United States

November trading was centered around the US election and its aftermath. US assets led the way, with US equities significantly outperforming their global counterparts. The US dollar strengthened considerably against both DM and EM currencies. Investment-grade…

As 2024 closes out a busy electoral calendar for North America, our Geopolitical strategists look at Canada, where an election will be held by October 2025. Canada is poised for a likely change in leadership next year. The next government will…

Our Commodity & Energy Strategy team evaluated the impact of president-elect Trump’s policies on commodity markets. Trump’s energy policies, while promoting increased domestic oil production, are unlikely to drive immediate growth in US crude output.…

European monetary data printed in line with expectations in October, with M3 growing 3.4% y/y vs. 3.2% in September. Growth in private sector lending was unchanged at 1.2% y/y despite the recent easing in lending standards. We expect the credit impulse to…

The Fed’s preferred measure of inflation, core PCE, met expectations of 0.3% m/m in October, and accelerated to 2.8% y/y from 2.7% in September. Inflation rose on the back of hot inputs from the PPI report, which is not expected to last. The market-based core…

President-elect Trump jolted markets Monday night by declaring that tariffs will be implemented on imports from Mexico, Canada, and China. The US dollar strengthened while stocks fell, as did Treasury yields. Equities, however, recovered on Tuesday, as a…

Consumer confidence came in as expected in November, with The Conference Board’s index rising to 111.7 from 108.7 in October, a level not seen since August 2023. Both the assessment of consumers’ present and future situation drove the increase. The…

We used last Friday’s BCA Live & Unfiltered Meeting to assess our views on the US dollar after its recent bull run. While technical indicators may show short-term exhaustion, and Scott Bessent’s nomination for Treasury Secretary put a lid on recent dollar…

Our US Investment Strategy team analyzed recent US consumer trends through the lens of major retailers’ earnings calls, which highlighted increasingly prudent spending. Consumer caution is apparent in these earnings calls as pandemic-era savings fade, and…

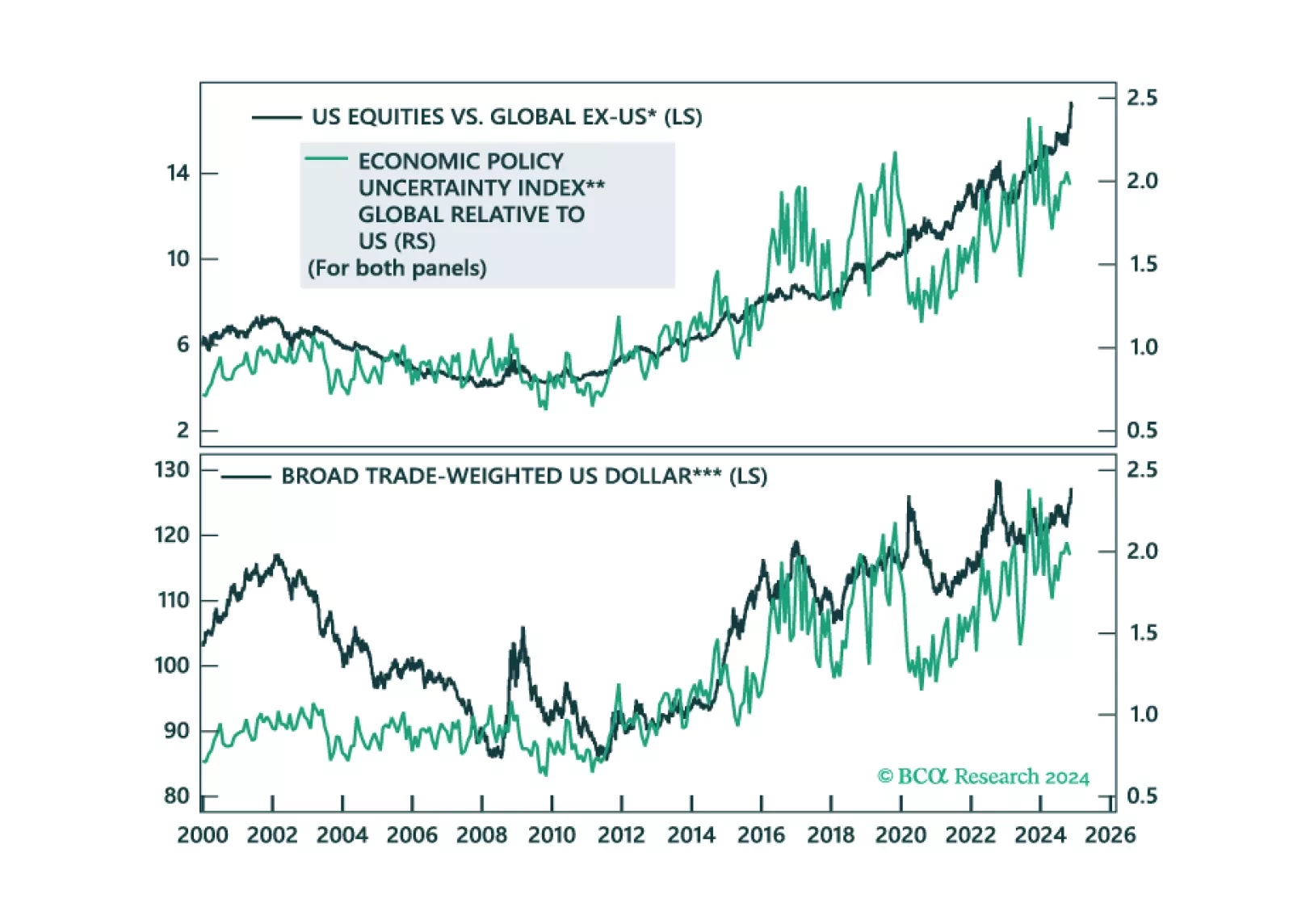

Executive Summary Political Uncertainty And The Dollar The consensus is that Republicans will blow out the budget deficit, leading to a higher fiscal risk premium on the dollar. That seems unlikely for now. If the deficit does not blow out, that path of least resistance for the dollar remains up, for now. The US economy is already outperforming the rest of the world, so does not need outsized tax cuts to keep the economy humming. Longer term, what matters are expected rates of return, and the US stock market will likely see outflows in the coming years. However, the bond market matters more for currencies, and real yields remain elevated in the US. Short-term investors should remain long the greenback. Longer-term investors should start bottom-fishing opportunities in non-currency adjusted terms where valuations are becoming very compelling. Bottom Line: Stay long the US dollar. Feature The standard economic theory is that Republicans will blow out the budget deficit, so that should be negative for the dollar, as it pushes up inflation expectations and depresses real interest rates. This is also true given a campaign trail of deregulation, tax cuts and siphoning off US competitors, via tariffs, which all sound inflationary. So far, Republicans have been rather budget friendly. For example, one of the most contested issues amongst Democrats and Republican has been what should be done around social security and Republicans are giving in to social security cuts (Chart 1). While too early to tell, the budget deficit is unlikely to be much wider under a Trump administration. Chart 1What Rising Budget Deficit? Deficits And Risk Premia Chart 2Deficits And Risk Premia Bond volatility has tended to rise as risks of a rising fiscal deficit increase. We might well end up in world where the US budget deficit does blow out, and investors will require a bigger risk premium to hold US bonds or the dollar. We are not there yet. It is true that the rise in the VIX and corporate bond spreads could be attributed to concerns about a widening deficit in the US (Chart 2), but a strong dollar tells us those concerns are premature for now. Putting President elect Donald Trump’s policies into perspective, the effective corporate tax rate in the US will be in line with many other countries (Chart 3). This means the prospect of an administration that fans the US inflationary wave is plausible, but not probable for now. That should keep US real interest rates high for now. Chart 3No Outsized Tax Cuts In The US Putting everything together, the US runs a fiscal deficit of around 8% of GDP, while the unemployment rate only sits around 4.1% (Chart 4). Ergo, this is not an economy that needs more fiscal stimulus. Most economists on the Trump administration will consider this point. Chart 4The US Does Not Need More Fiscal Stimulus The External Balance The exorbitant privilege of the dollar has meant that the US has earned more on its assets, than it has paid on its liabilities. That remains the case today, suggesting that the short-term outlook for the greenback remains positive from the basis of the US external balance (Chart 5). Ergo, more inflows into the US. That said, this is one area we are very concerned about when it comes to the dollar. For one, we know that payments on US liabilities are rising and will especially explode if we have a fiscal crisis in the US. This is worth monitoring. For now, real interest rates in the US are very positive suggesting that there should be little appetite for a massive capital flight from US Treasury securities (Chart 6). Chart 5The US External Balance Chart 6Real Interest Rates And The Dollar Chart 7Prospective Equity Returns Another source of risk is also the US equity market. US stocks are overbought and over owned, and a massive outflow from this market is a source of risk for the dollar. Over a five-to-ten-year horizon, valuations are a perfect guide for what happens in both equity, fixed income and currency markets. The message from our valuation models is that US securities are overvalued, and we should be using dollar strength to diversify into cheaper markets like Japan (Chart 7). The bottom line is that the US market remains defensive and will likely attract inflows in a global market selloff. US bonds are also a high-yielding vehicle for many foreign investors. That is bullish the dollar. Longer-term, these factors will be outweighed by valuation concerns and rising opportunities in other markets. What Should Investors Do? Here is what we know. When global policy uncertainty is rising, especially vis-à-vis the US, American stocks perform better and the dollar soars (Chart 8). With a Trump presidency baked in the cake, the potential source of any uncertainty could come from outside the US. This will keep the dollar bid. Carry trades have been a big trend in currency markets, and with EM volatility rising, a lot of these trades could still be unwound (Chart 9). EM currencies typically have a higher carry, and the yen was the perfect vehicle to fund these trades. That said, these have blown up. Within the rubble, some interesting opportunities like the Mexican Peso and the Norwegian krone that are no longer market darlings, are emerging. Stay tuned. Chart 8Political Uncertainty And The Dollar Chart 9Rising Risks In EM Currencies Chart 10Our Trading Model Is Short The USD A final note on our US dollar trading model – it remains short the greenback. The model has underperformed our recommendations since August but keeps us grounded in the methodology we use to analyze FX markets. We are excited about a new version of this model, that is more tactical in nature. That said, the blueprint of the original model was capital preservation which will remain an important tenet of any changes (Chart 10). Chester Ntonifor Foreign Exchange/ Global Fixed Income Strategist chestern@bcaresearch.com Trades & Forecasts Strategic View Cyclical Holdings (6-18 months) Tactical Holdings (0-6 months) Limit Orders Forecast Summary