Developed Countries

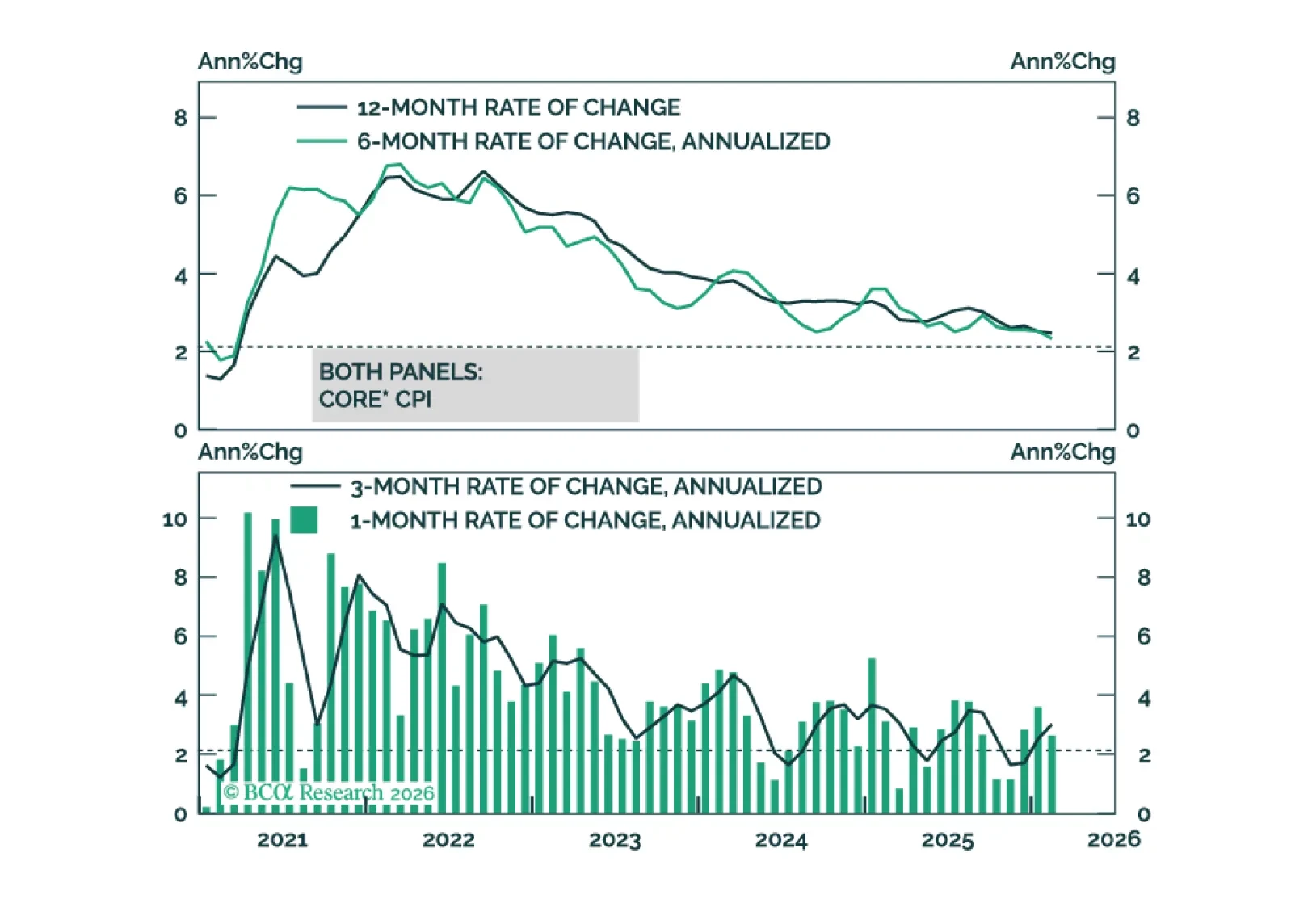

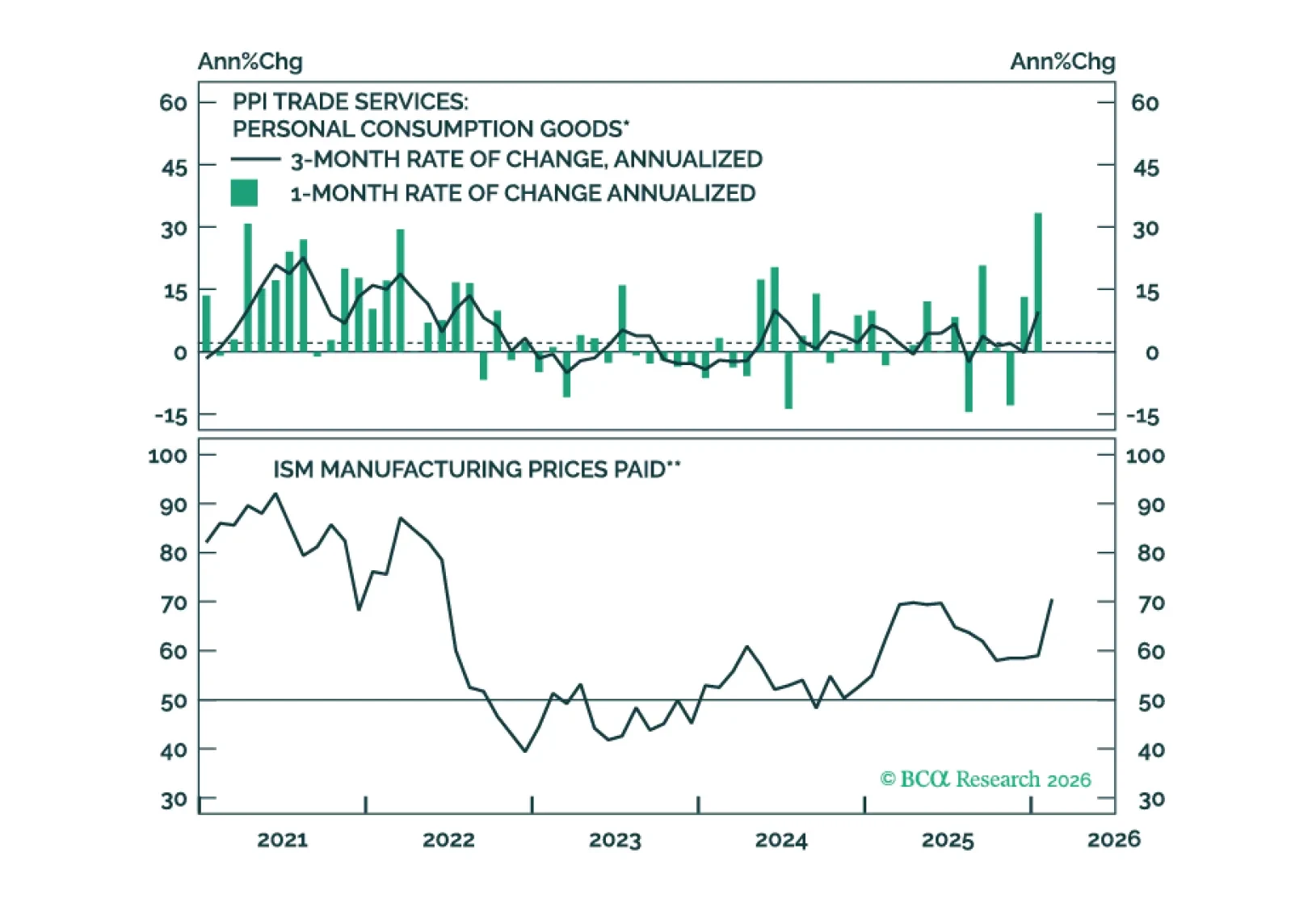

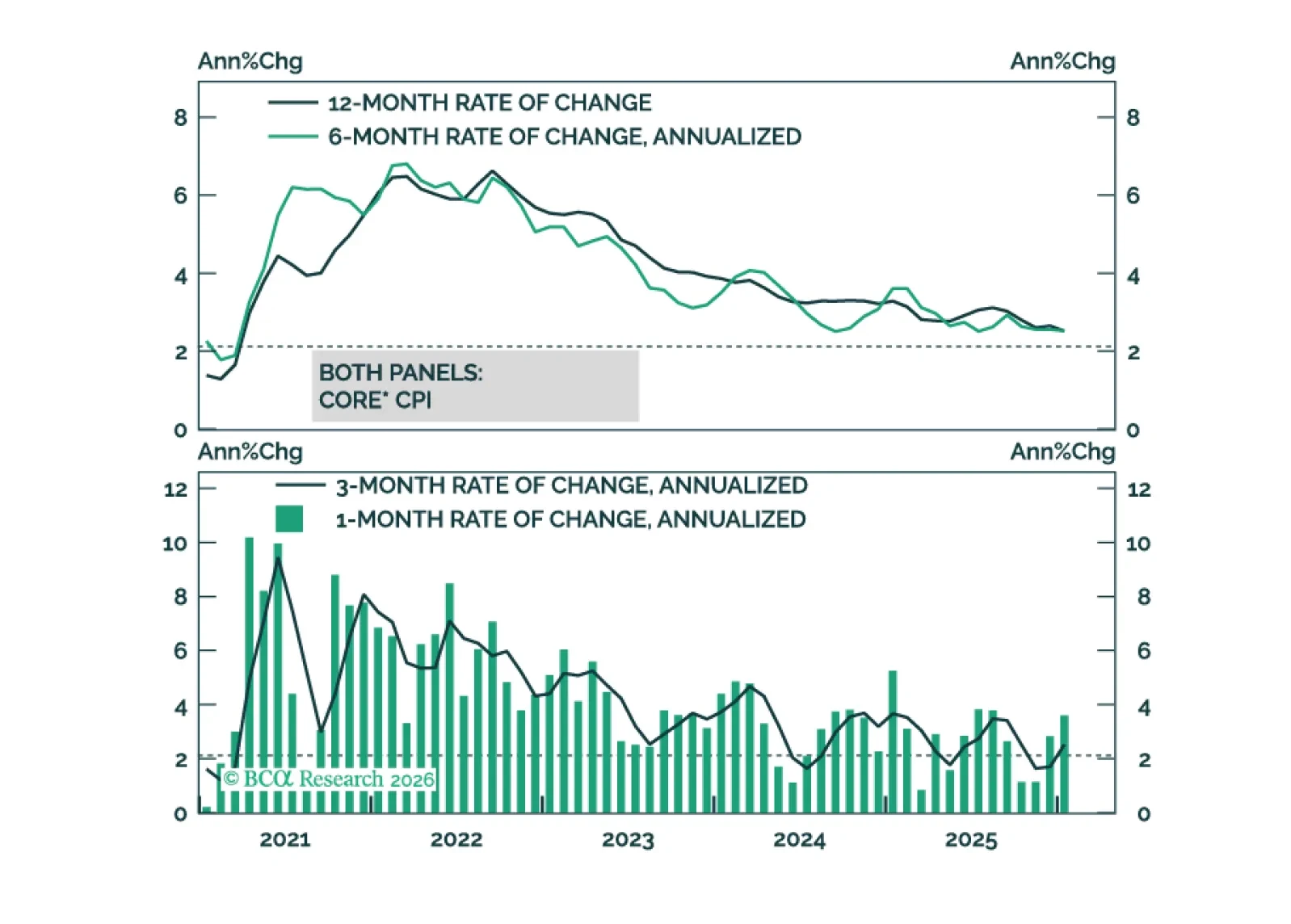

The recent oil price shock reinforces our view that inflation will surprise to the upside during the next few months but fall rapidly in H2 2026.

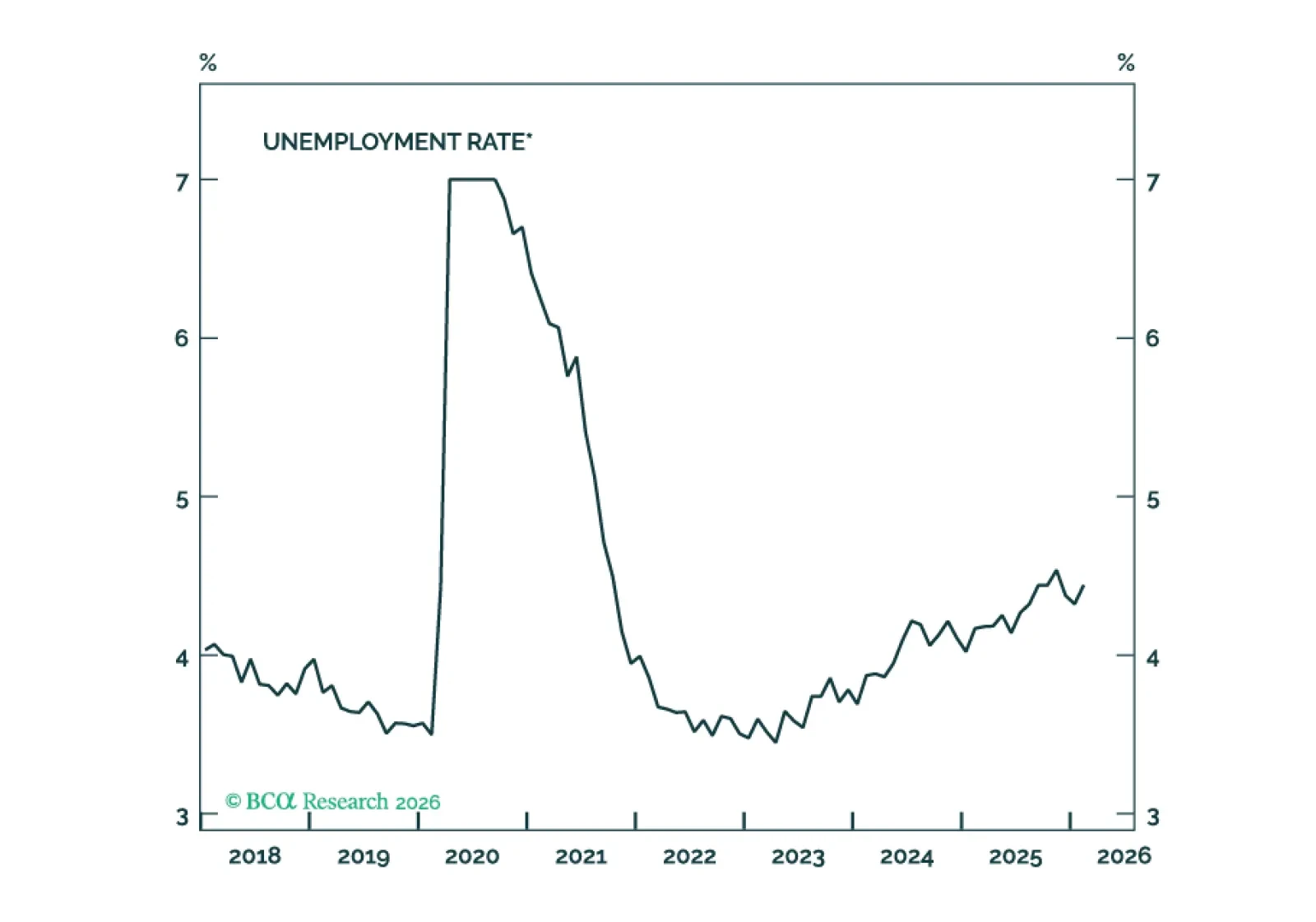

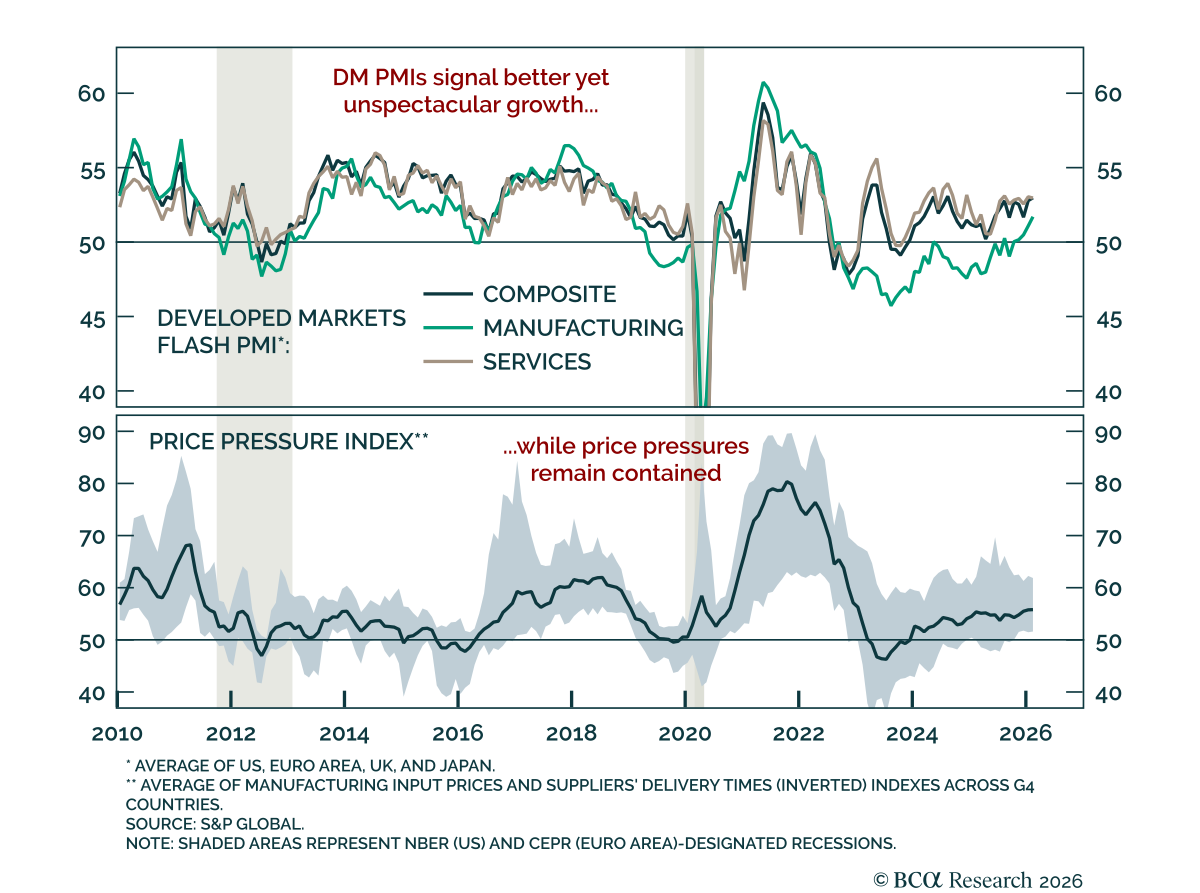

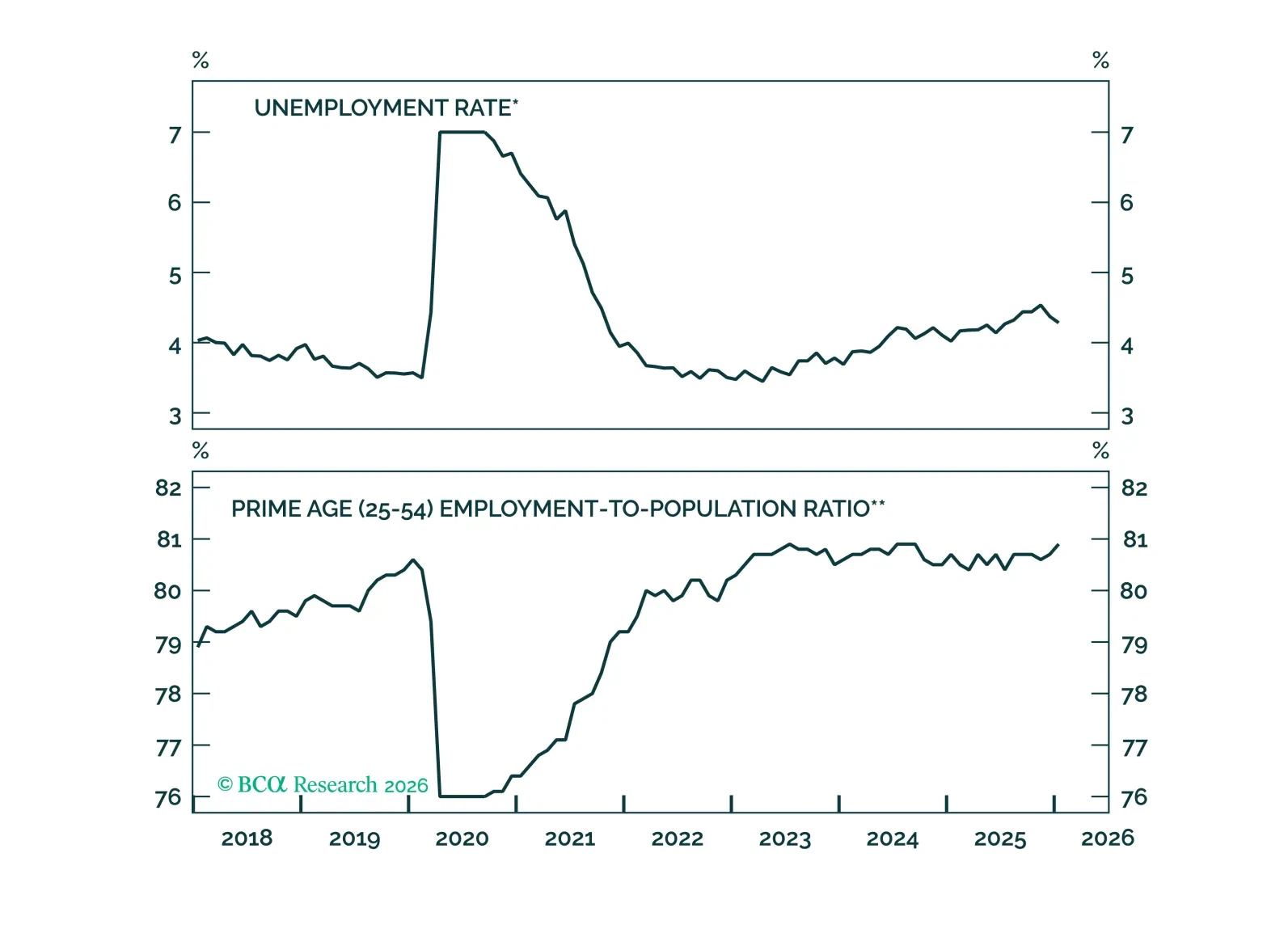

Looking through month-to-month volatility, job growth’s underlying trend is stable and consistent with a flat-to-slightly higher unemployment rate.

Our Portfolio Allocation Summary for March 2026.

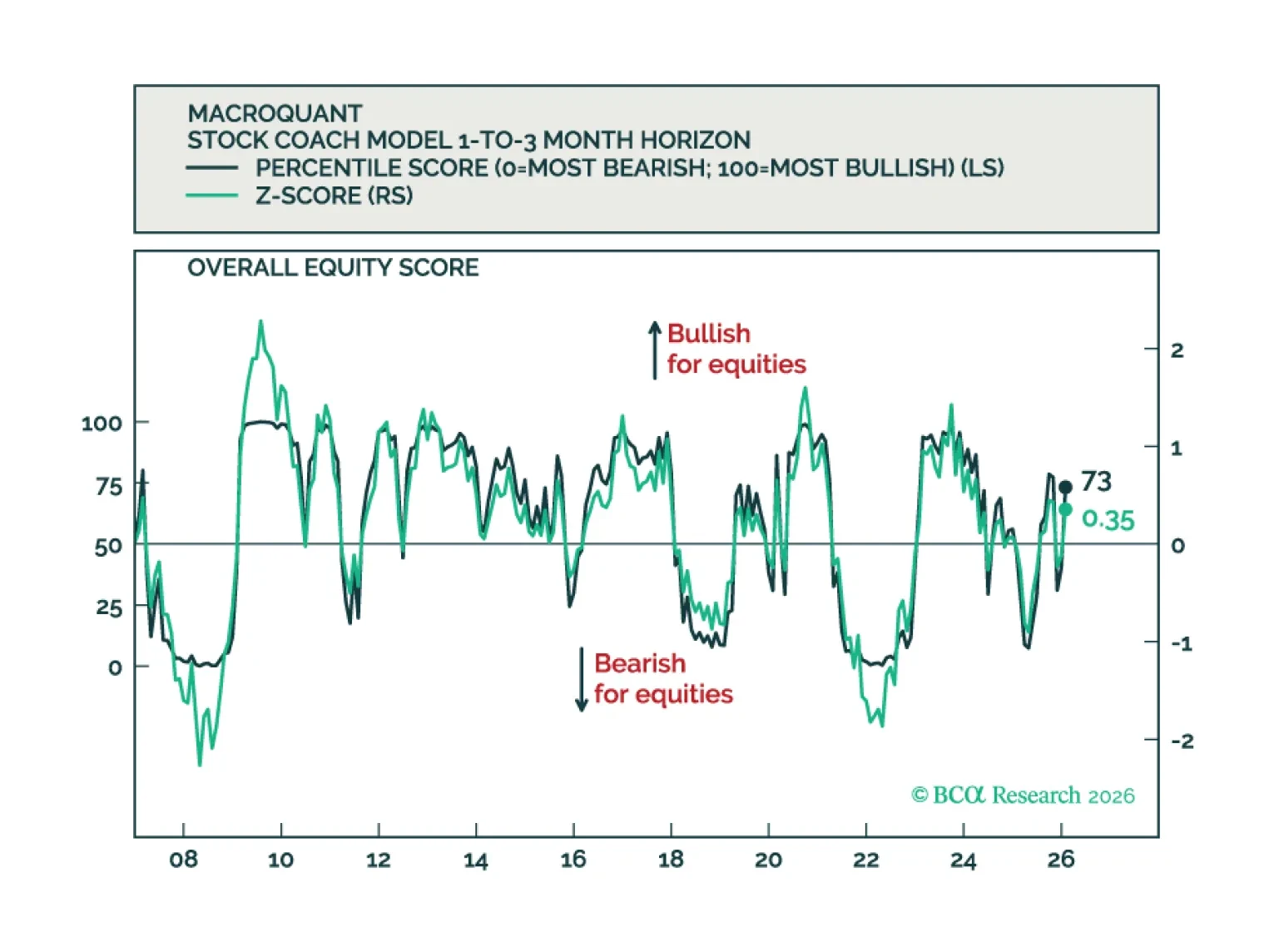

MacroQuant recommends a modest overweight position in equities, favors an above-benchmark duration stance in fixed-income portfolios, remains bearish on the US dollar, has downgraded oil to neutral, and is bullish on copper and gold.

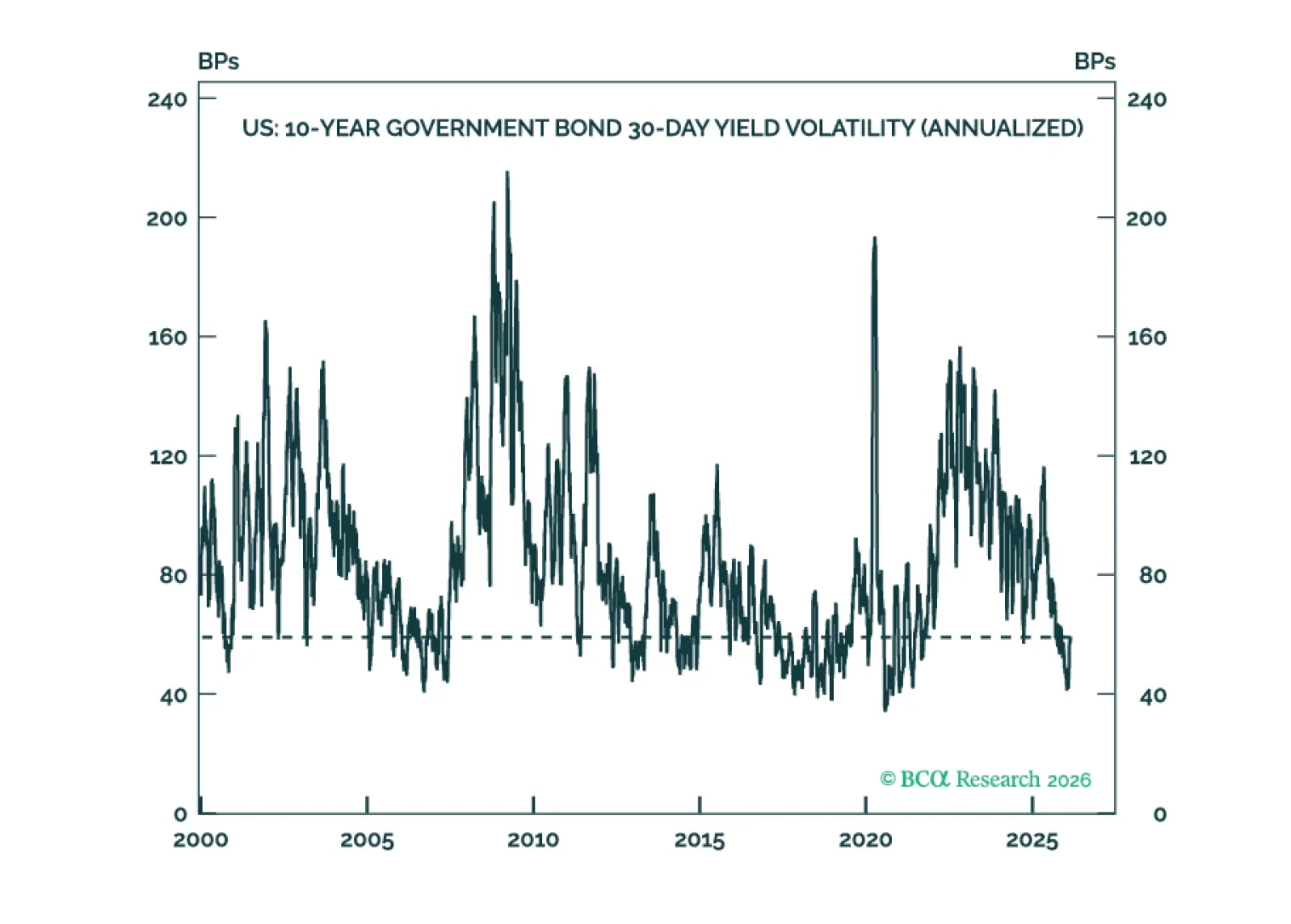

Interest rate volatility is very low across developed market fixed income. Investors should maximize the carry in their portfolios to outperform in a low rate vol environment.

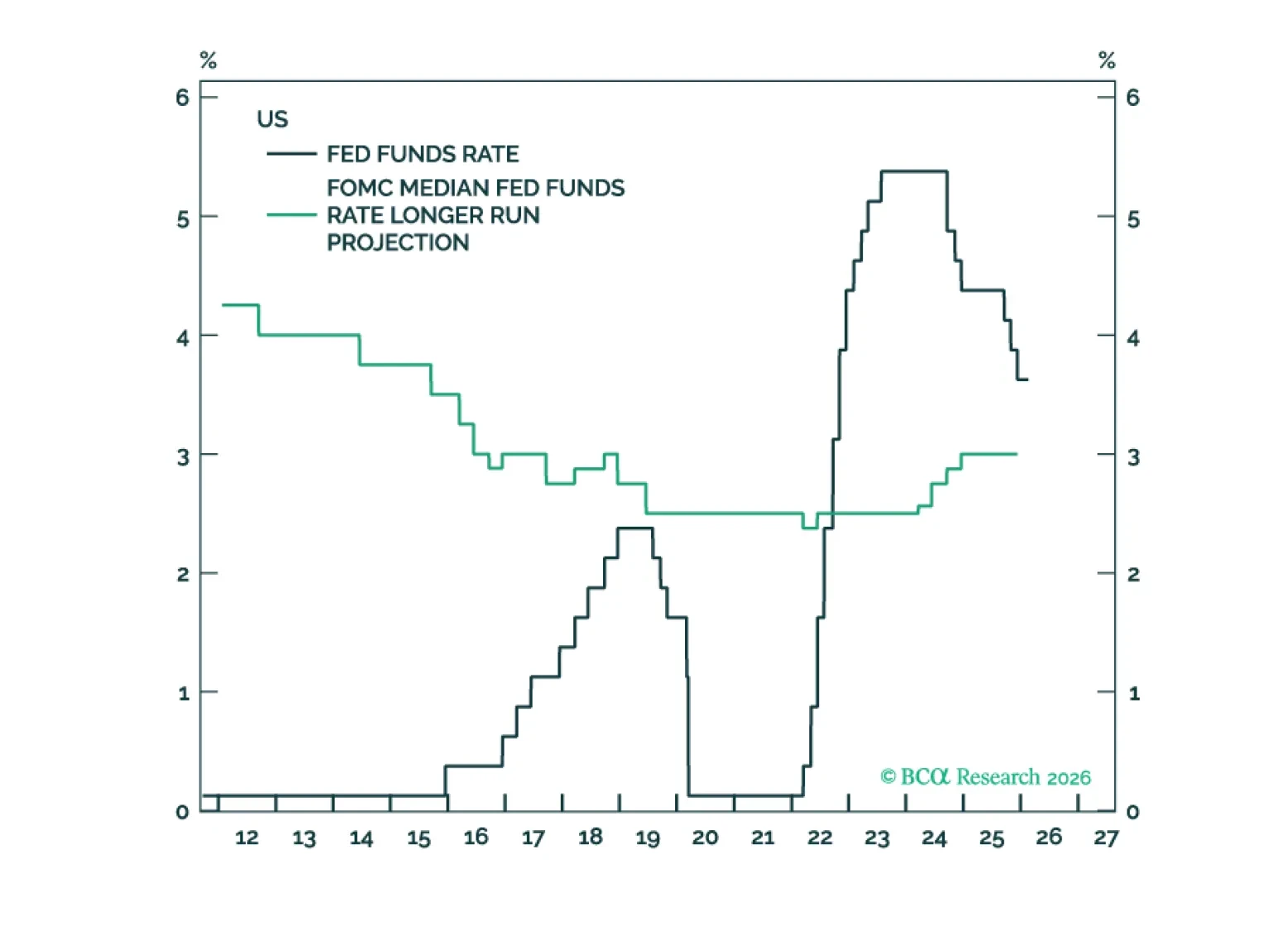

The neutral rate in the US is being propped up by a variety of forces that are at risk of reversing. These include the AI capex boom, large budget deficits, and the extraordinarily high level of household wealth. As such, interest rates are likely to surprise to the downside over the next few years.

Core inflation will get close to the Fed’s 2% target by the end of this year.

The labor market tightened in January, significantly lowering the odds of a H1 2026 rate cut. Rate cuts driven by lower inflation are still likely in H2 2026.

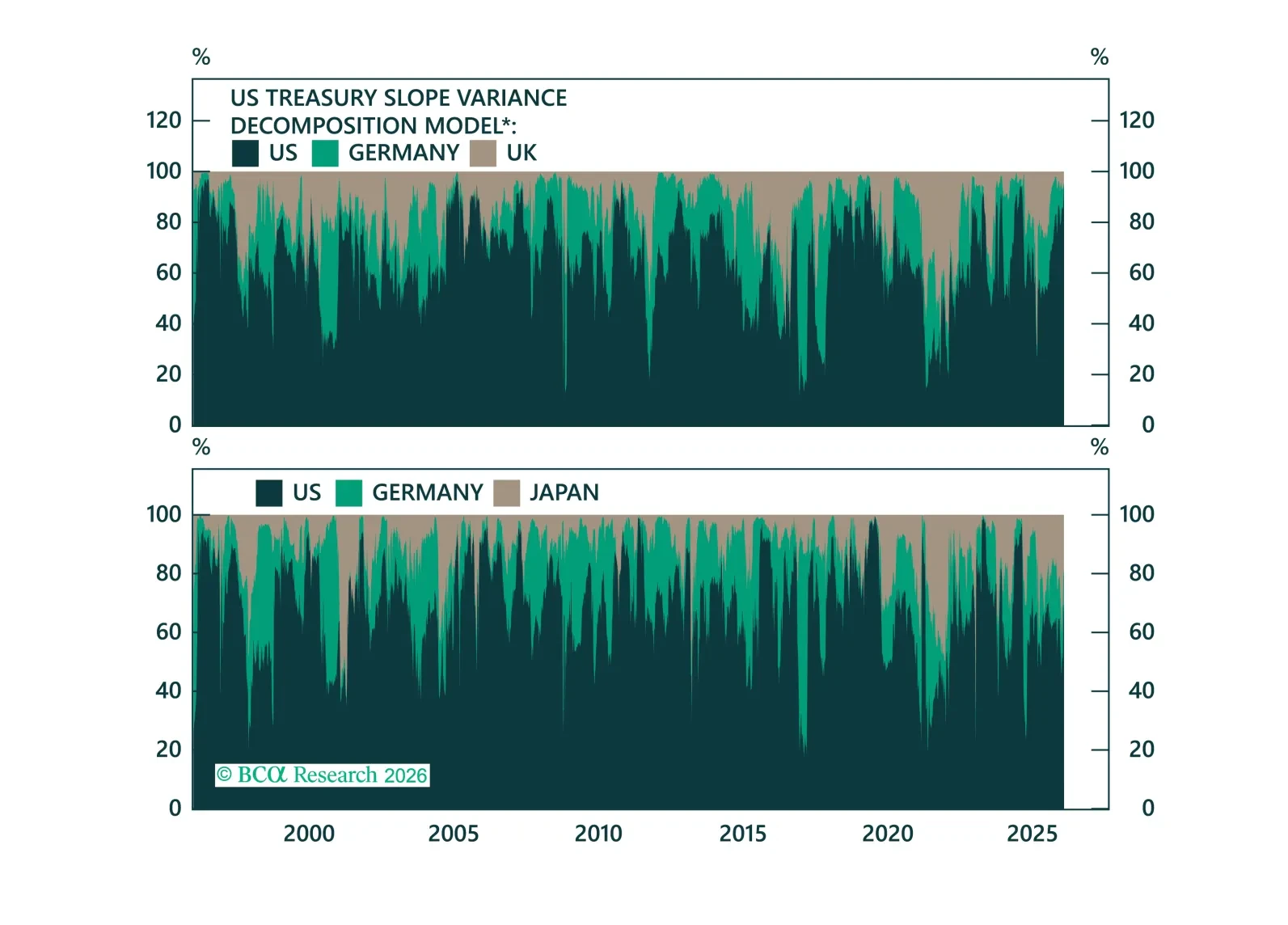

What’s driving government bond yields, and how do different bond markets impact each other? In today's Strategy Insight, we decompose yield moves into global drivers and idiosyncratic local drivers.