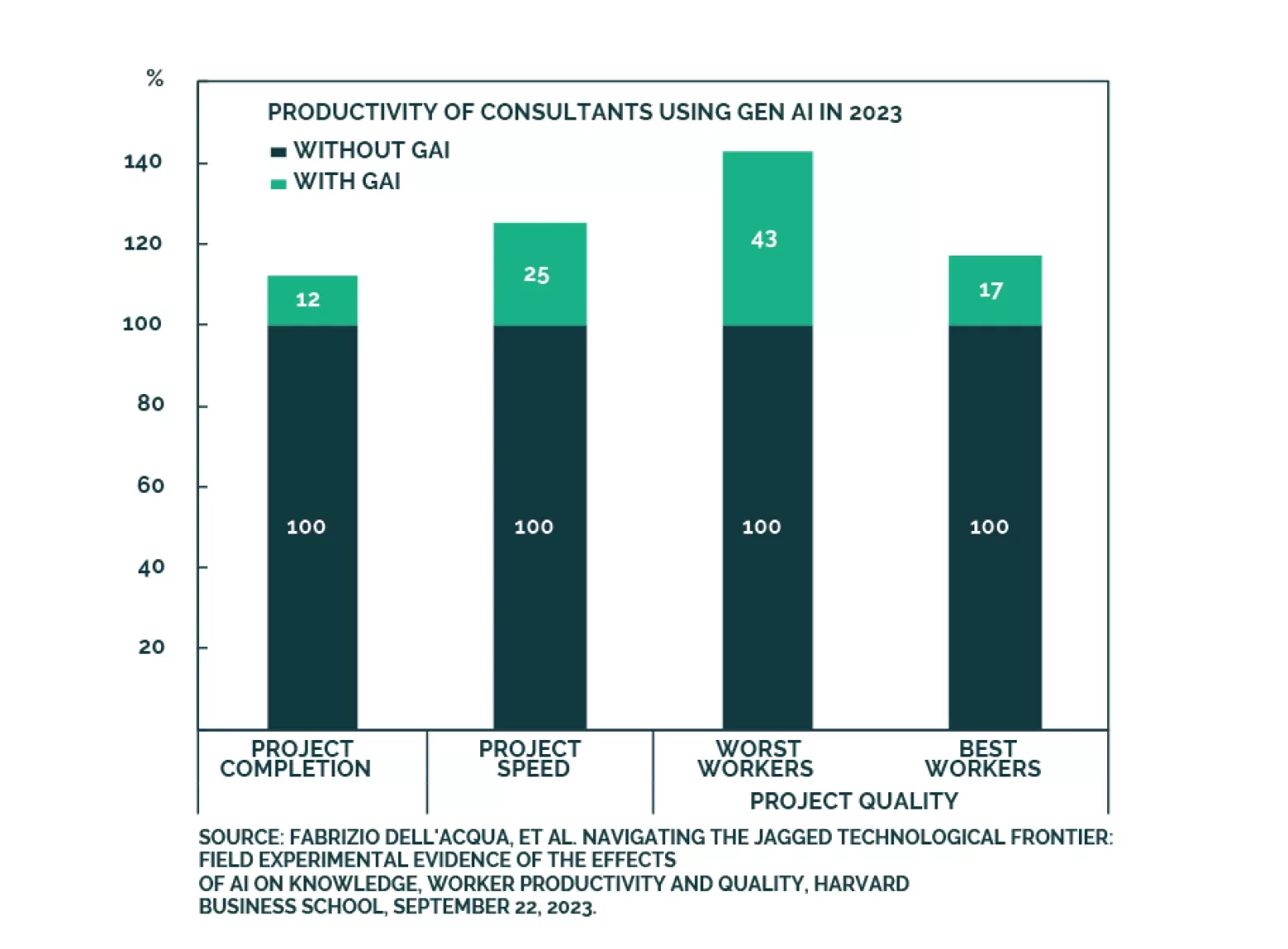

Productivity

In Section I, Doug notes that the chaos of the new administration, including bellicose tariff threats and DOGE’s abrasive and indiscriminate approach, are sowing uncertainty and fortifying economic headwinds. Lowered guidance of prominent retailers, alongside weakening services PMIs, bode poorly for economic activity considering that improving manufacturing PMIs likely reflect tariff frontrunning. A recession remains our base case, suggesting that investors should be underweight stocks within multi-asset portfolios. In Section II, Jonathan presents a checklist that investors can use to confirm whether AI’s purported productivity gains are real. The checklist does not currently suggest that artificial intelligence is meaningfully boosting productivity growth. US equity valuation reflects very significant optimism about AI, underscoring the profound risk facing equity investors if the narrative about AI shifts in a pessimistic direction.

We anticipate decisive tariff measures early in Trump’s second term. In this Special Report, we explore how the costs of higher tariffs might be distributed among foreign suppliers, U.S. importers, and consumers.

US assets and the US dollar should remain resilient relative to global peers over the next 12 months as policy uncertainty, election risk, and geopolitical risk reach a climax. After that, investors should reassess their regional allocation.

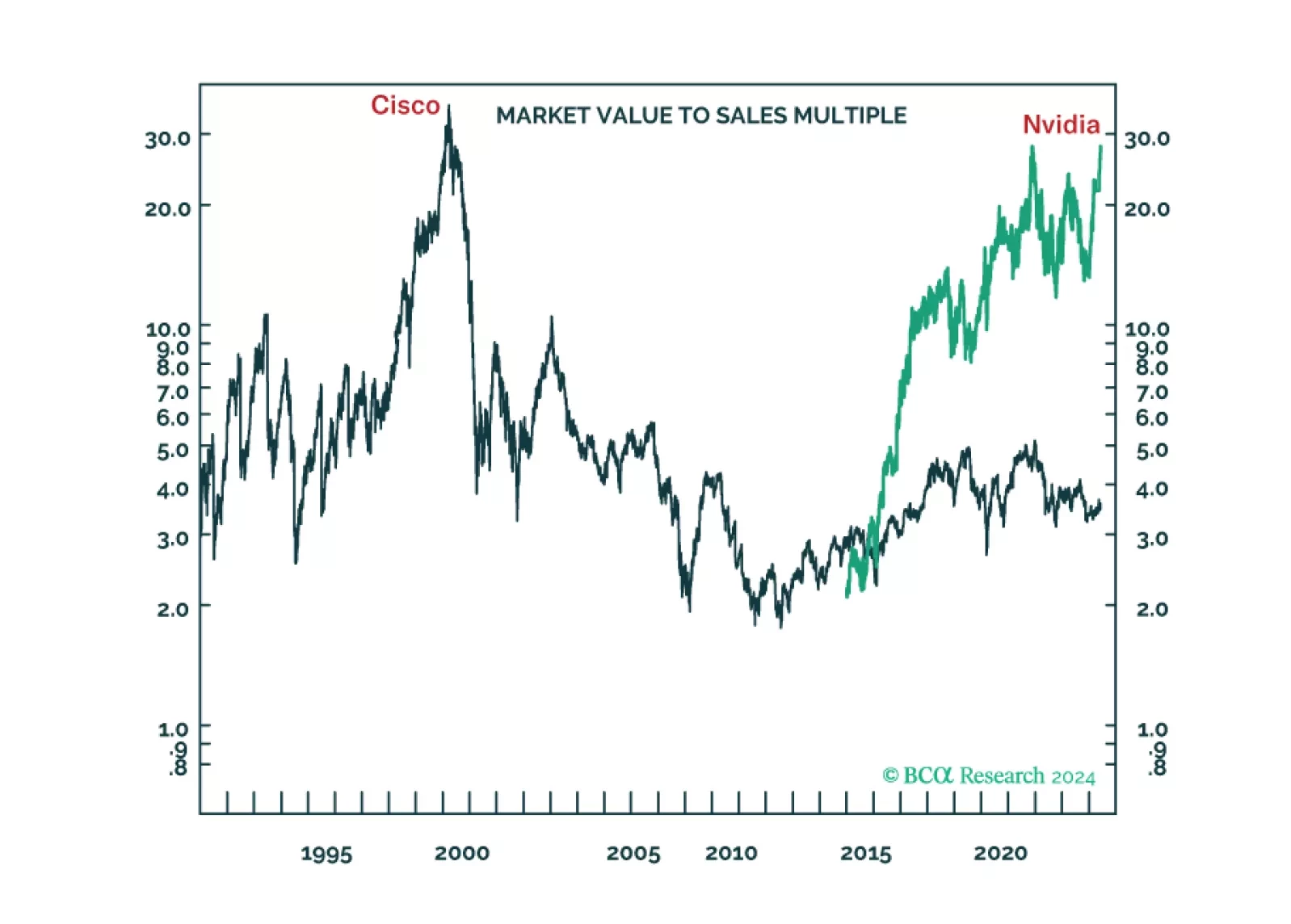

The long-term winners from the generative-AI gold rush are unlikely to be the ‘picks and shovels’ stock Nvidia or the overvalued US superstars of Web 2.0. We discuss the structural investment implications. Plus: time to go tactically overweight global consumer discretionary (RXI).

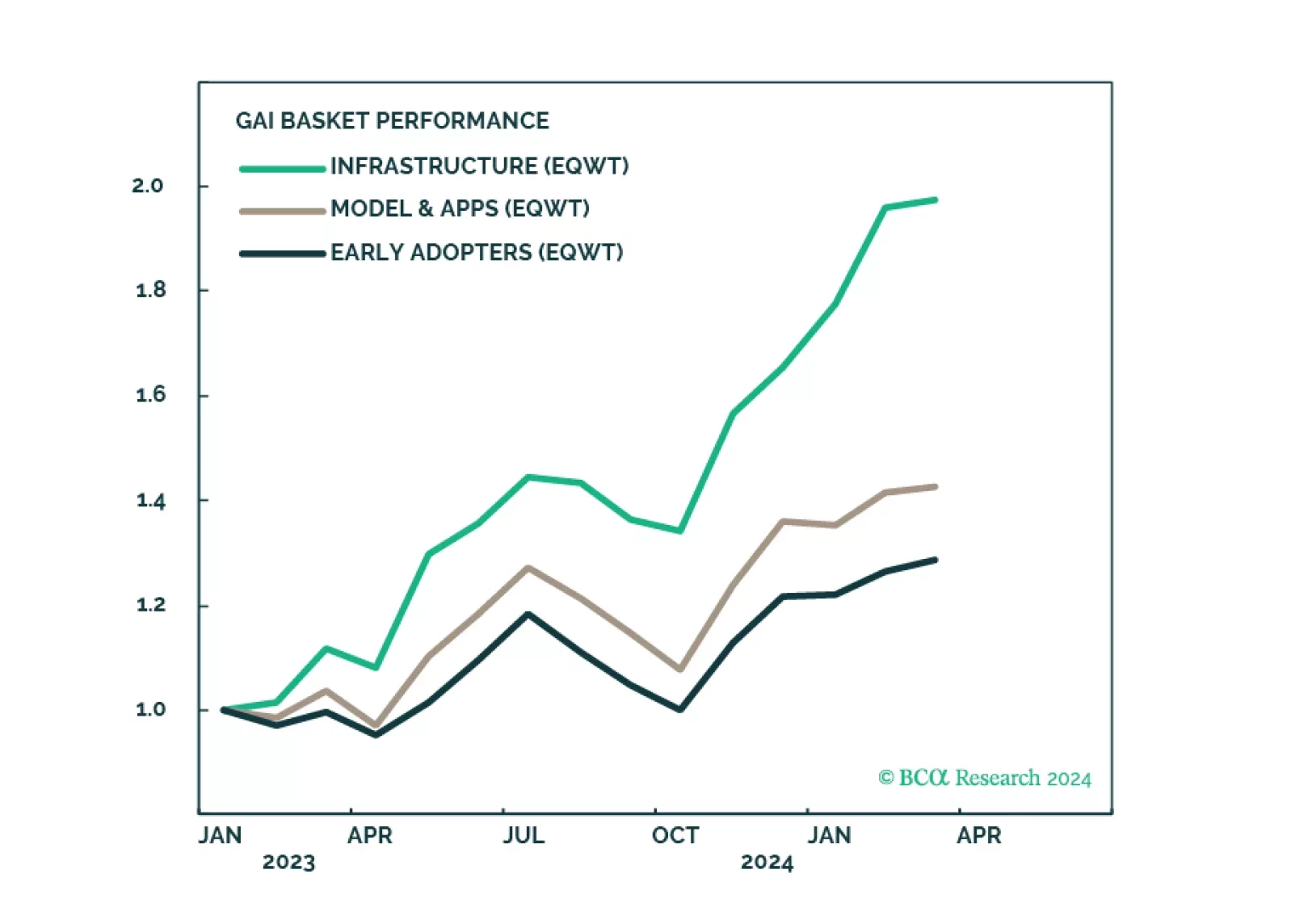

GAI is a powerful force that will revolutionize the global economy and we are sold on this long-term investment theme. To partake in the upward momentum, we recommend a nuanced approach. The GAI infrastructure cohort is now overbought - there should be a better entry point. The models and applications companies and early adopters are less of a crowded trade and offer more opportunities.

GAI technology has made tremendous gains over the past year. It has advanced from being a mere “curiosity” to becoming an everyday helper. While the promise of GAI is enormous, its effects are still limited: Companies are still struggling with monetization while productivity improvement is still at least a year away. In terms of evolution, the focus is shifting away from “picks and shovels” infrastructure companies toward model and application developers.

The US ‘immaculate disinflation’ has run its course, given that labour force participation is topping out. This leaves the Fed with a dilemma. Settle for price inflation stabilising at 3 percent, and cut rates early to avoid higher unemployment. Or, not cut rates early and go the final mile to 2 percent price inflation, at the risk of higher unemployment. We discuss which way the Fed is likely to tilt, and the investment implications. Plus: China is oversold while Japan is overbought.

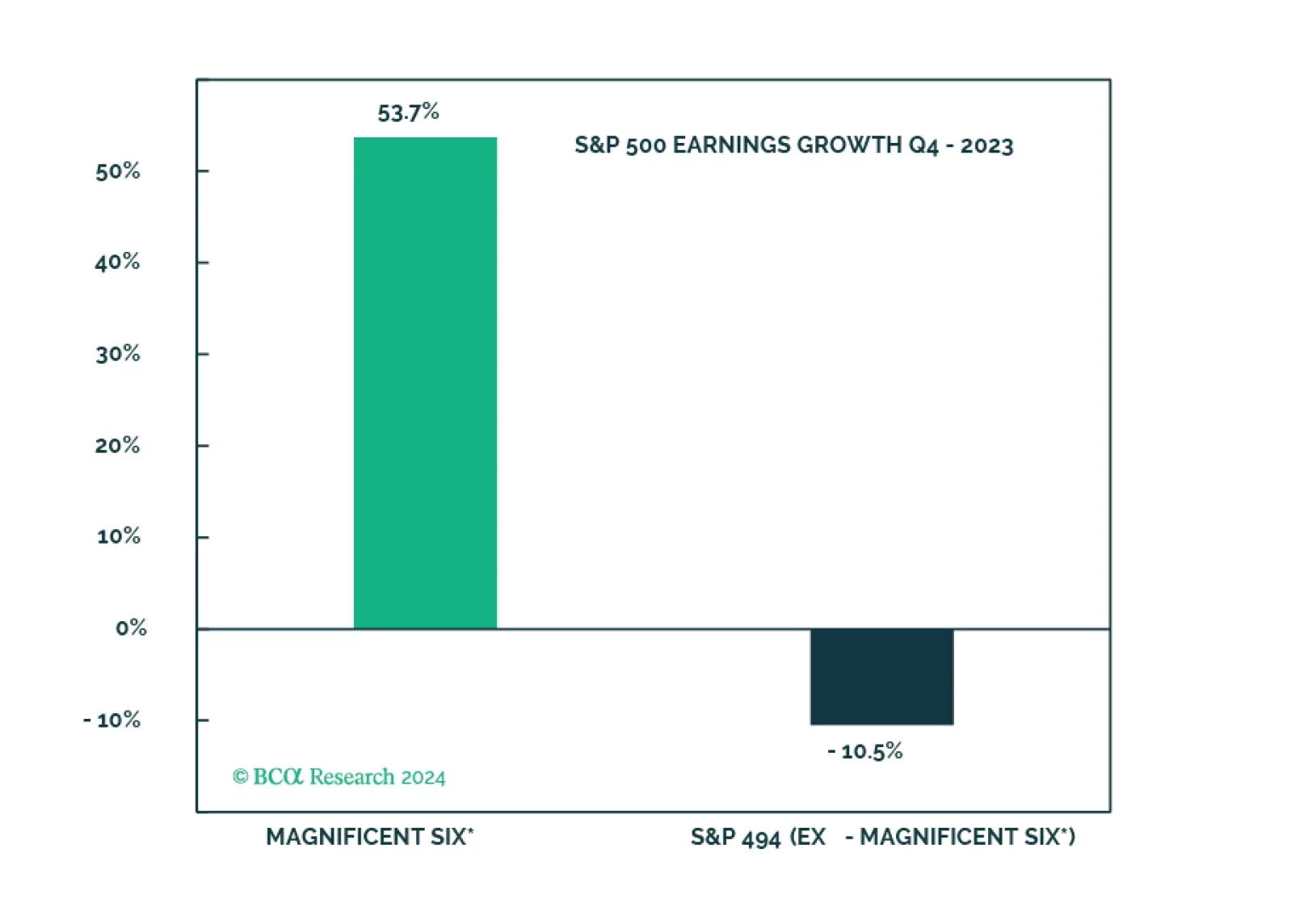

The soft landing and rate cuts narrative is being priced out, and the S&P 500 is overvalued and getting overbought. The Magnificent Seven are about to get a new moniker on the back of performance dispersion. However, without the cohort, S&P 500 earnings would have been even deeper in the red.

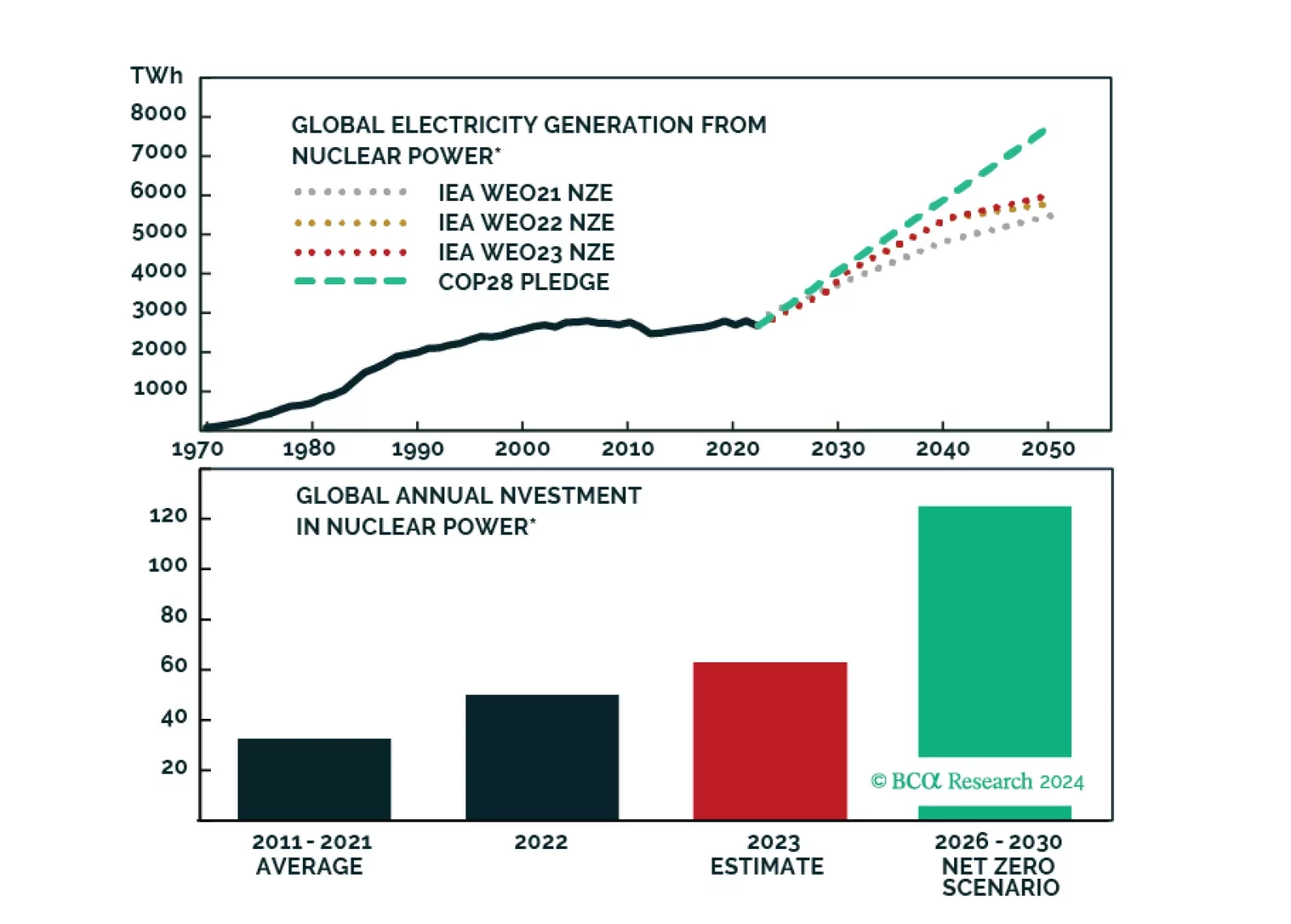

BCA Research presents a limited monthly special series about the Nuclear Renaissance.

Our 2024 outlook can be encapsulated into just 39 words and three key views. Key view 1: The end of China’s housing boom means the end of the world’s main growth engine. Key view 2: If the Fed and ECB don’t kill the economy, they won’t kill inflation. Key view 3: The AI gold rush will struggle to find any gold. We go through the investment implications for the year ahead.