Fixed Income

Downgrade global and US portfolio duration from “above benchmark” to “at benchmark” as the risk of hawkish monetary policy surprises is rising.

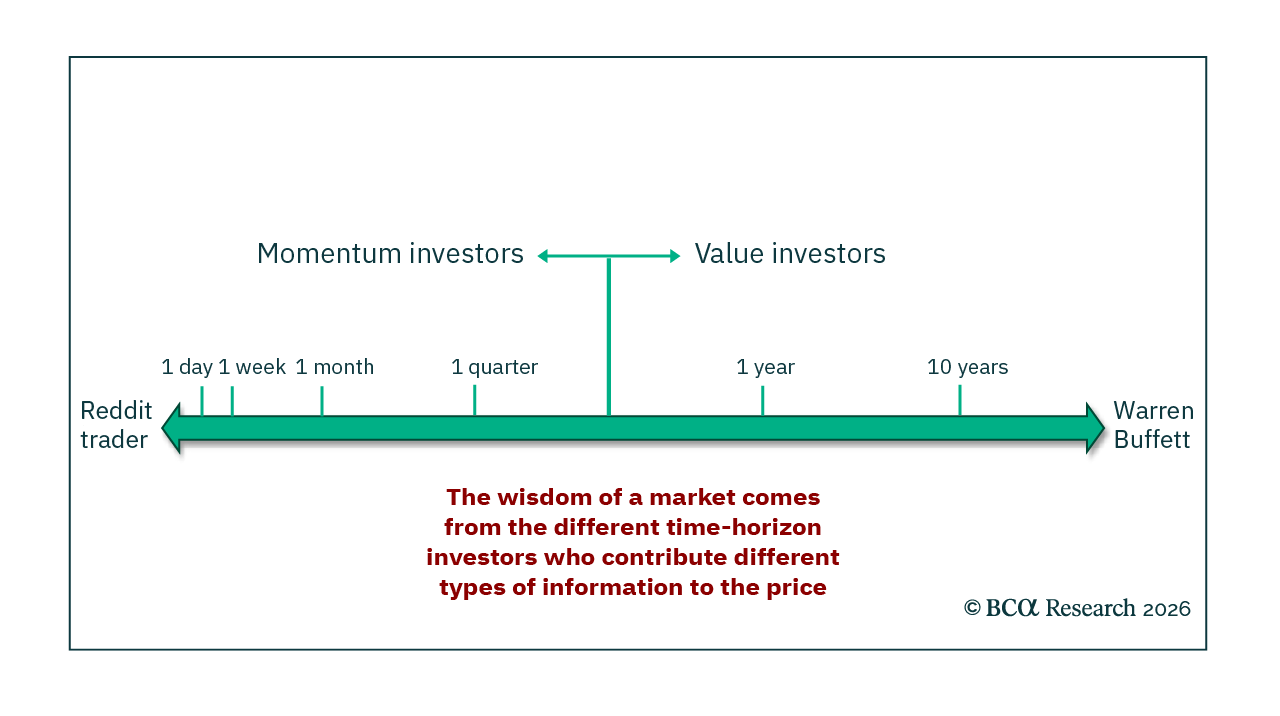

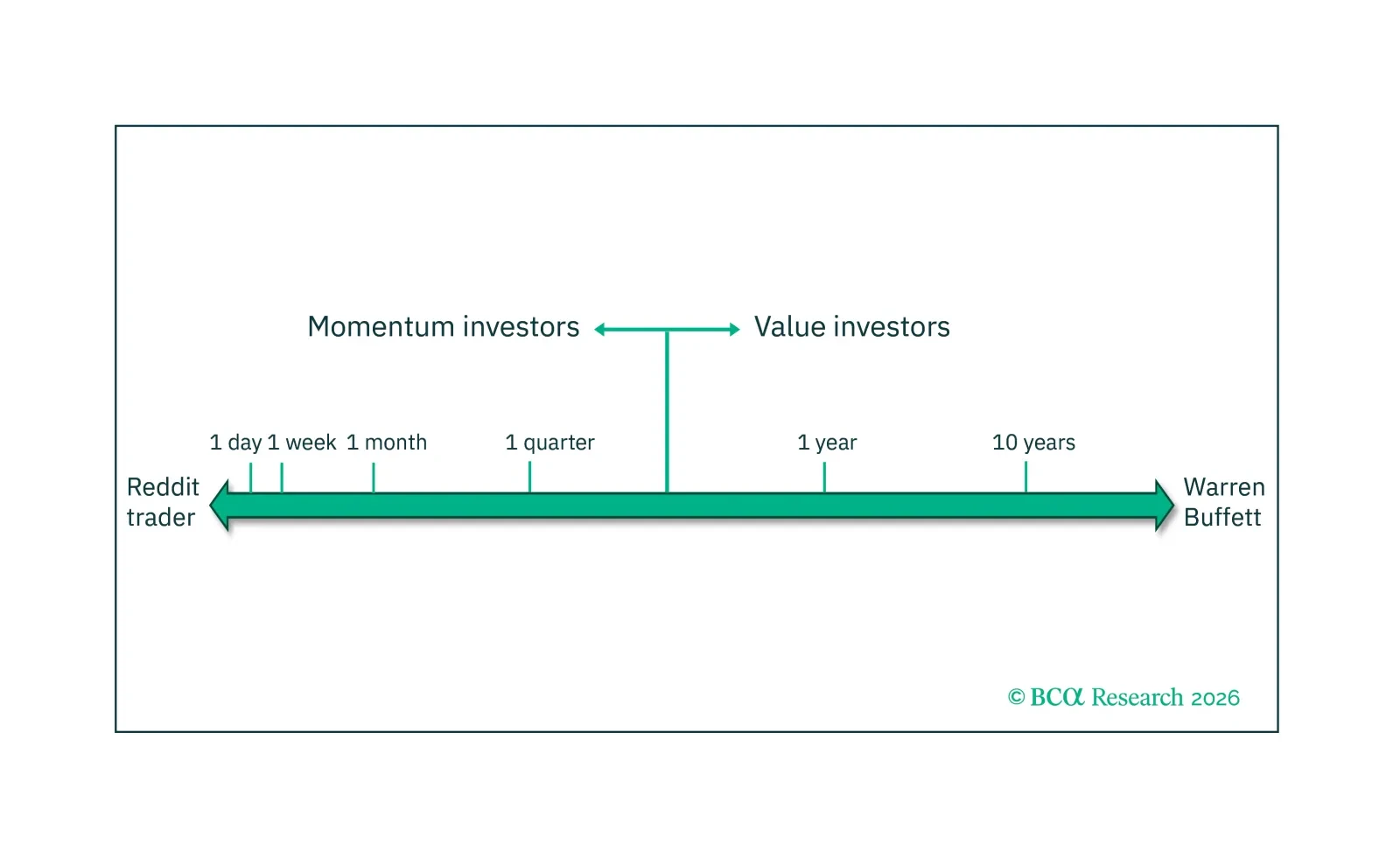

A market becomes inefficient, illiquid, and vulnerable to a phase transition when the ‘wisdom of crowds’ switches to the ‘madness of crowds.’ This switch from market wisdom to market madness may be the most significant recurring behavioural opportunity in active fund management and can be exploited in real-time by measuring the market’s complexity.

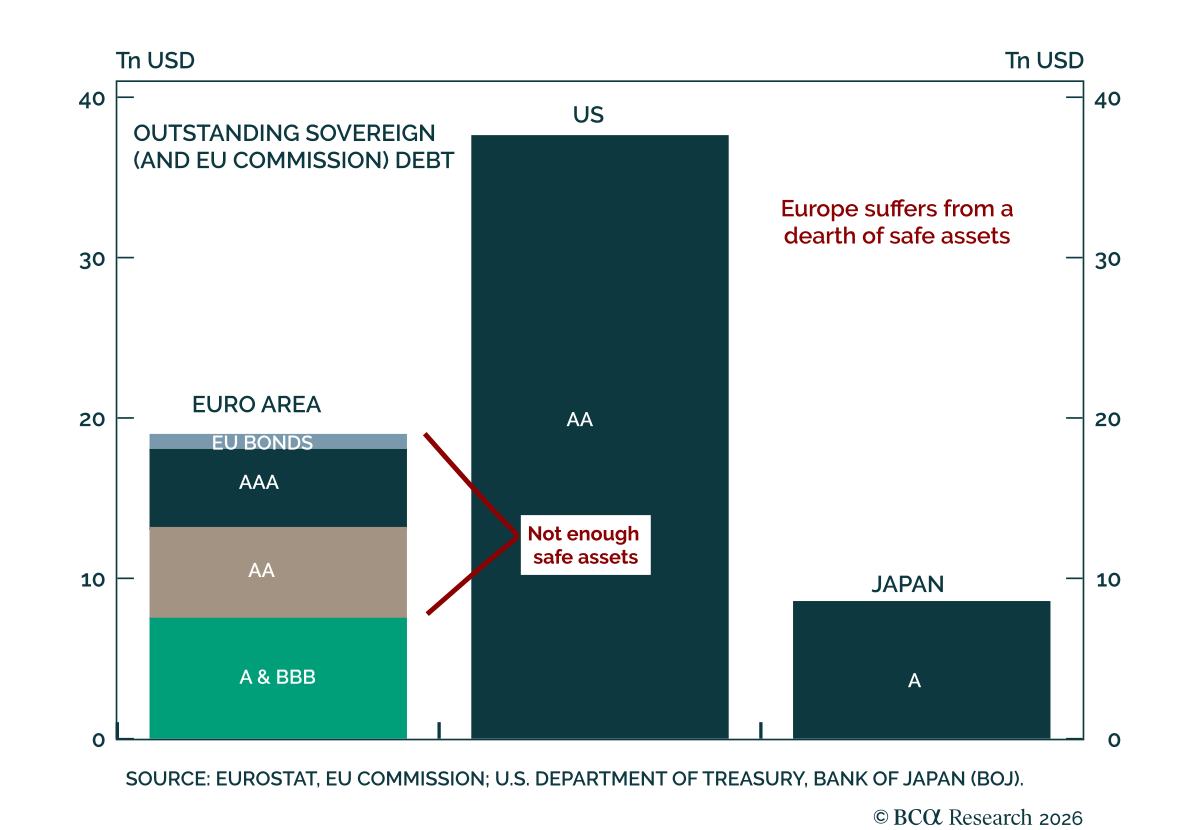

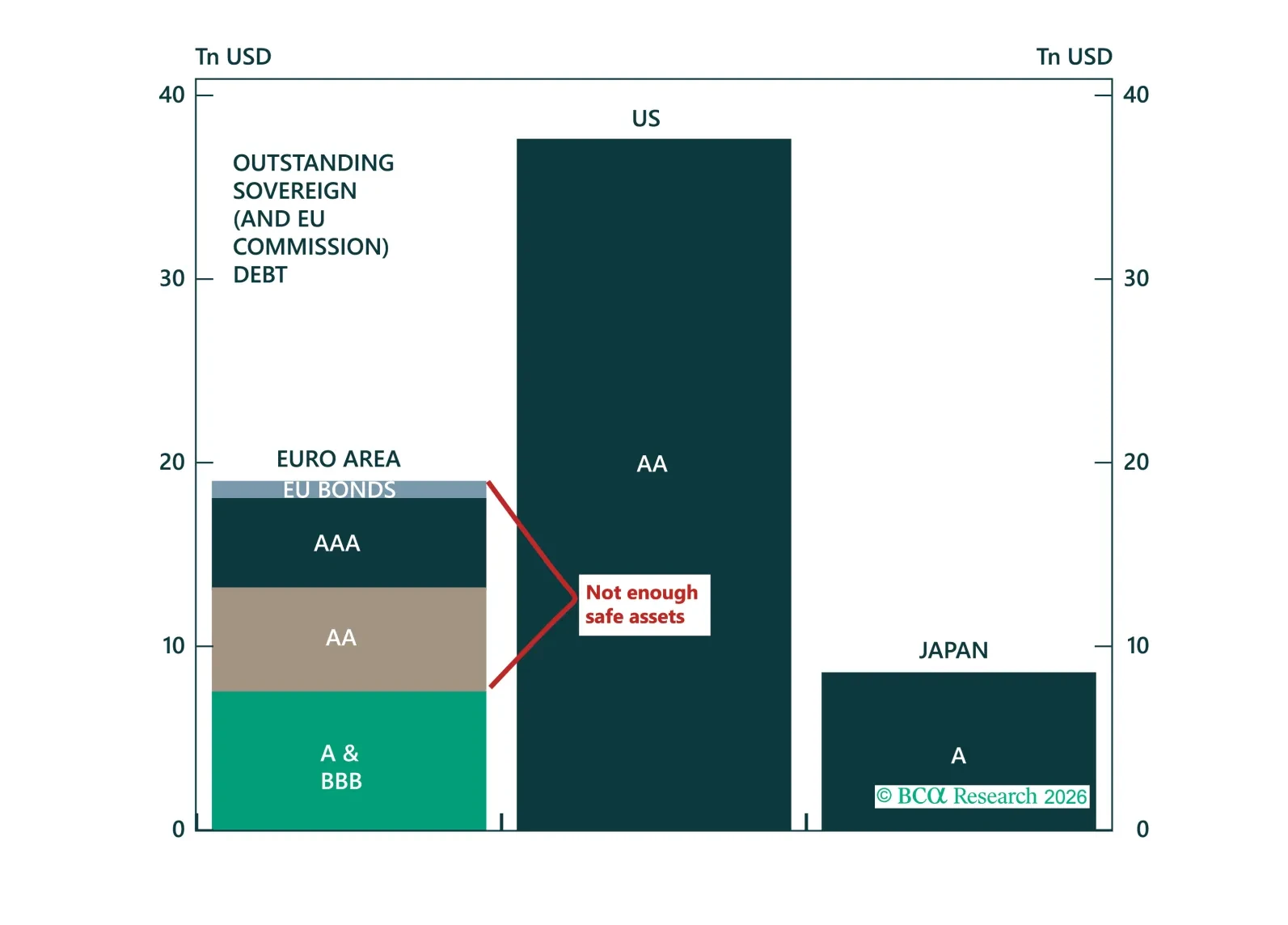

The dollar's retreat is creating the most compelling window for euro internationalisation since Maastricht, but Europe is missing the one instrument that would make it real. In this report, we make the case for the Eurobond, assess which model is most likely to prevail, and explain why the trade is long euro on dips and overweight Central and Eastern European sovereign spreads.

The April CPI report showed clear evidence of the direct effect of higher oil prices on inflation but, so far, limited evidence of passthrough to core.