Emerging Markets

The magnitude of US tech/AI capital spending already rivals past bubble thresholds, threatening hyperscalers’ future returns on capital. There are echoes of previous market tops. Our preferred overlay strategy for equity portfolios remains long semiconductor producers / short hyperscalers.

The rally in Colombia’s financial markets has a short shelf life. The election will bring a right-wing government, but it cannot fix inflation, fiscal arithmetic, or balance-of-payments vulnerabilities. Use the near-term rally to downgrade Colombian fixed income and equities.

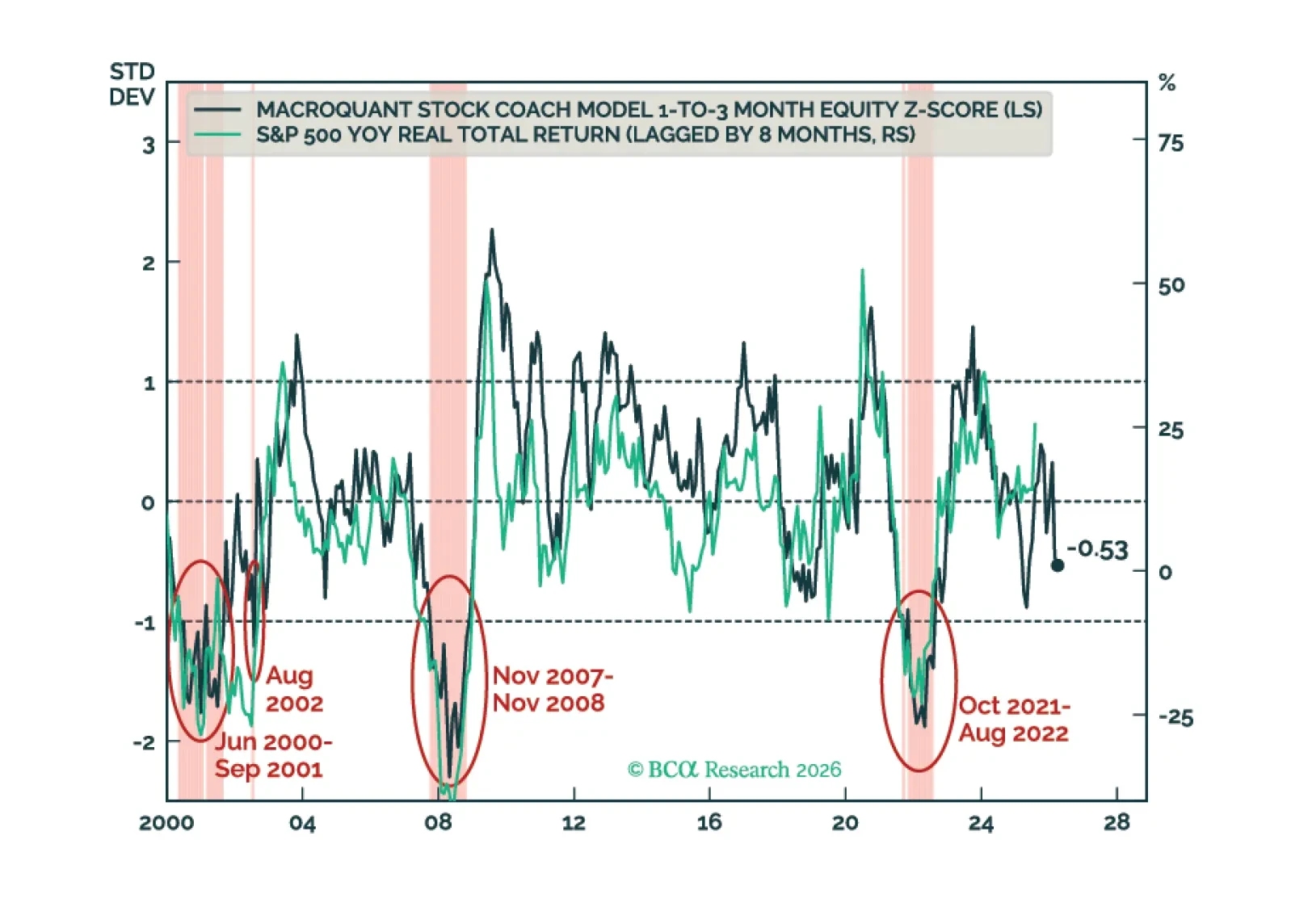

MacroQuant recommends a slight underweight position in equities, favors a below-benchmark duration stance in fixed-income portfolios, is very positive on the US dollar, downgrades gold to underweight, upgrades copper to overweight, and remains very bullish on oil.

US stocks and bonds are on a collision course. Only a meaningful equity selloff is likely to pull bond yields considerably lower. Global equity risk-reward looks poor. The dollar will stay firm near term, but its medium- and long-term outlook remains bearish.

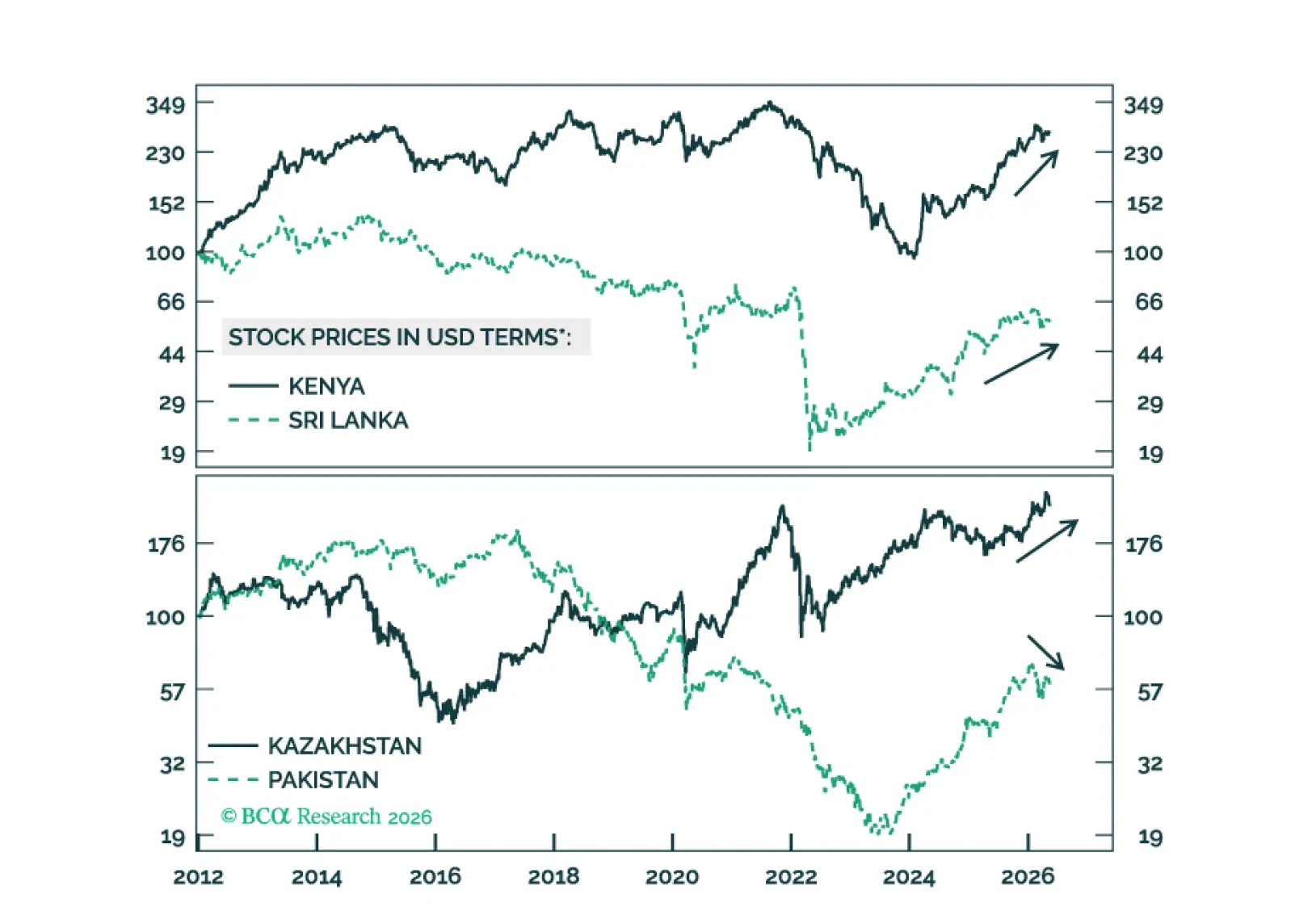

The divergence across frontier markets is likely to widen. Kenya, Kazakhstan, and Sri Lanka are well placed to outperform, while Pakistan is vulnerable. We offer several trade ideas to capture this divergence.

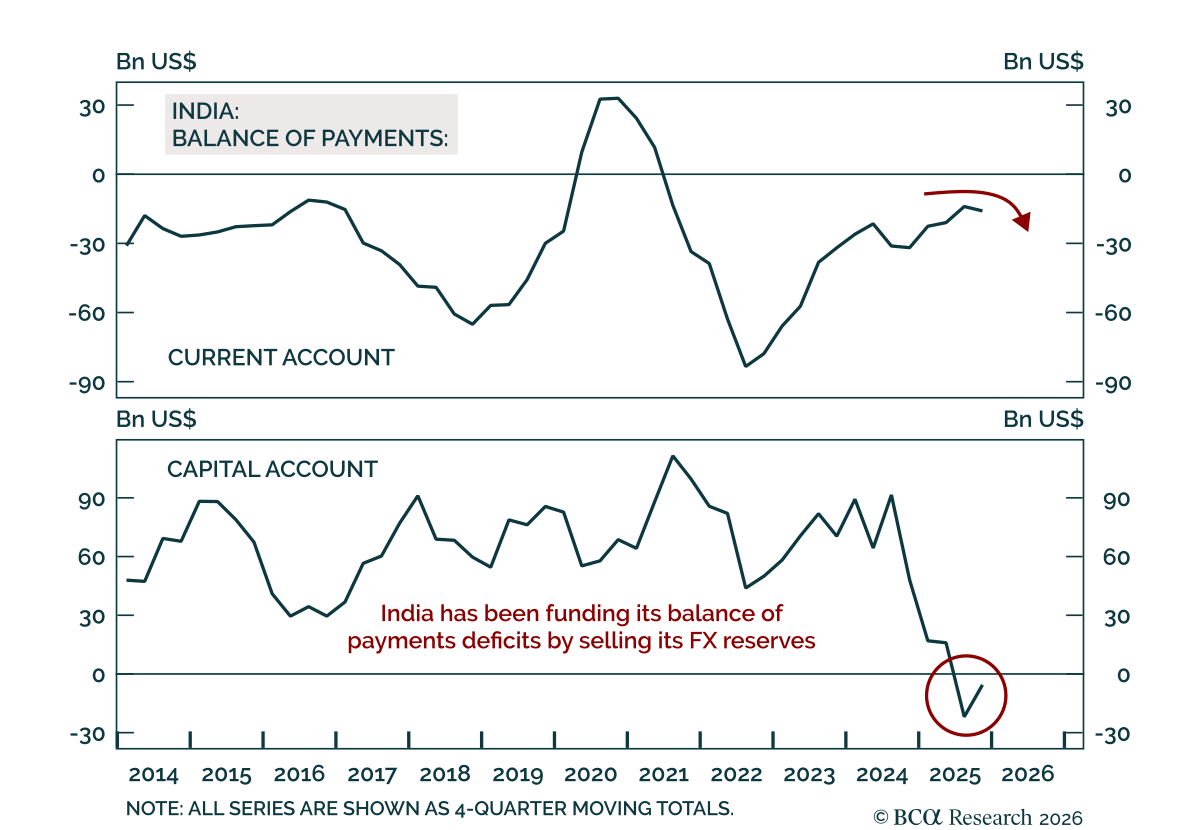

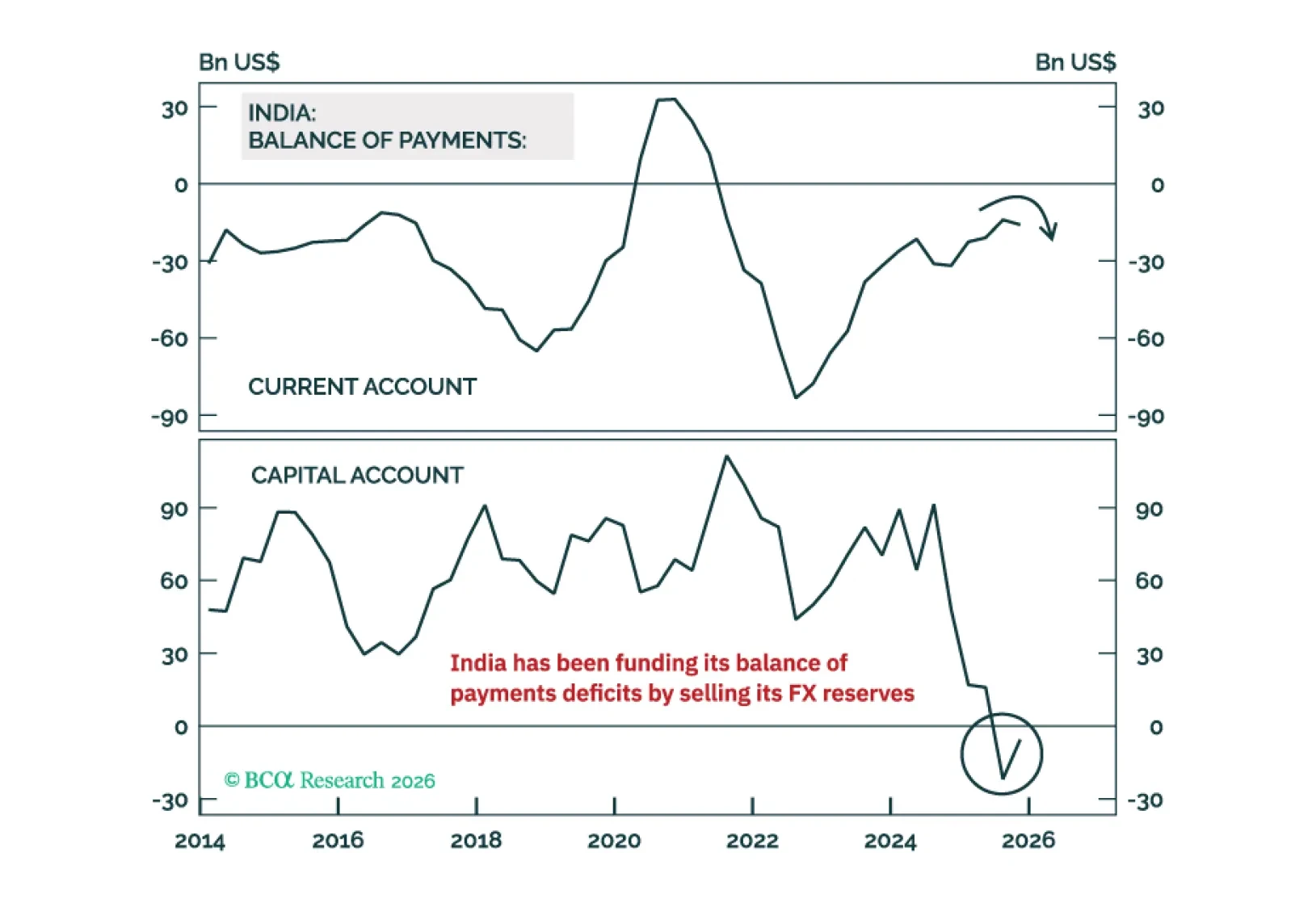

India is probably the most vulnerable among the G-20 economies should the Strait of Hormuz not reopen fully by the end of this month. Growth will slow, while inflation will rise materially. Investors should brace for further weakness in the currency and stock prices.

MacroQuant recommends an underweight position in equities, favors a below-benchmark duration stance in fixed-income portfolios, is neutral-to-slightly positive on the US dollar, remains neutral on gold, upgrades copper to neutral, and is very bullish on oil.