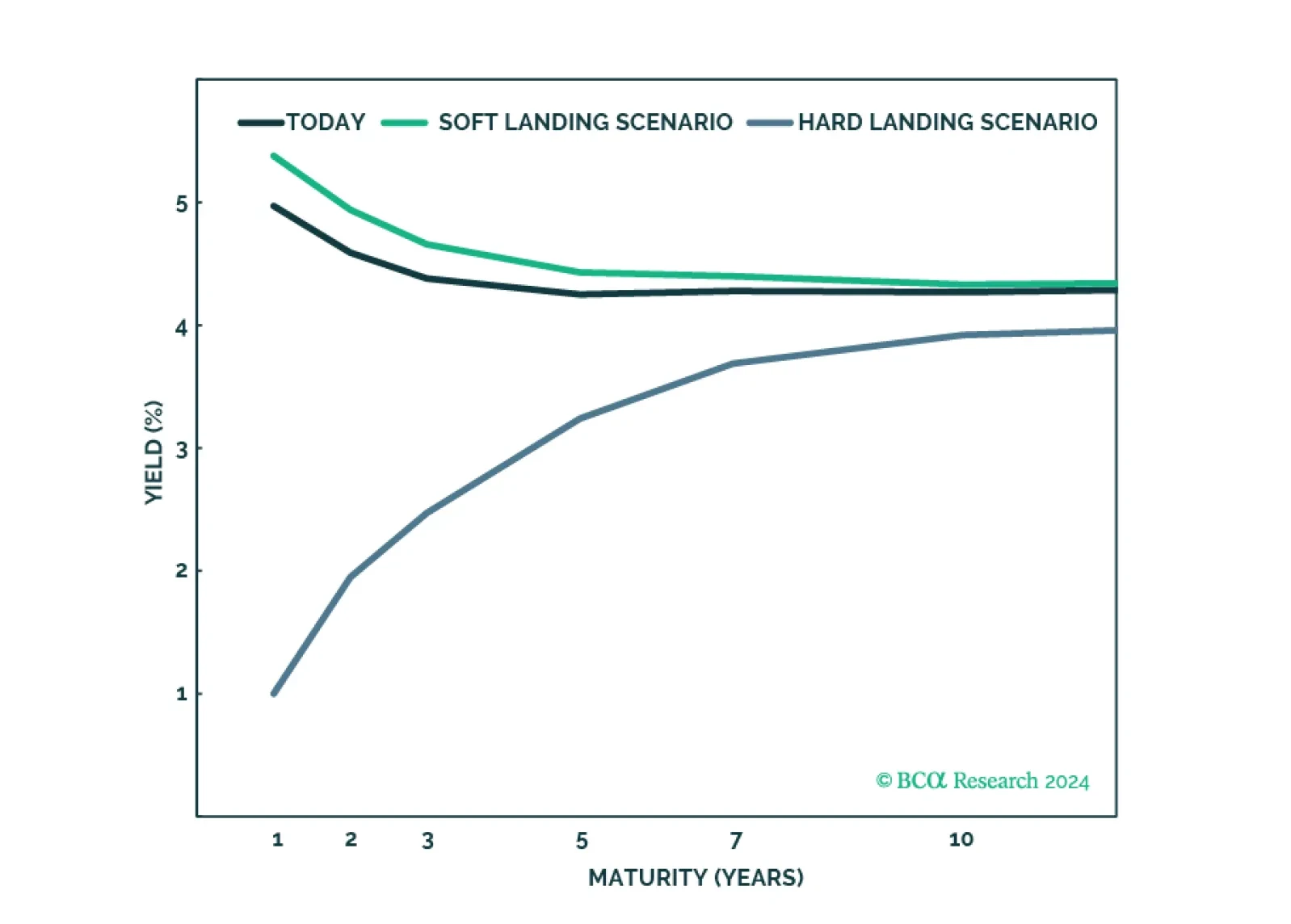

Yield Curve

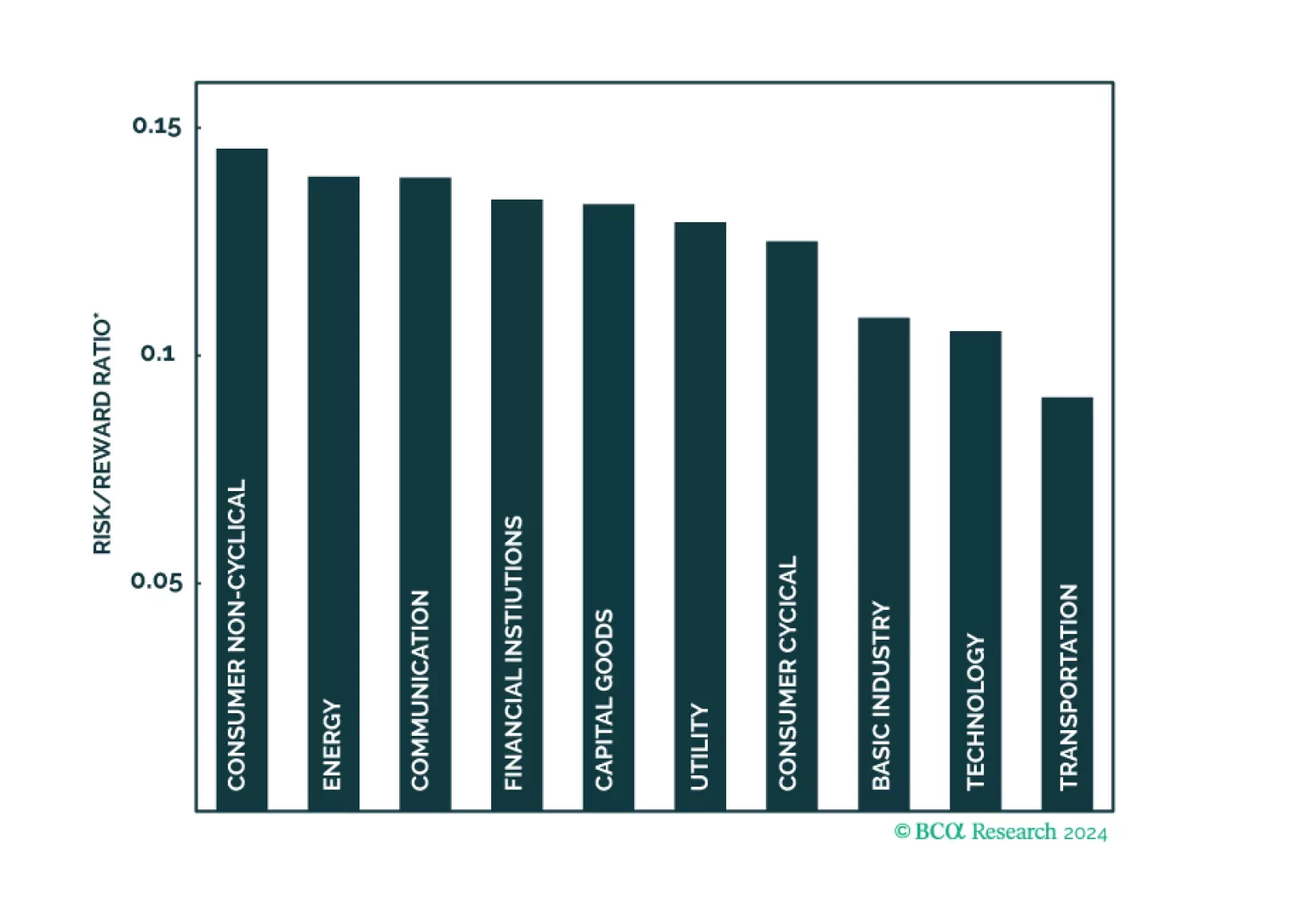

A risk/reward ranking of the 10 major US investment grade corporate bond sectors.

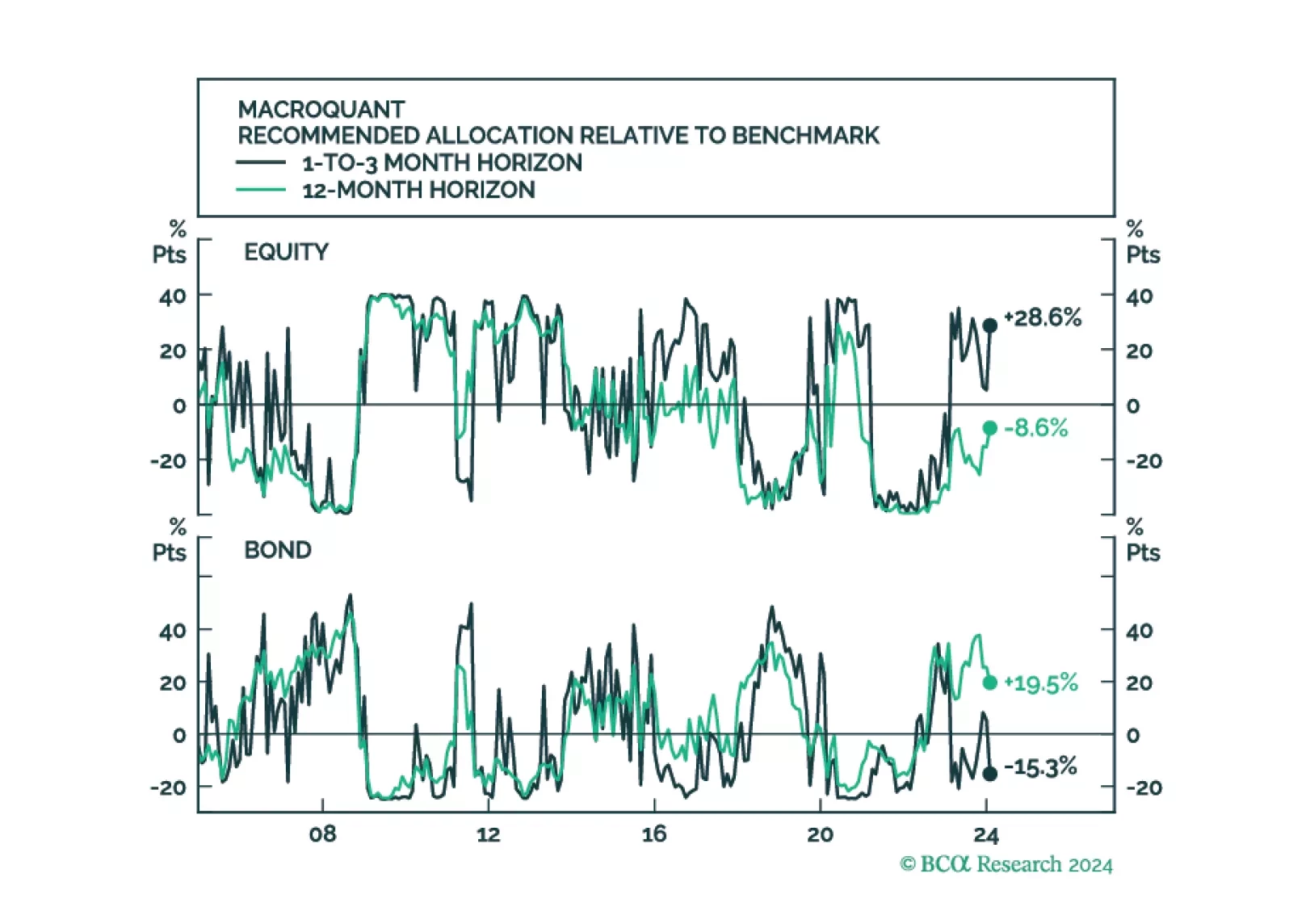

Our Portfolio Allocation Summary for March 2024.

MacroQuant upgraded equities to overweight in February on a tactical short-term (1-to-3 month) horizon, but it continues to see downside risks to stocks on a medium-term (12-month) horizon. Consistent with the model’s relatively somber medium-term growth outlook, it sees more downside for bond yields on a 12-month horizon than on a 1-to-3 month horizon.

The first in a series of Strategy Insights where we present a checklist for extending duration in each major government bond market. This first entry focuses on the US.

We rank the US spread sectors in terms of risk versus reward.

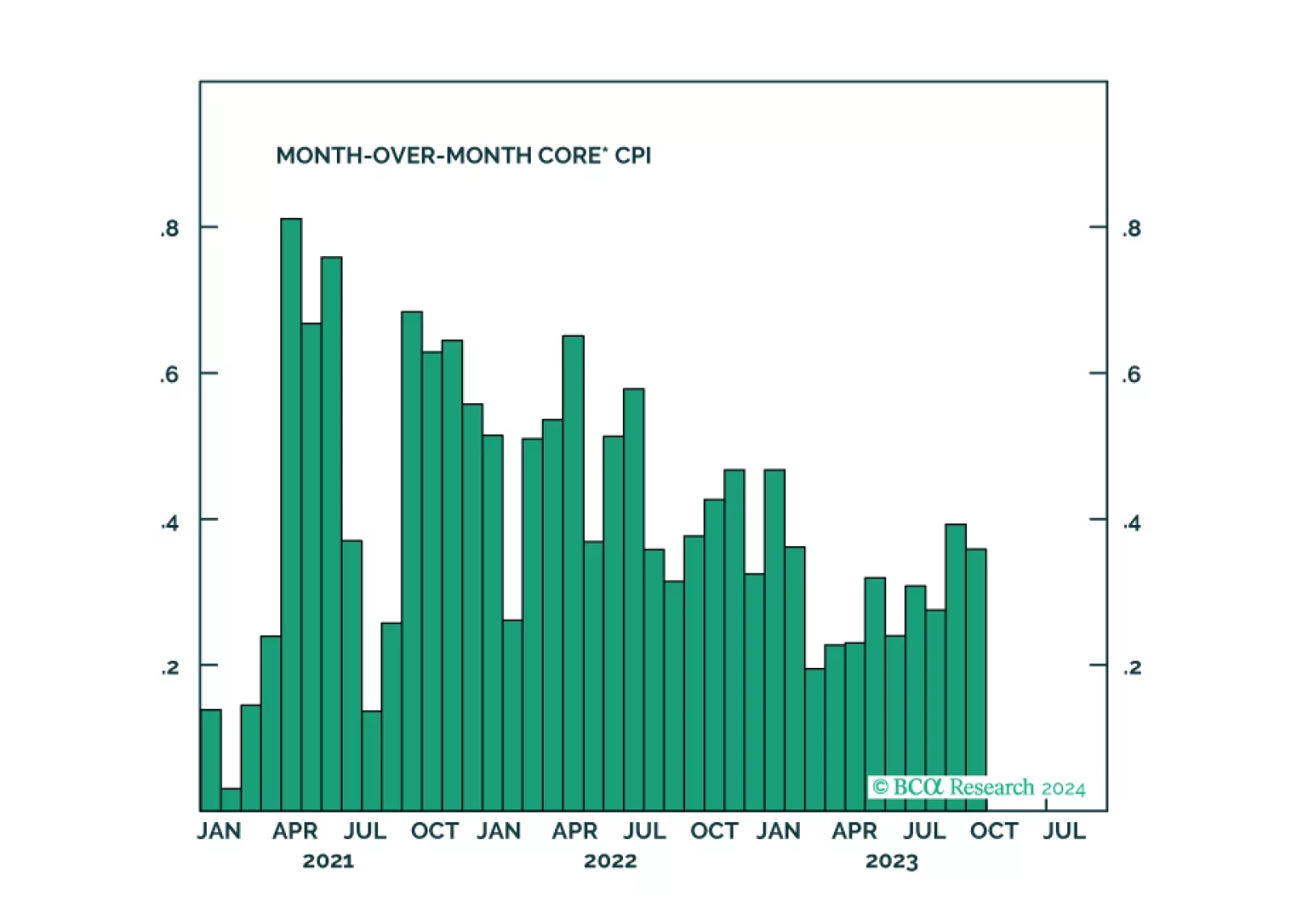

Comments on yesterday’s CPI report and yield moves.

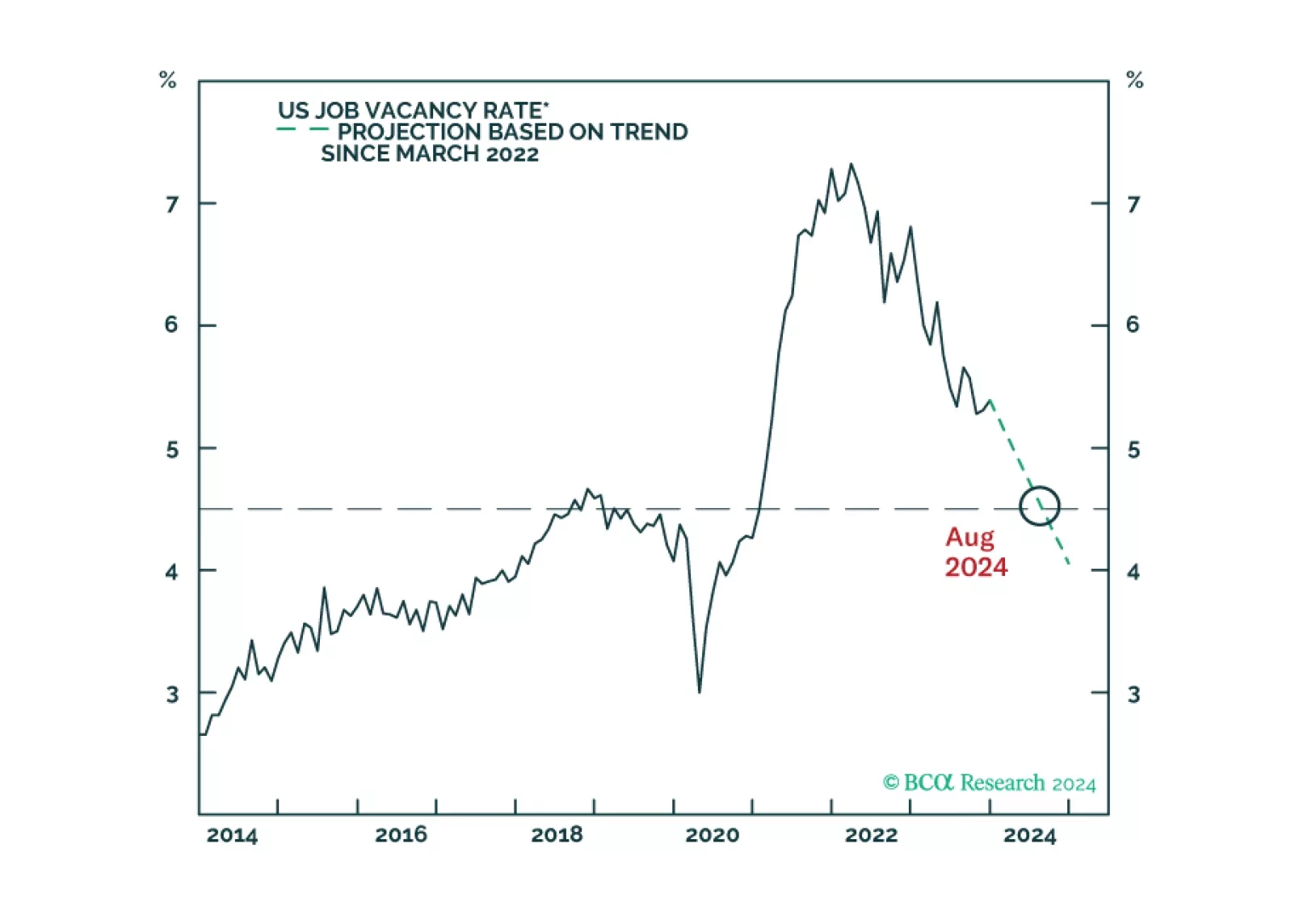

Easier financial conditions, rising home prices, rebounding consumer sentiment, and a stabilization in manufacturing activity all augur well for near-term US growth prospects. An unsustainably low savings rate is a key risk to the US economic outlook. Our revised forecast is centered on a recession starting in late 2024 or early 2025.

Our Portfolio Allocation Summary for February 2024.