US Election

As part of our new and improved GeoMacro service, please find attached our Global Risk Outlook, a quarterly digest of scenario probabilities and estimated market impacts for all the major geopolitical topics in the world today.

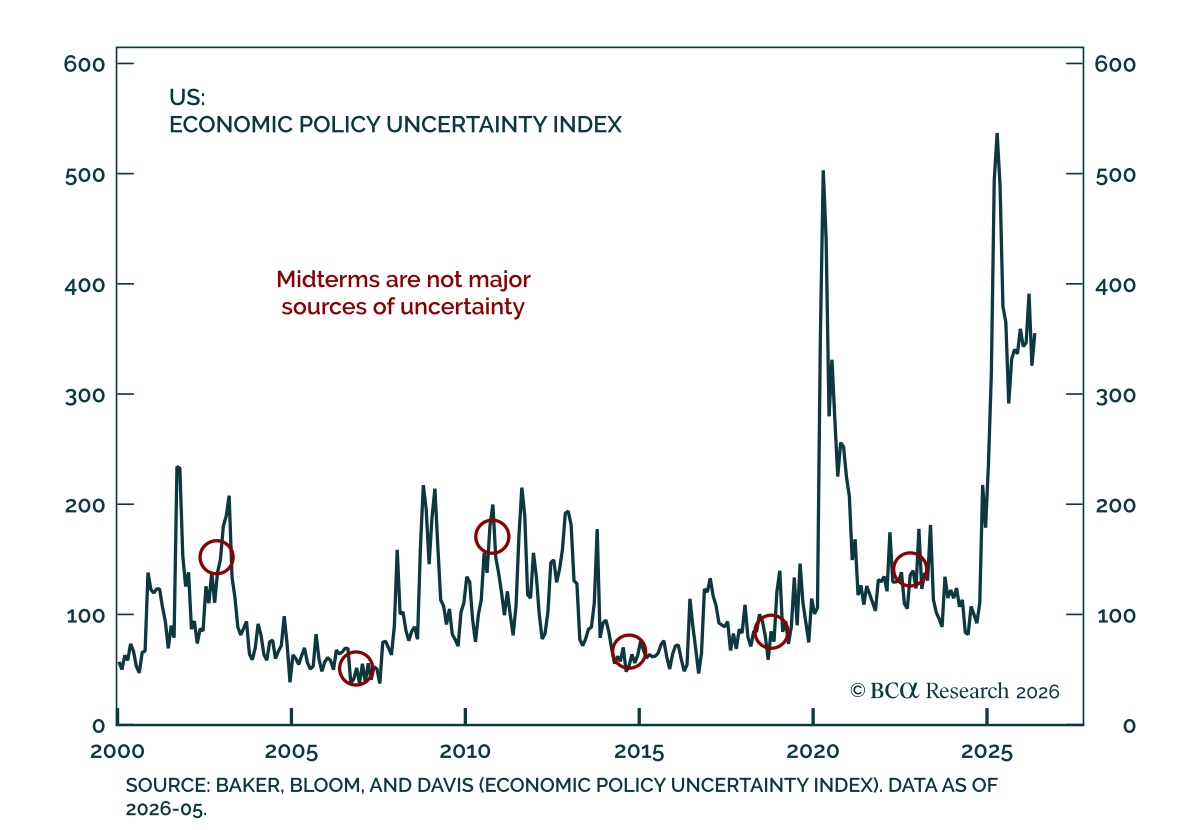

Midterms matter but geopolitics are the main risk this year. Markets will eventually refocus on geopolitical and inflation risks, raising Fed rate hike odds and supporting US dollar and stocks over global counterparts this year.

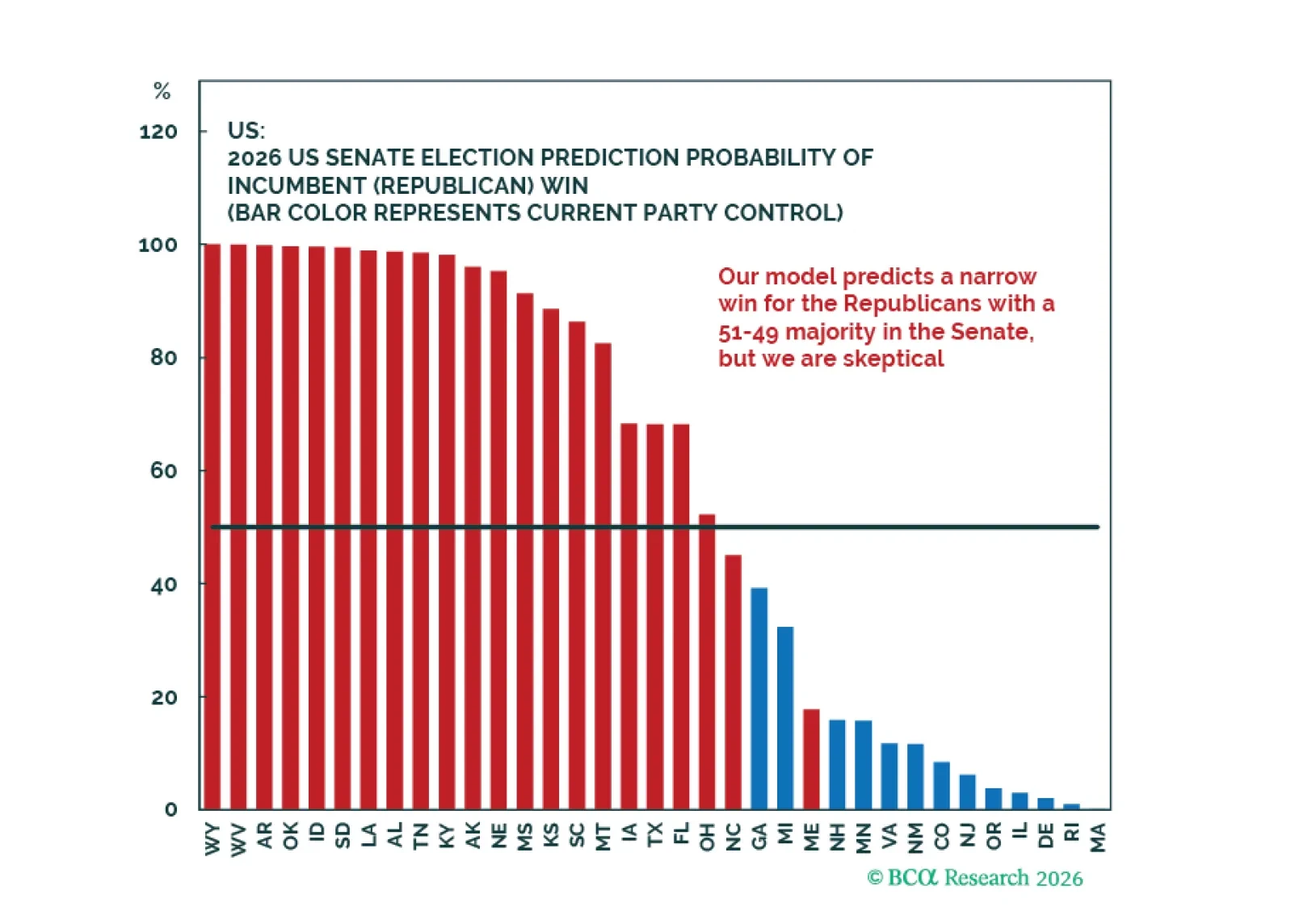

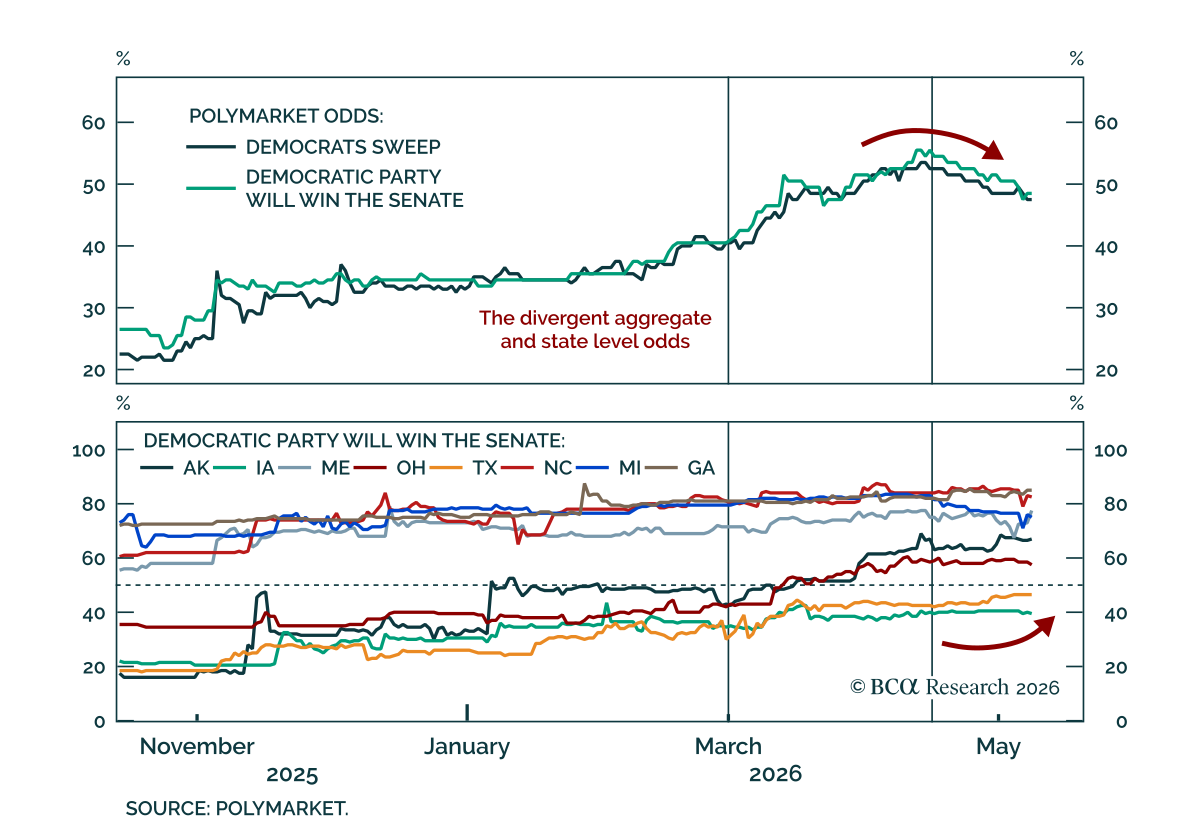

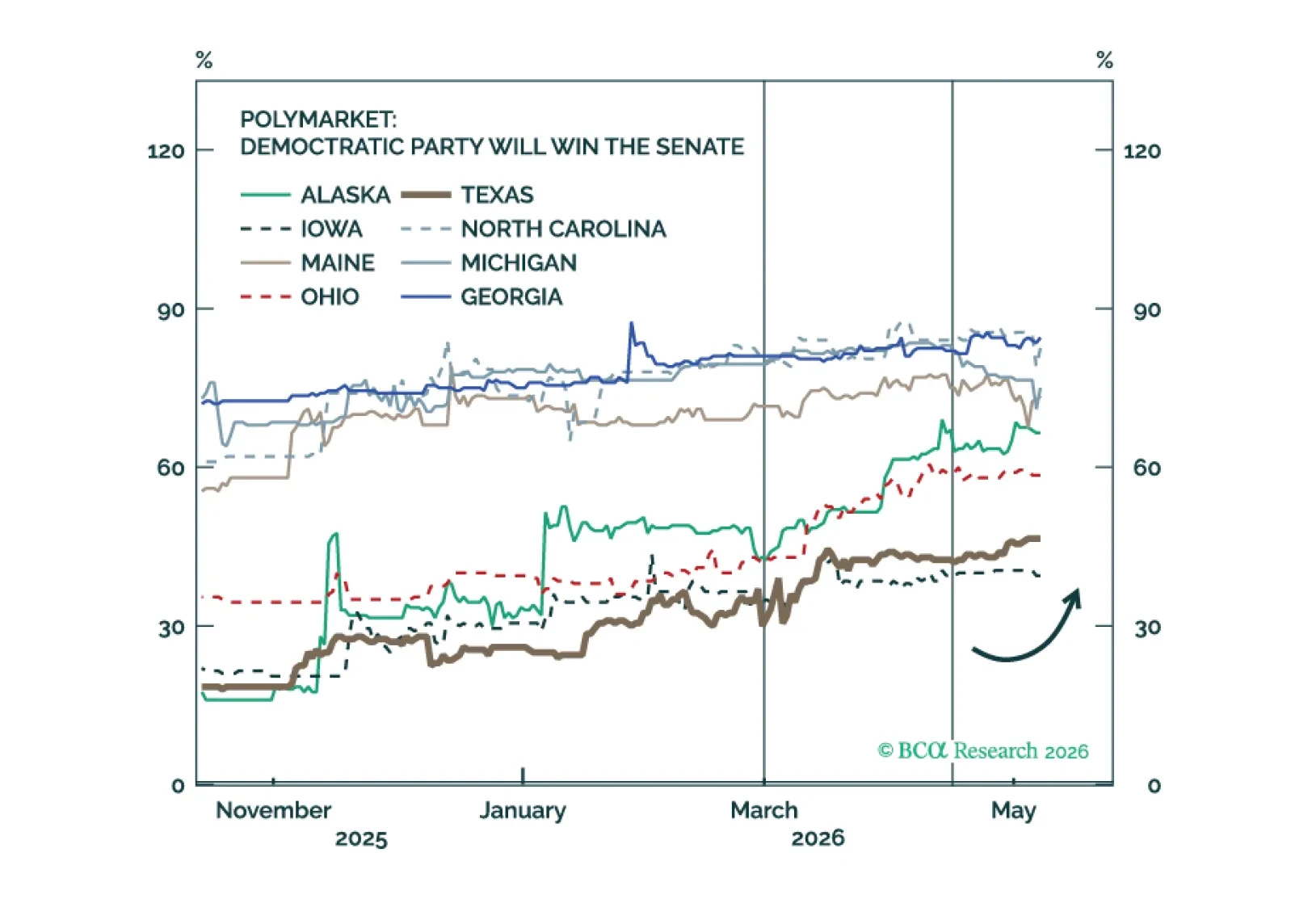

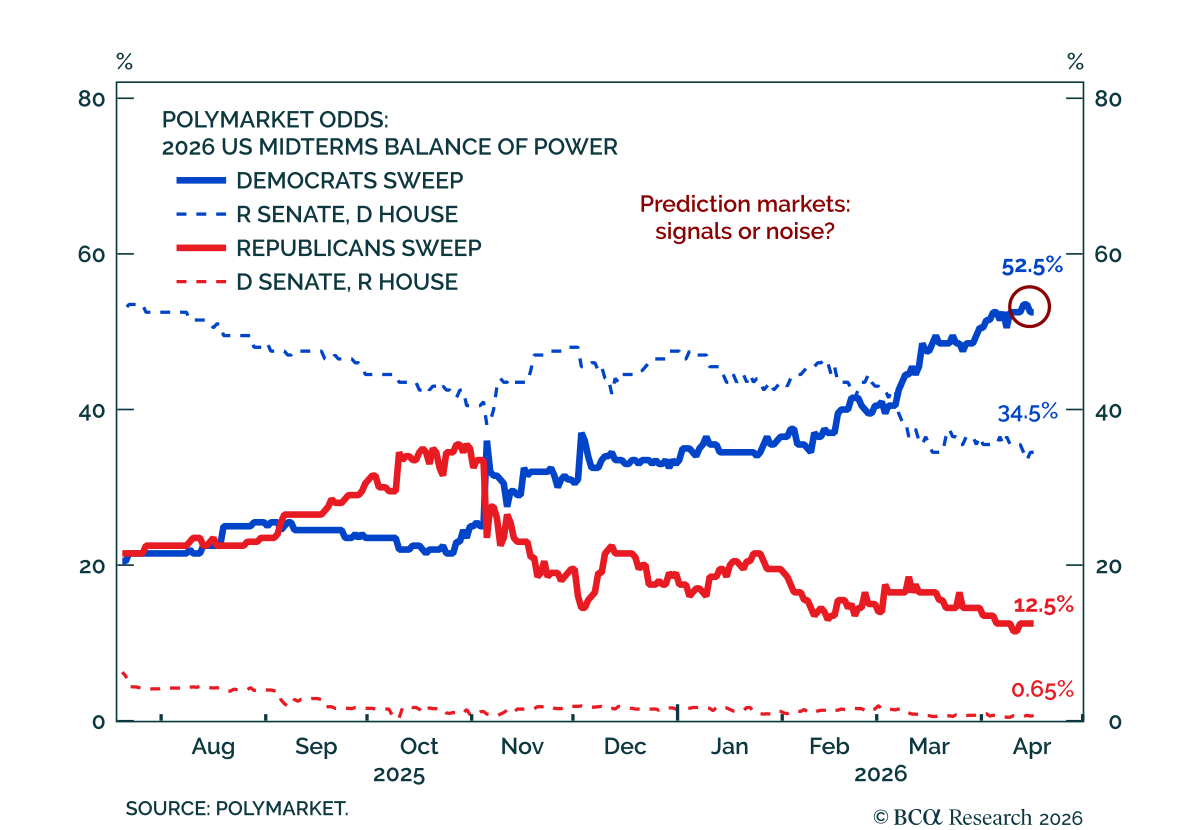

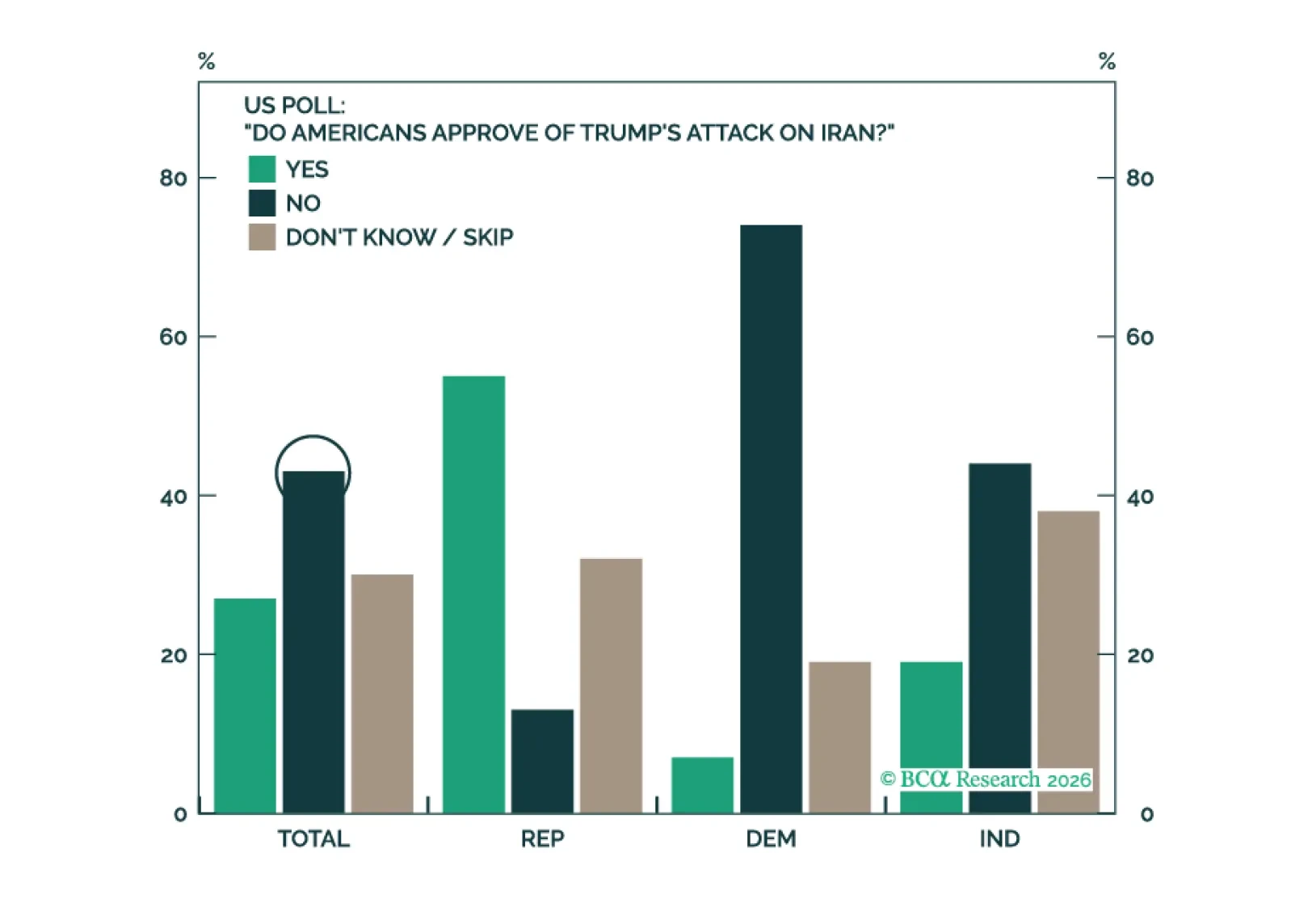

Aggregate Senate betting market pricing appears too pessimistic on Democrats relative to state-level odds and early polling, suggesting a potential mispricing and a relatively sanguine attitude towards the still-unresolved conflict in Iran and its aftermath.

Markets may be underpricing a bifurcated political outcome. Unless the Iran deescalation succeeds, the delayed economic fallout from the energy shock could materially worsen Republican prospects and raise the probability of a Democratic Senate victory.

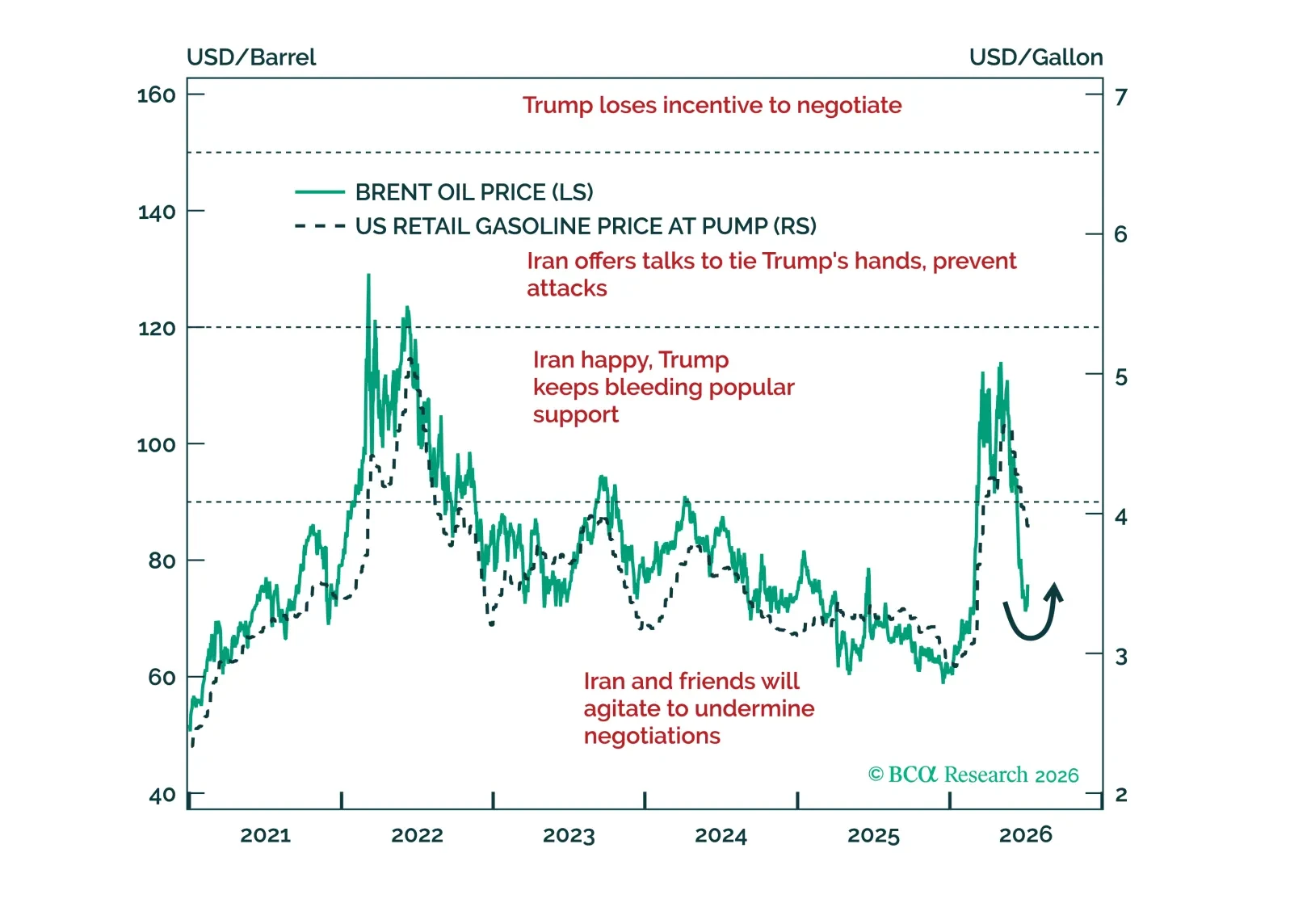

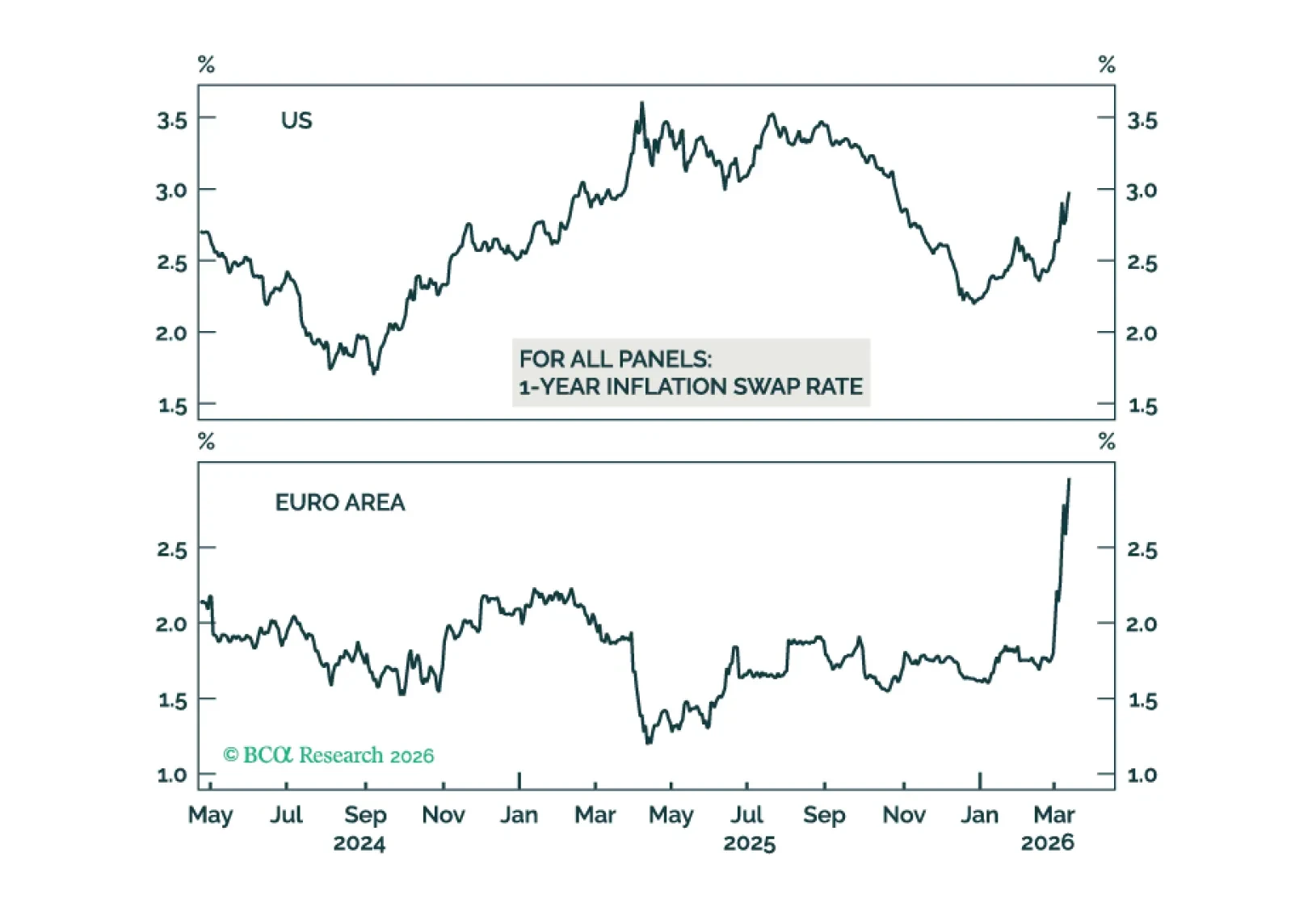

The spike in oil and gas prices has raised the odds of a global economic downturn. Combined with a more negative signal from our MacroQuant model, this warrants tactically downgrading stocks from neutral to underweight. Looking further ahead, the Iran war will lead to bigger defense budgets and a greater focus on energy self-sufficiency.

An energy price spike caused by a Middle Eastern war almost guarantees that Republicans will lose control of the House, and the chance of a Democratic Senate victory increases from 35% to 40%.

President Donald Trump’s political capital is moderate, as he frontloaded his most disruptive policies within the first year.