Equities

Unlike most advanced economies that are flirting with recession due to weak demand, the ‘inverted’ US economy is motoring along due to strong supply, from a combination of surging labour participation and surging immigration. We go through the implications for stocks, bonds, interest rates, and the dollar. Plus: IXJ, PEP, and MCD are good tactical outperformance candidates.

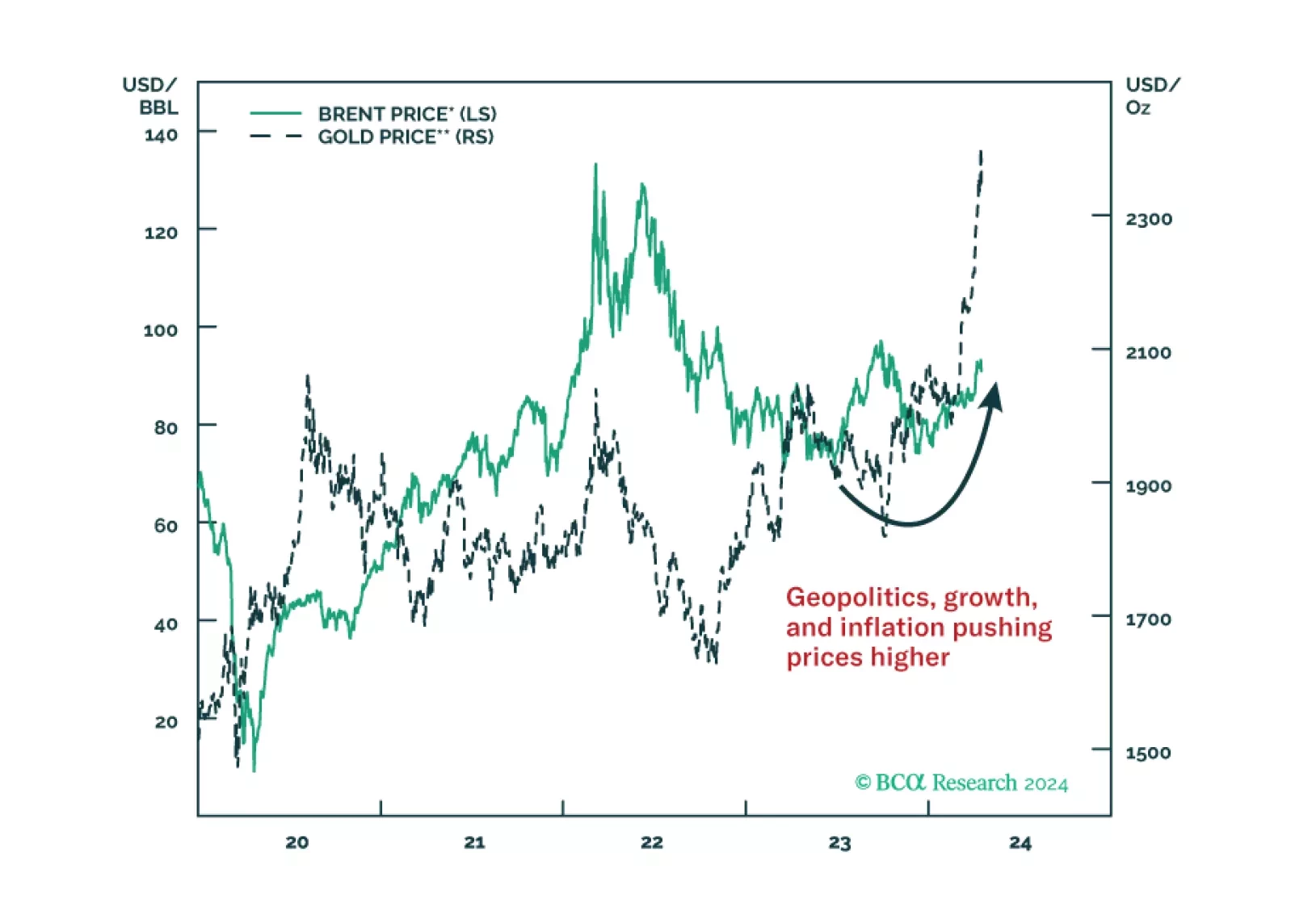

In the near term, favor oil and oil producers outside the Gulf Arab states. Over a 12-month horizon, favor US and North American equities, defensive sectors over cyclicals, and safe-assets. Within cyclicals, stick to energy and defense.

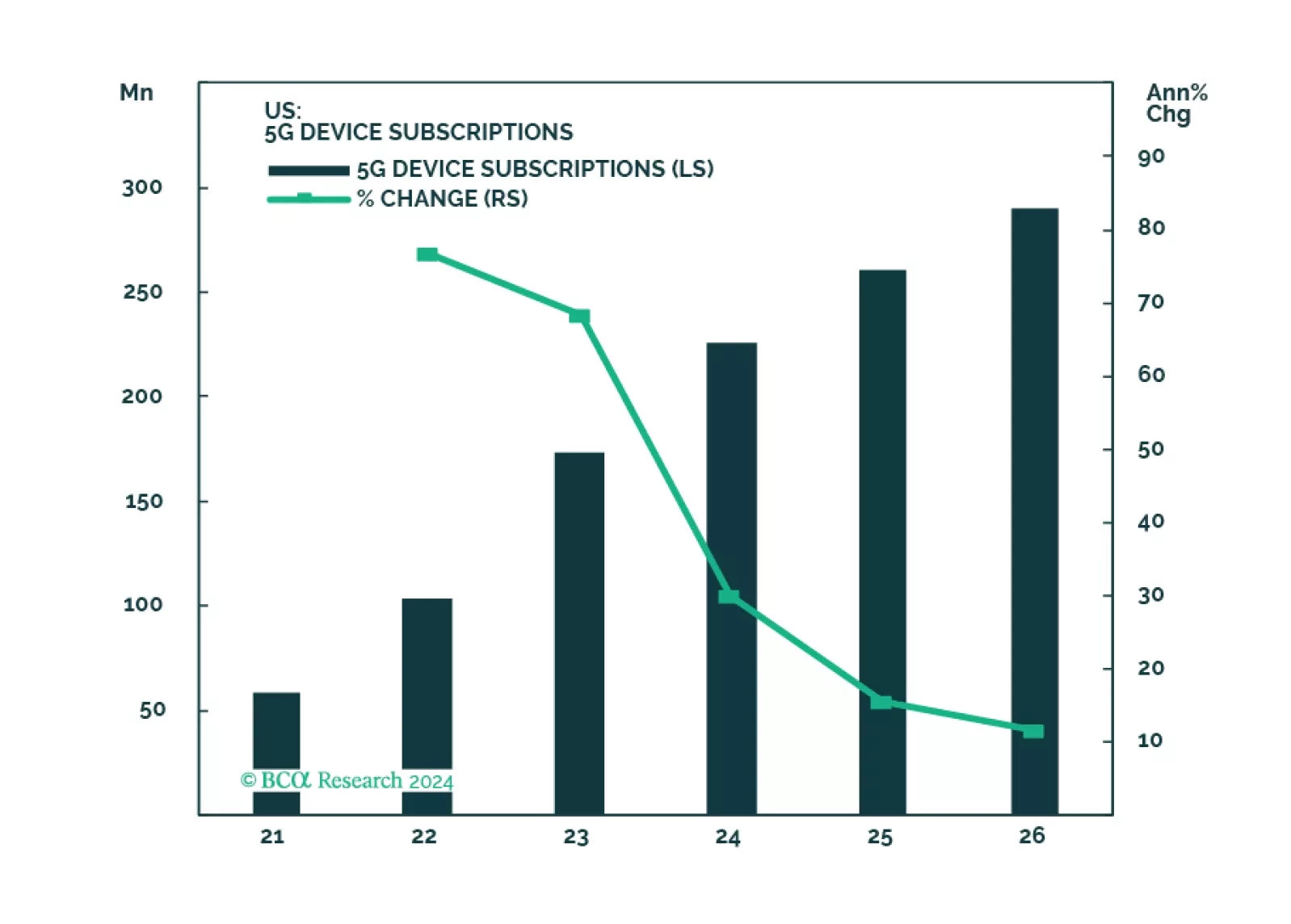

The Telecoms industry is highly concentrated, and carriers compete on price and quality of service in a slow growing market. Demand for capex is relentless. The roll out of 5G has disappointed. Recently, capex outlays have slowed, and operating cash flow has rebounded. Further, Telecoms is a quintessential defensive industry that will outperform during a market pullback.

In the short run, global risk assets are vulnerable due to rising oil prices and bond yields. Cyclically, a global economic downturn will weigh on global risk assets.

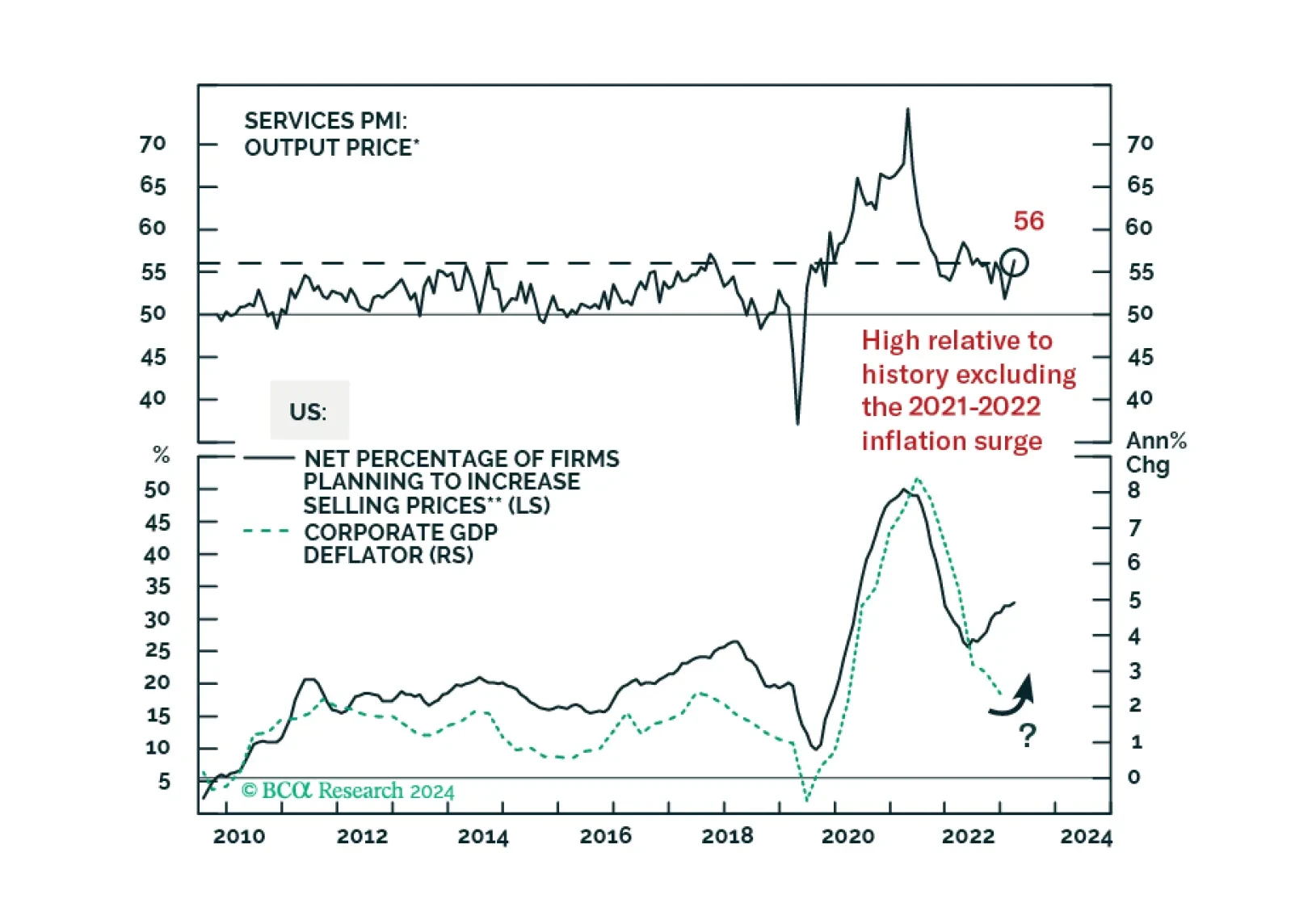

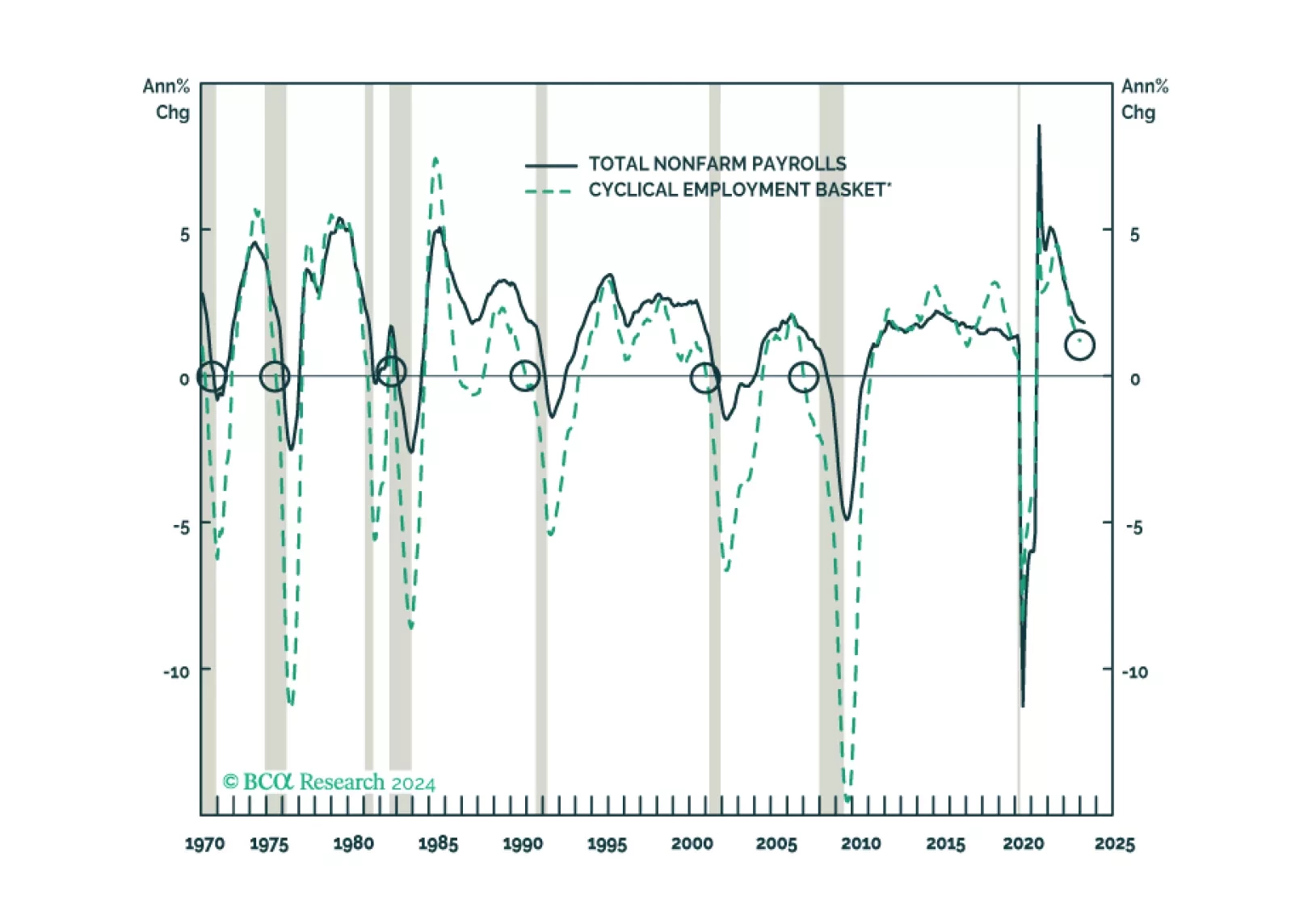

We look beneath headline data to assess the state of the labor market in cyclical goods-producing industries that have previously led overall nonfarm payrolls and in the services segments that have recently been leading the charge. The bottom-up view looks a lot like the top-down view: the labor market is softening, but very slowly, and offers no indications that a recession is at hand.