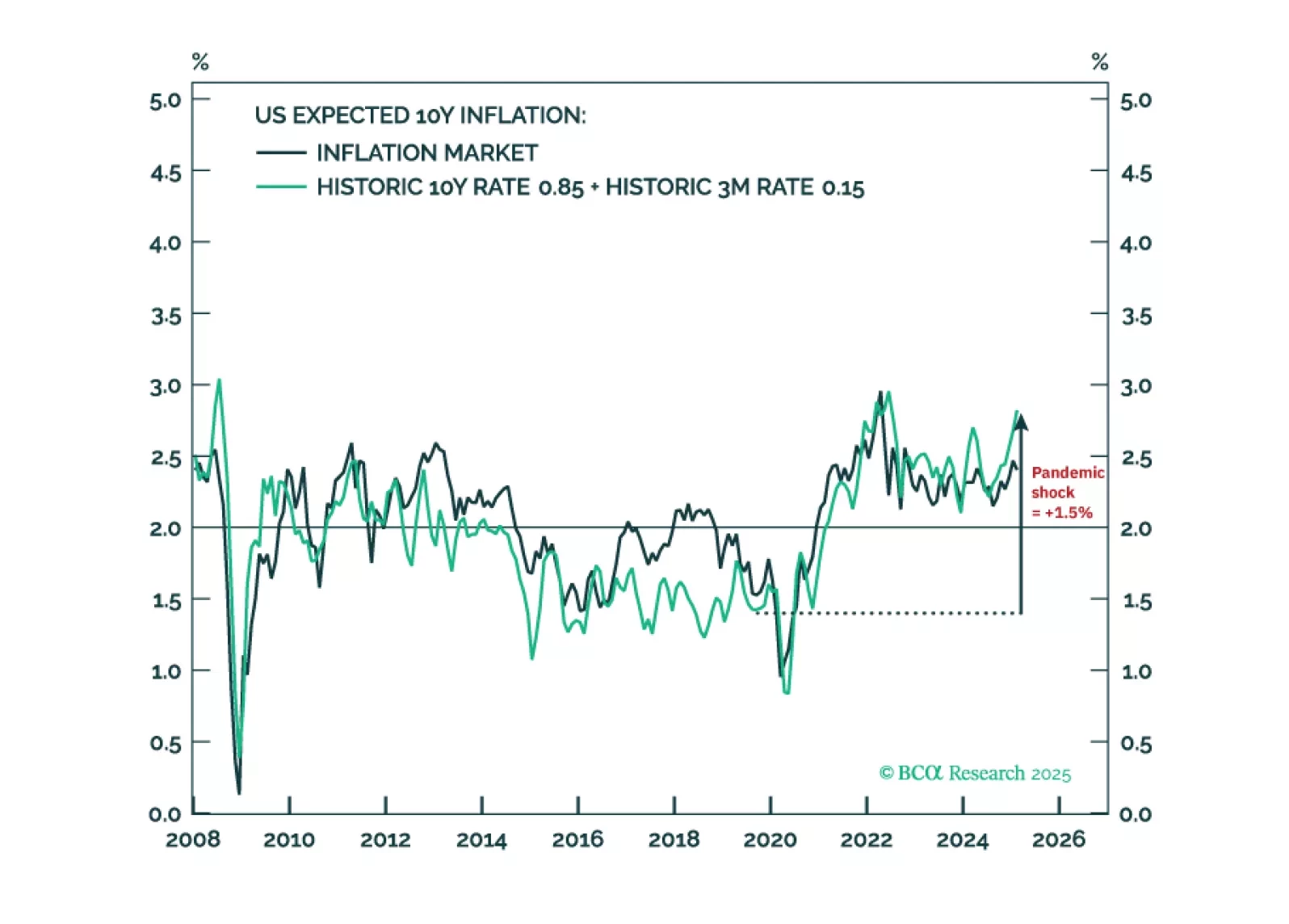

Tariffs will make a difficult job almost impossible. Hitting and sustaining a precise 2 percent inflation target is more about luck than judgement. It requires both the starting point for inflation expectations and any inflation/deflation shock to combine perfectly to 2 percent. While structural inflation expectations in the euro area and Japan could be close to 2 percent, those in the US and the UK will be stuck uncomfortably above 2 percent. We discuss the investment implications for rates and FX. Plus: gold is vulnerable to a tactical reversal.