Developed Countries

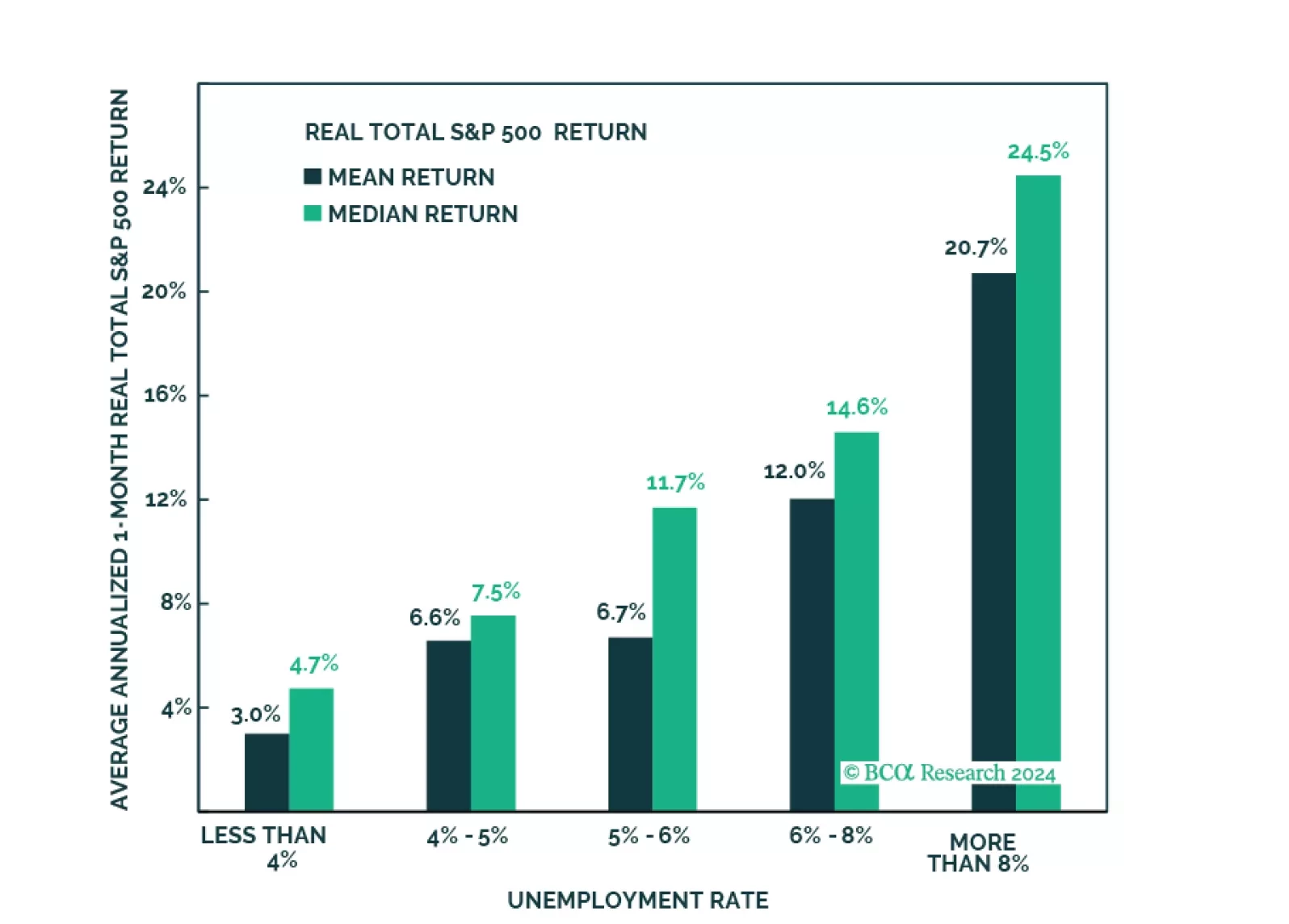

In this Strategy Outlook we examine why, contrary to popular perception, the odds of a global recession over the next 12 months are rising not falling.

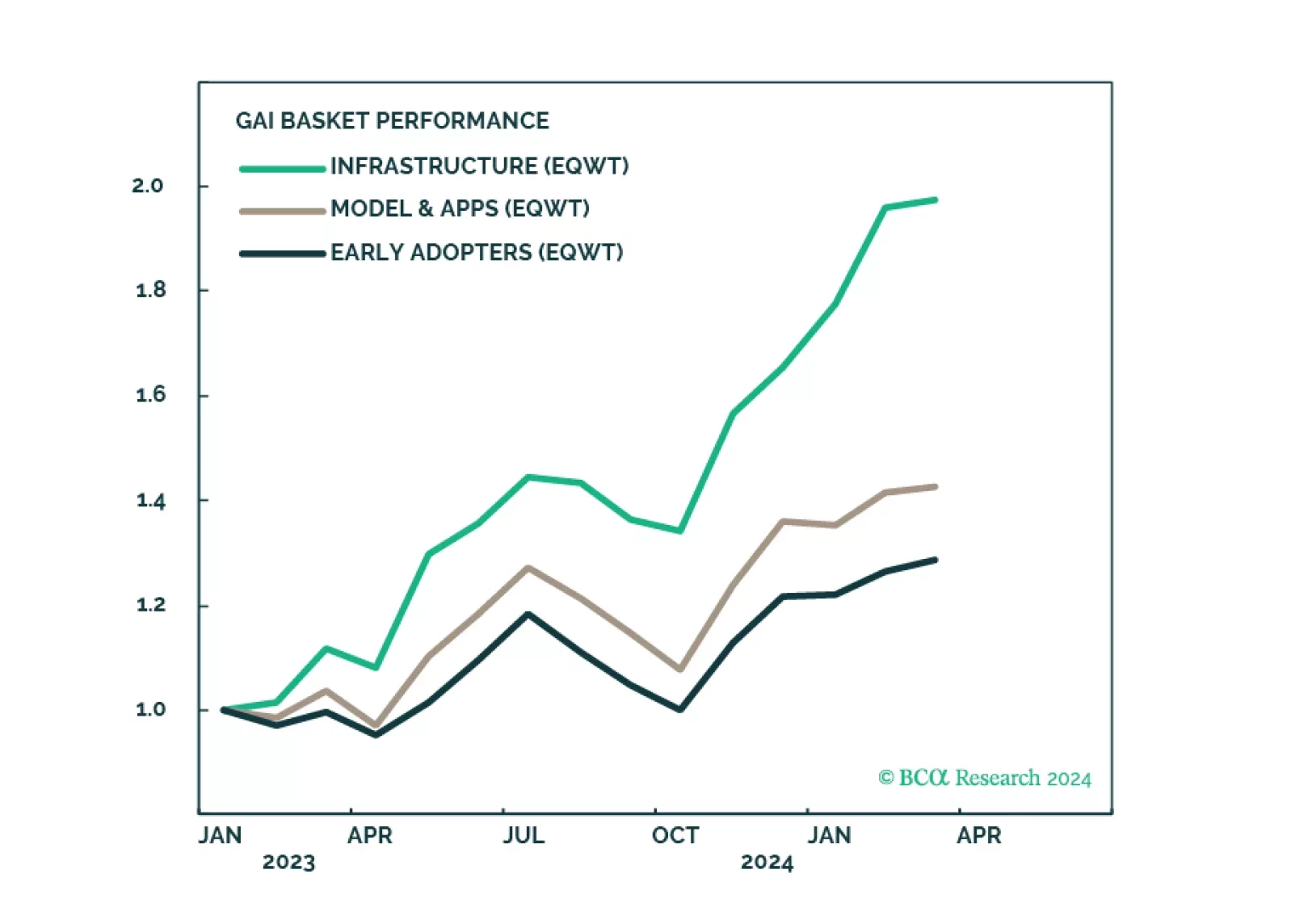

GAI is a powerful force that will revolutionize the global economy and we are sold on this long-term investment theme. To partake in the upward momentum, we recommend a nuanced approach. The GAI infrastructure cohort is now overbought - there should be a better entry point. The models and applications companies and early adopters are less of a crowded trade and offer more opportunities.

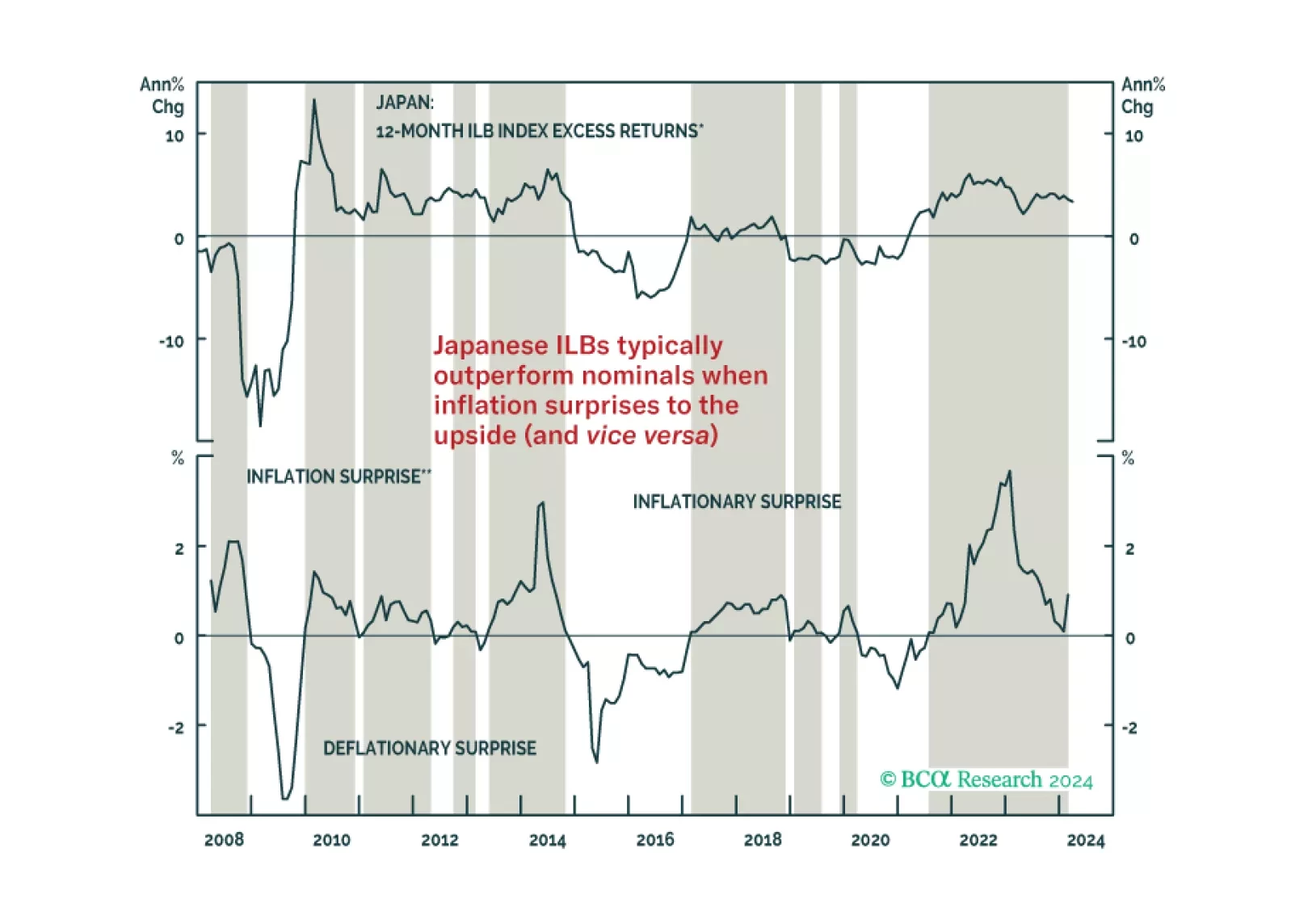

In this Insight, we continue our series of reports outlining investment frameworks for inflation-linked bonds in the developed markets, this time focusing on Japan. Our Japanese Inflation-Linked Golden Rule suggests that investors should overweight Japanese inflation-linked bonds versus nominal JGBs on a strategic (6-12 month) investment horizon. Our new Japanese inflation models suggest that there is a material risk that Japanese inflation exceeds the current level of market-based inflation expectations over the next year.