United States

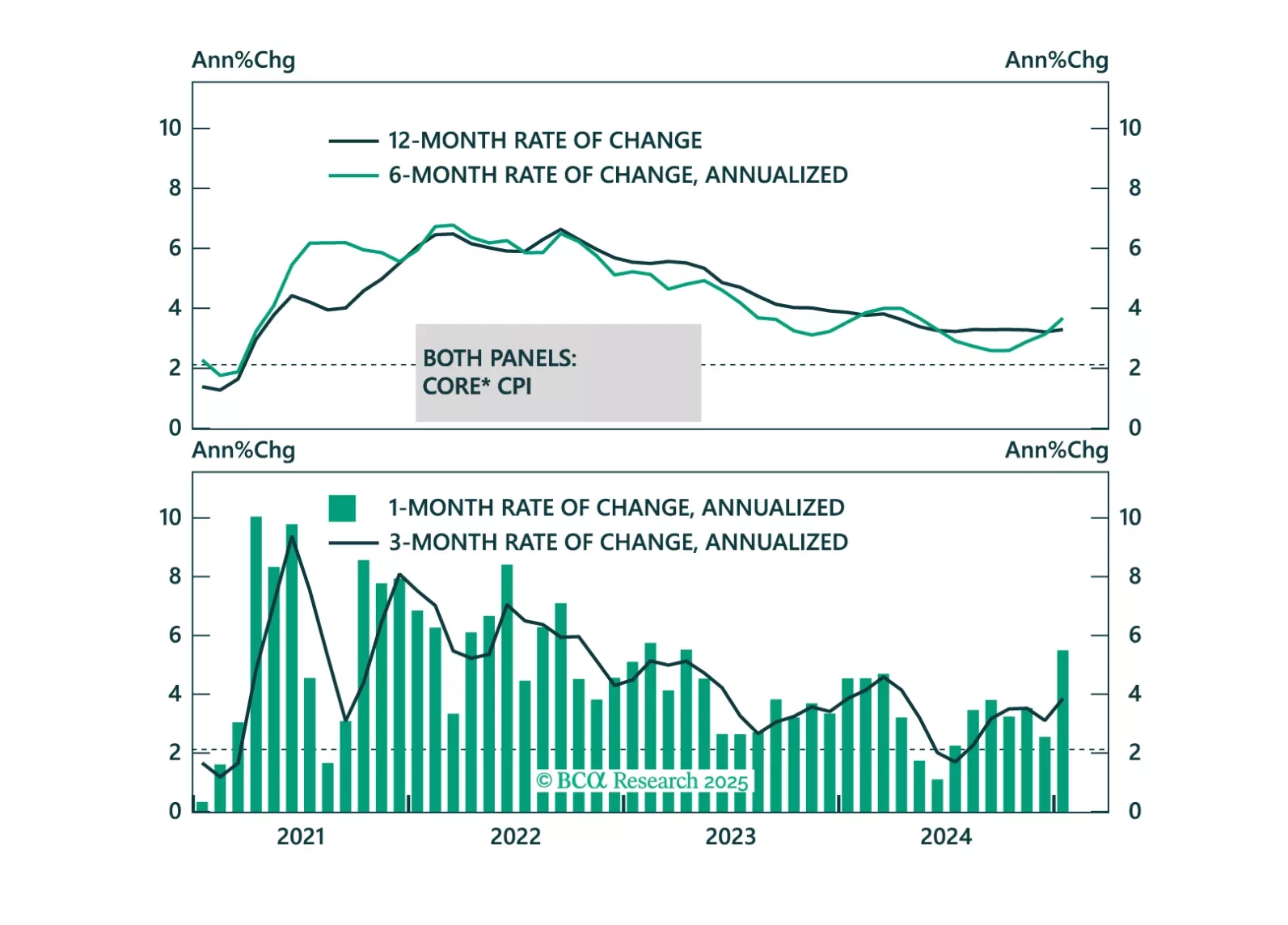

Some thoughts on this morning’s CPI report and its implications for the Fed and Treasury yields.

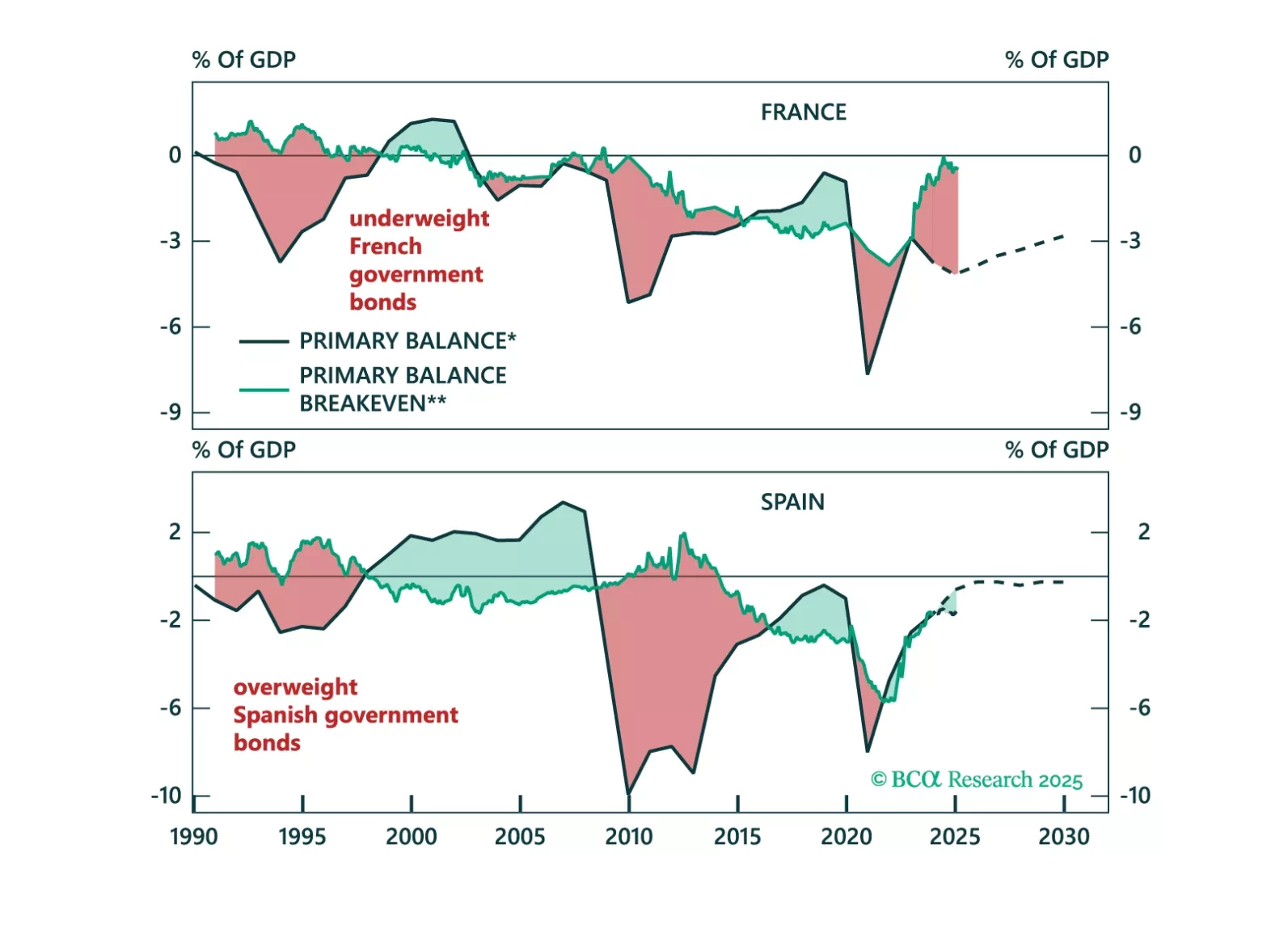

Questions about fiscal risks and their impact on bond markets have become more frequent in client conversations. This Special Report provides a framework to assess a country’s fiscal sustainability and how it affects its bond market outlook. On an individual country basis, Spain has shown a remarkable turnaround in its fiscal sustainability outlook while the fiscal outlook for France continues to deteriorate.

In his latest Thoughts Of The Day, Peter Berezin discusses the different moving parts of the global economy today and the potential impact of Trump's policies.

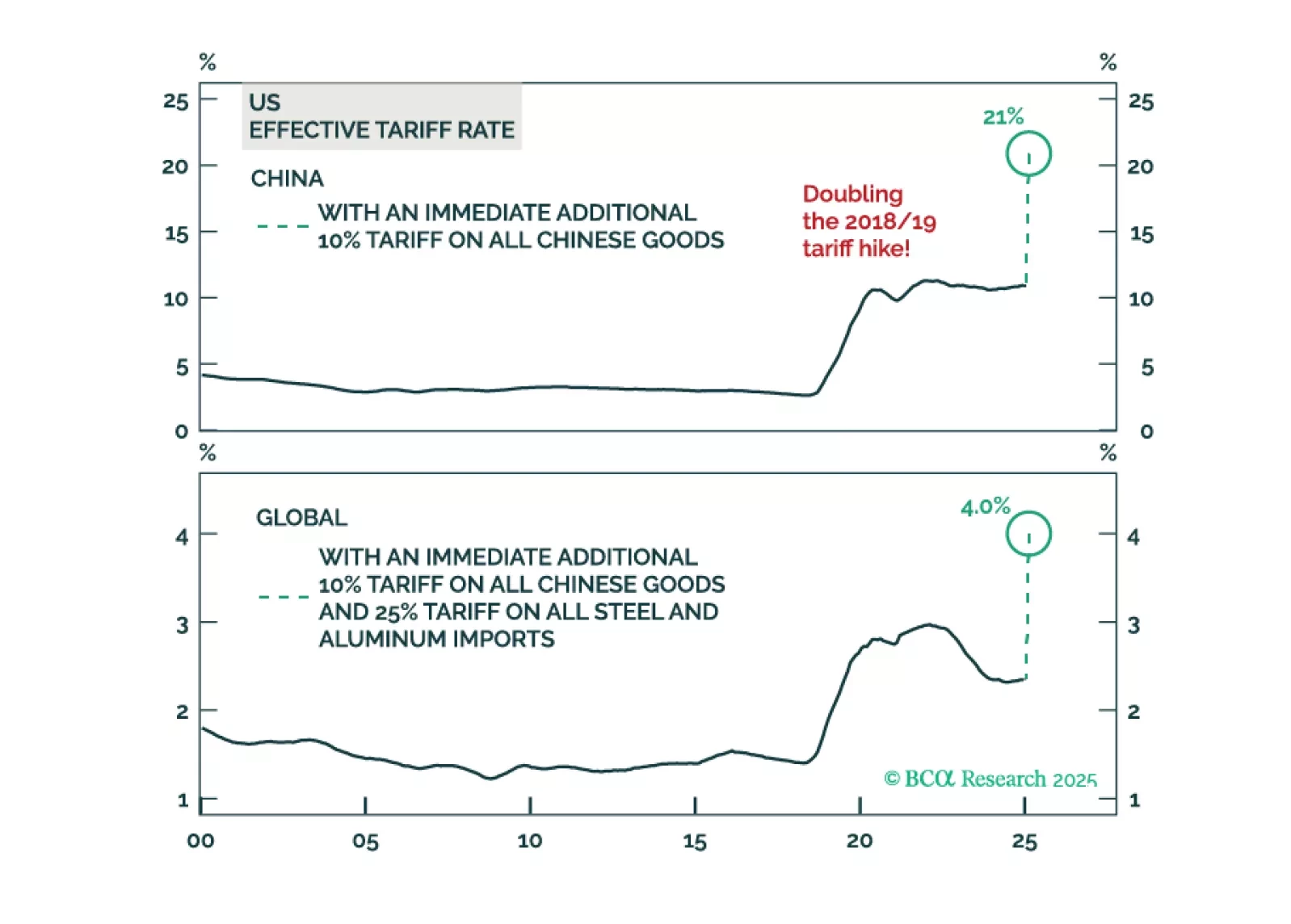

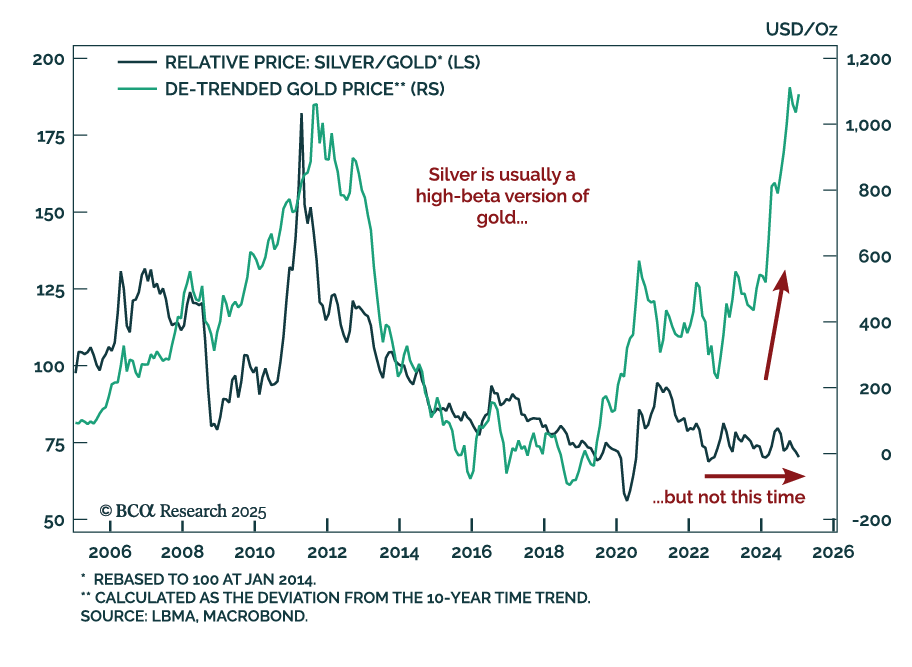

Our Commodity strategists provided an update on precious metals and the impact of US tariffs on commodities. Elevated policy uncertainty will drive a rally in precious metals over the next 12-to-18 months, but not all metals will benefit equally. Gold…

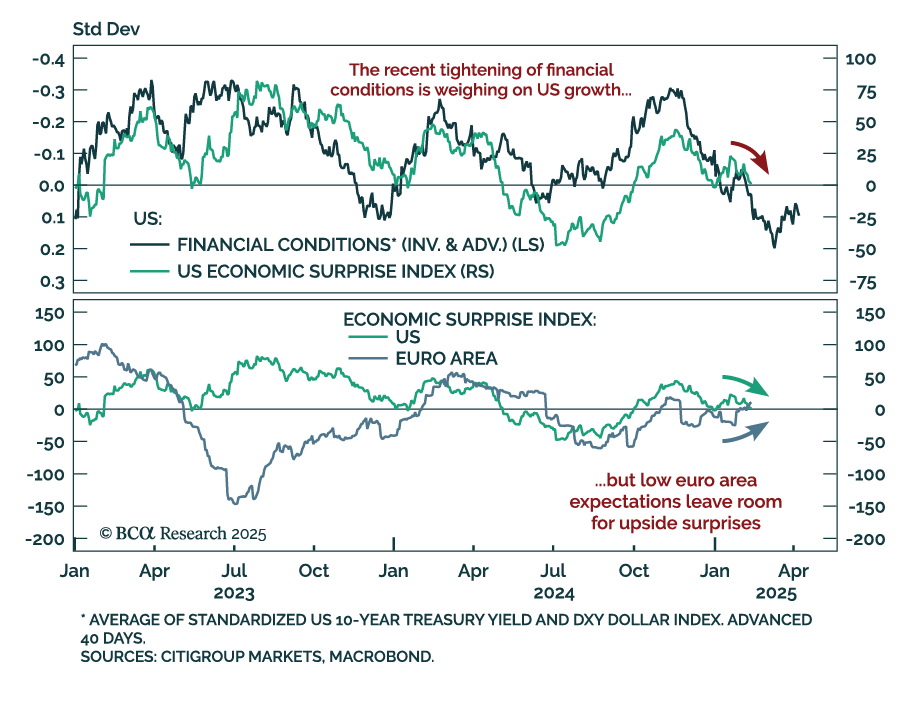

While geopolitics captured the latest headlines, Eurozone economic surprises have turned positive, while those in the US are on the verge of turning negative. Global economic surprises hinge on expectations and realized data, and they play a…

The January NFIB Small Business Optimism Index decreased more than expected to 102.8 from 105.1. After reaching near all-time highs in the wake of the election, expectations pulled back somewhat as uncertainty took center stage. The decline was…

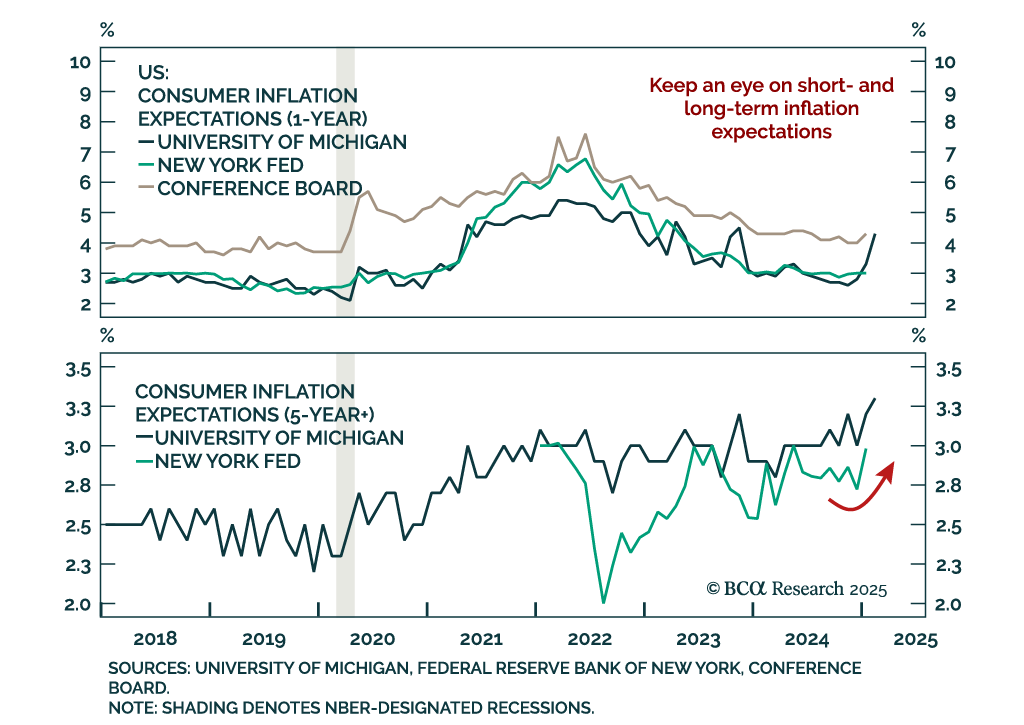

The New York Fed’s Survey of Consumer Expectations’ 1-year and 3-year inflation expectations were unchanged in January. Five-year ahead expectations however increased, as did expectations for staples inflation, while spending expectations…

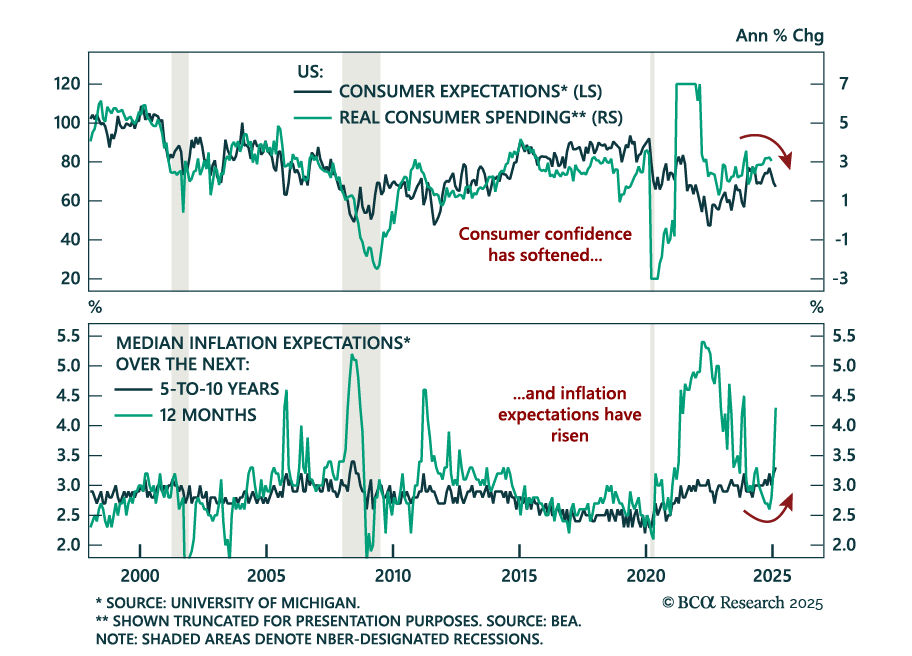

The preliminary February University of Michigan Consumer Sentiment Index missed estimates, falling to 67.8 from 71.1 in January. The decrease came from both expectations and the assessment of current conditions. Measures of 1-year and 5-10 year inflation…

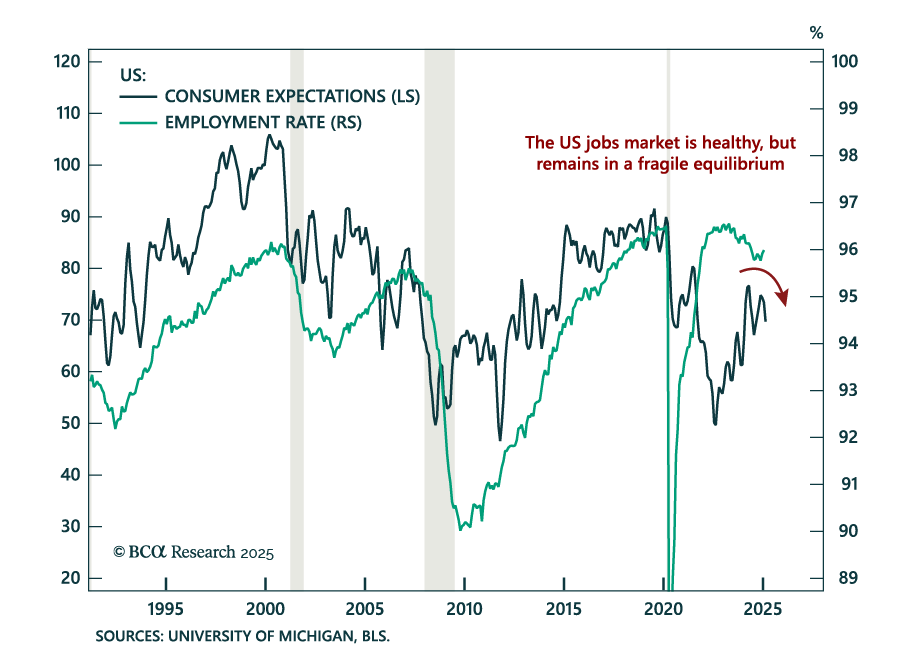

The January US jobs report was solid, reflecting a healthy labor market. Payrolls rose by less than expected at 143k, down from an upwardly-revised 307k in December, leaving the 3-month moving average at 237k. The unemployment rate ticked down 0.1% to 4.0%…

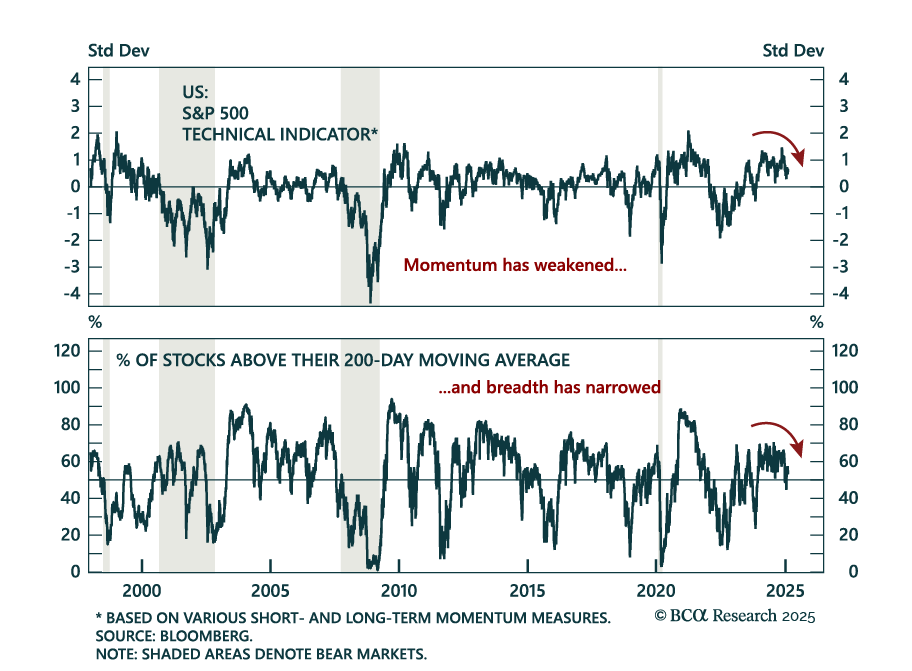

Our Chart Of The Week comes from Melanie Kermadjian, from our Global Investment Strategy team. The S&P 500 has been in a bull market for nearly five years and is currently up 2.5% YTD. A lot has been thrown at the US stock market so far this…