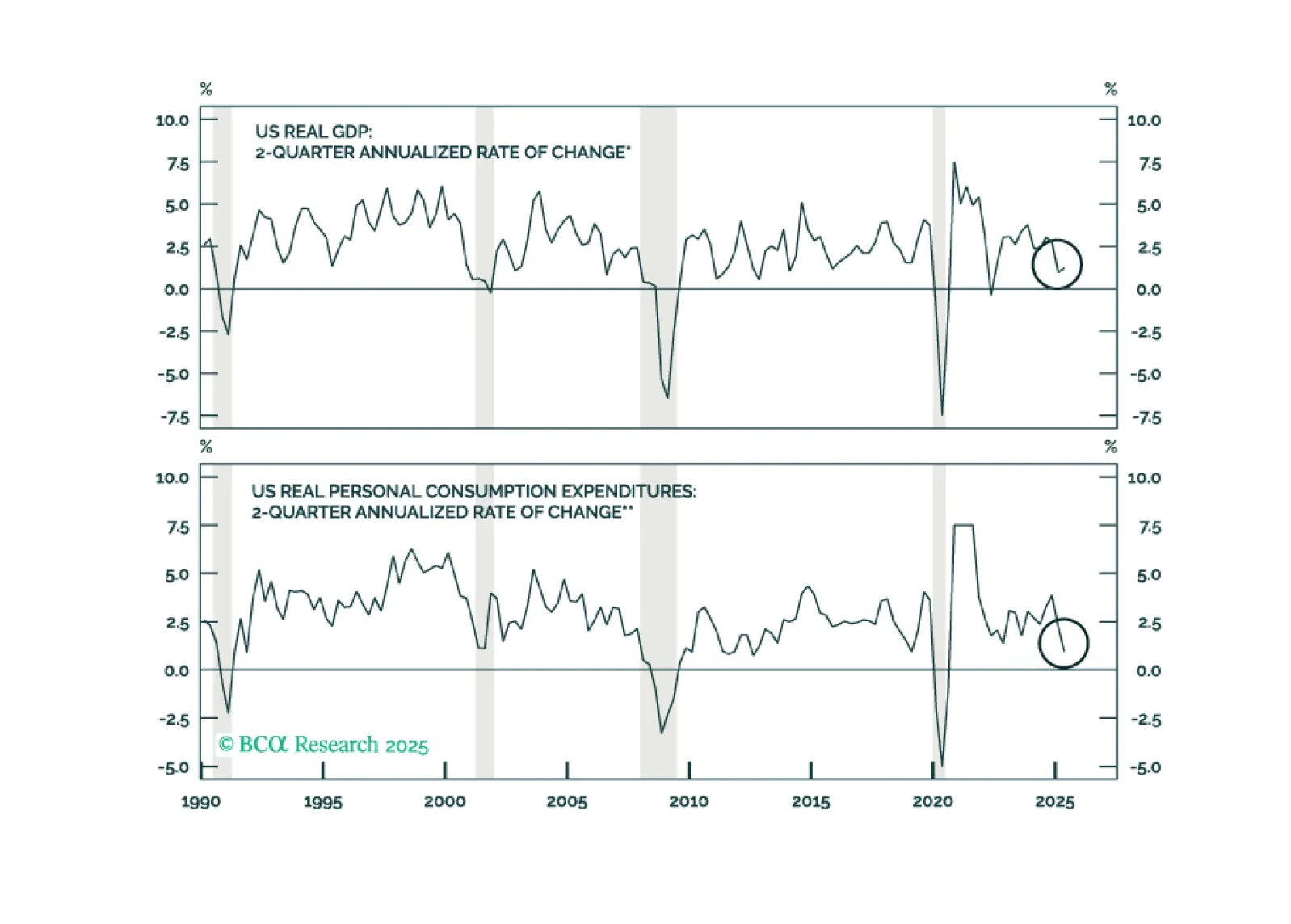

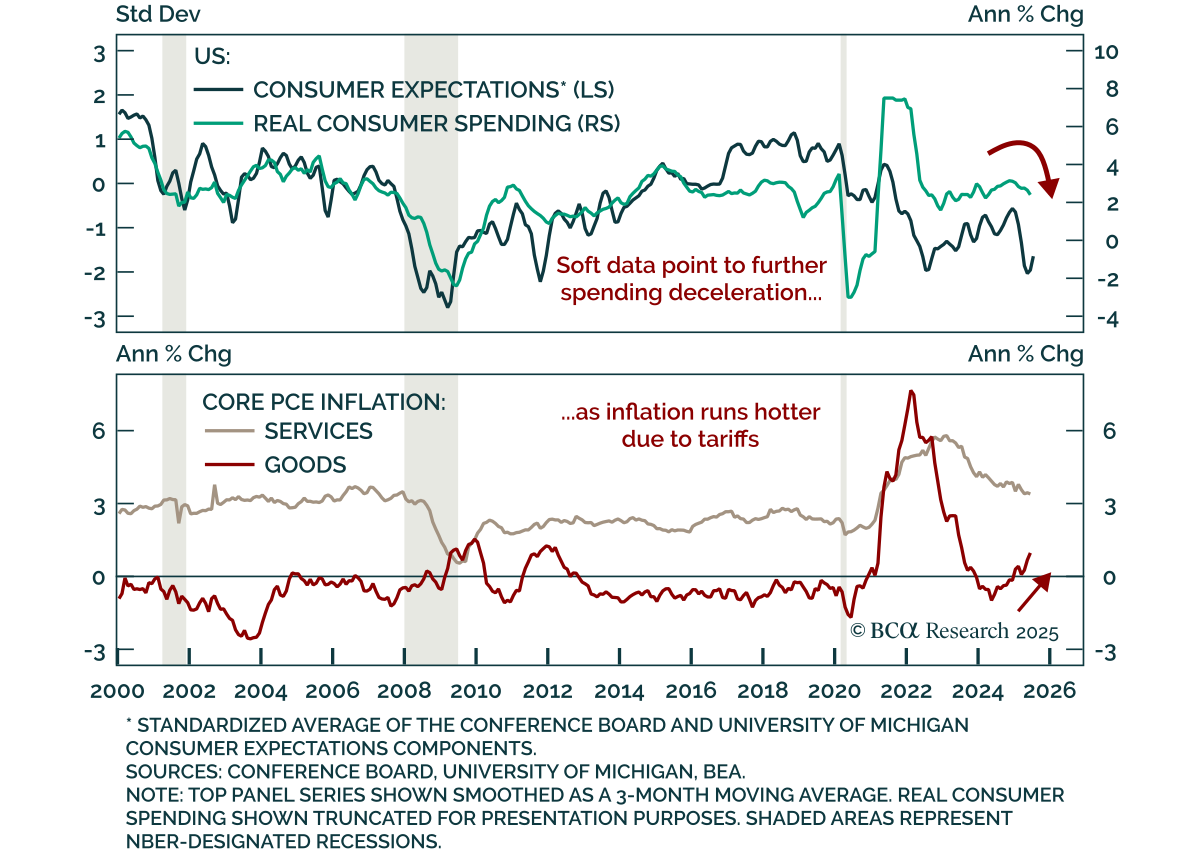

Consumer

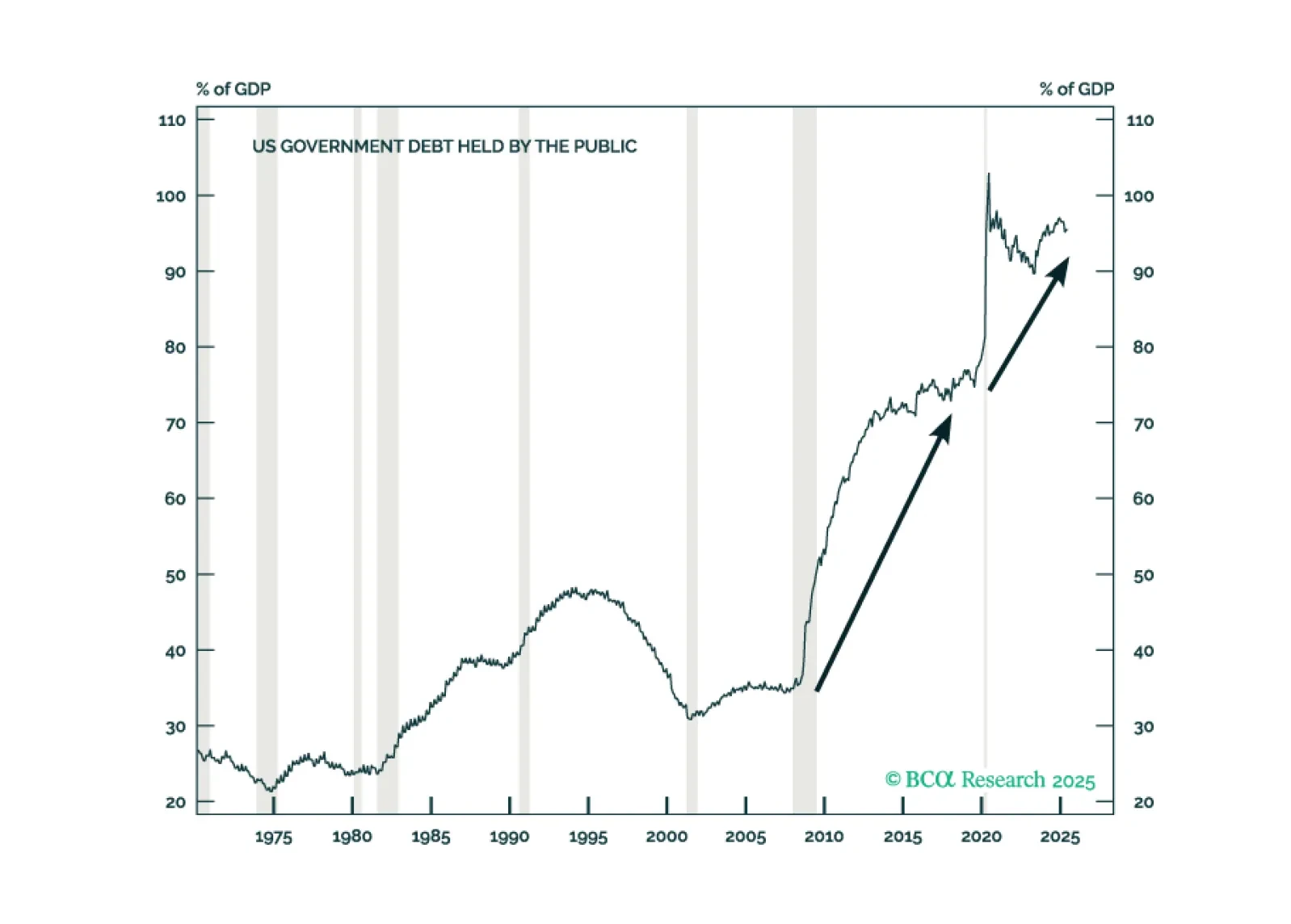

In Section II, Jonathan reviews the US fiscal outlook in the wake of the passage of the OBBBA.

In Section I, Doug weighs the recent reduction in trade uncertainty against the clear signs of labor market and consumer weakness. In Section II, Jonathan reviews the US fiscal outlook in the wake of the passage of the OBBBA.

We will only move to a fully defensive stance if the “whites of the recession’s eyes” appear. So far, they have not. We will be increasingly looking to our MacroQuant model for guidance on when the next turning point in markets may come.

Although we think the economy is weaker than investors realize, it has remained resilient and we will not fight the tape forever. If clear signs of a recession do not emerge over the next six weeks, we will drop our defensive recommendations.

Jay Powell won’t be removed as Fed Chair before the expiry of his term next May, but we will learn the identity of his replacement this year, setting up a potentially awkward “shadow Fed Chair” situation.

We will abandon our recession call if US economic data show clear signs of stabilization over the summer months. For now, that has not happened. Maintain a modest underweight to stocks but look to get more defensive if MacroQuant’s equity z-score falls below -1.