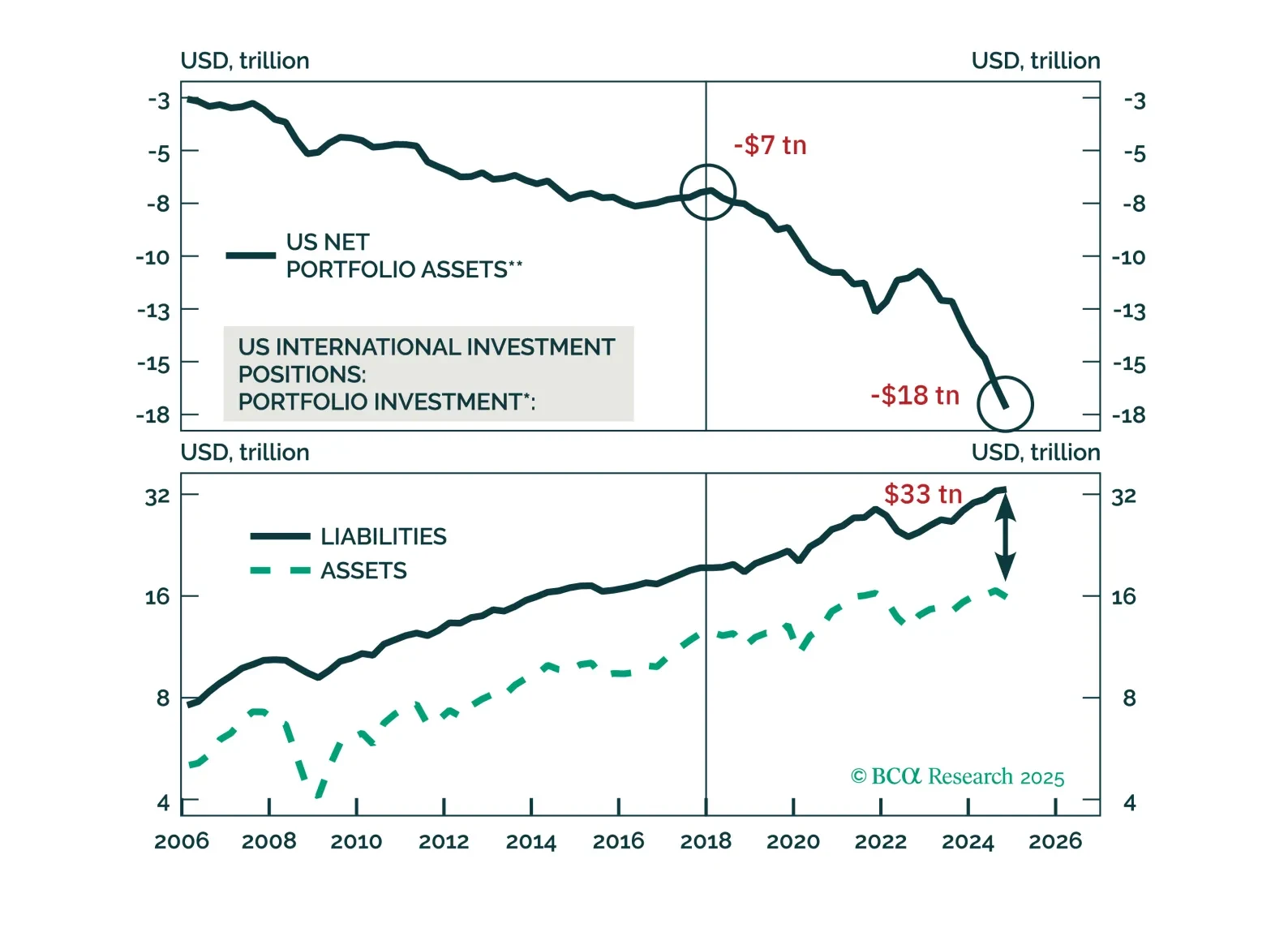

US Dollar

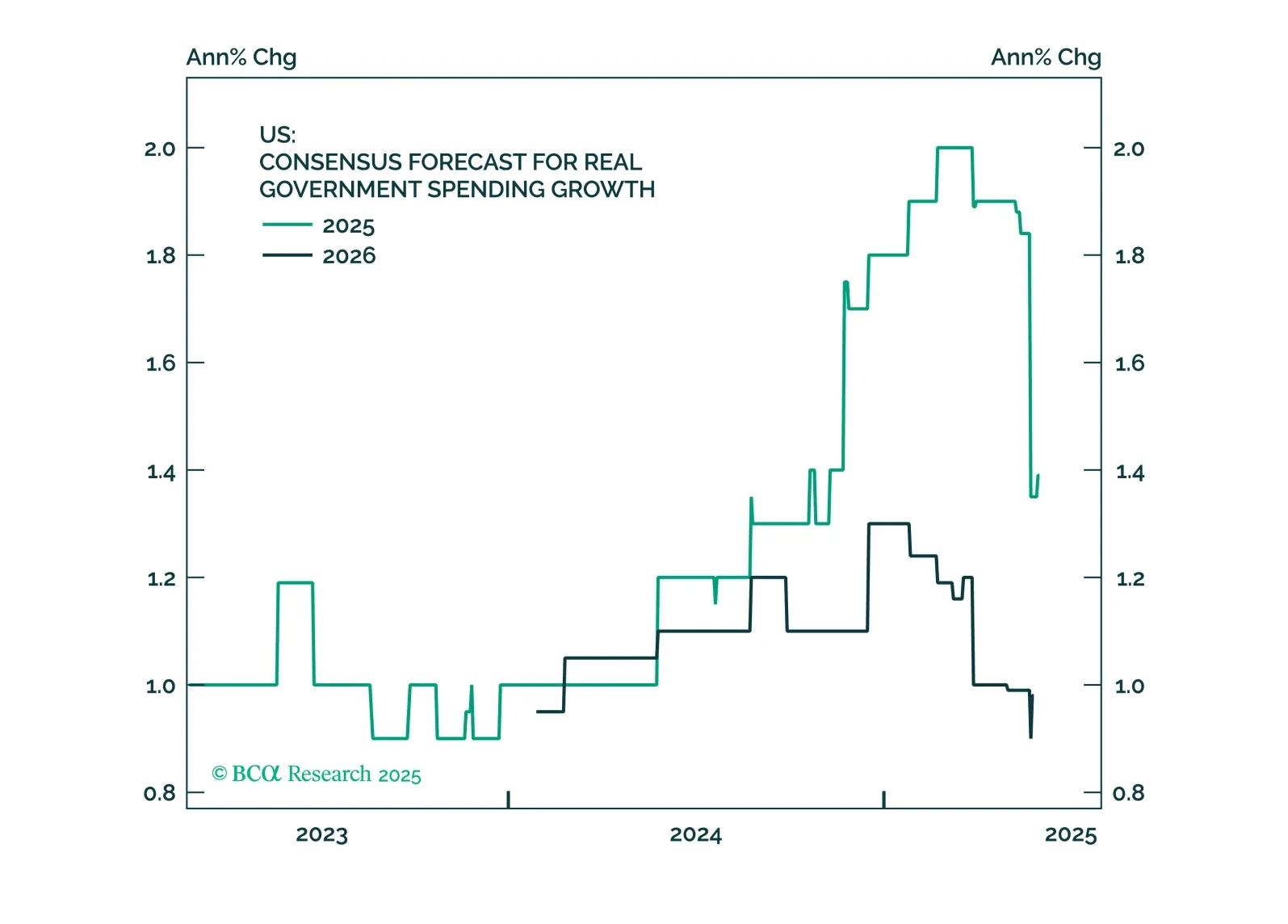

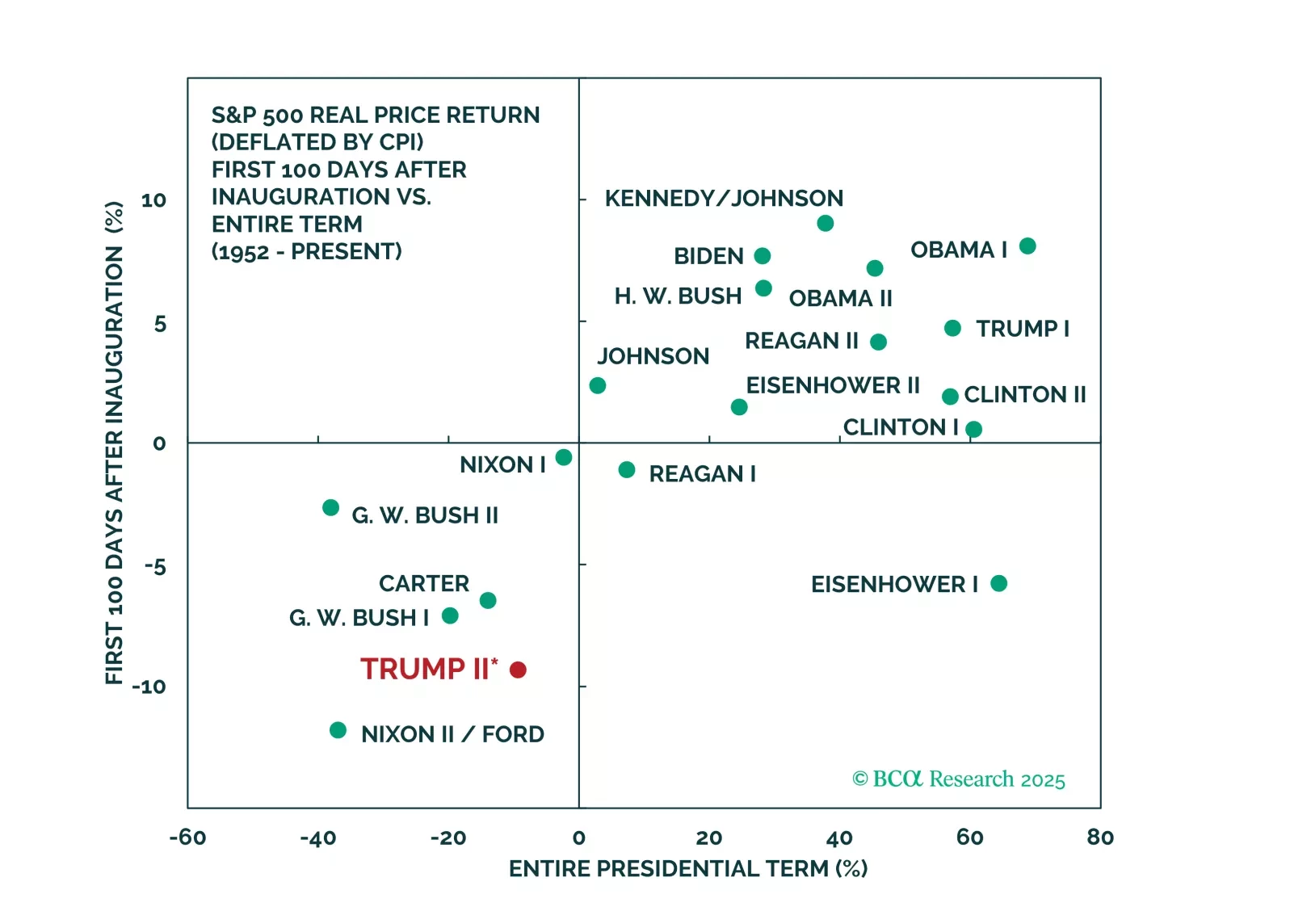

This month, we focus on the One Big Beautiful Bill Act (OBBBA). Our assessment in the Alpha report is that there won’t be any remaining alpha to harvest by shorting duration. The team that coined the “Human Steepener” moniker for President Trump is, effectively, throwing in the towel on looking for more upside to yields. There are many reasons for that view, but the main one is that the OBBBA legislation is just not that profligate, especially not relative to the investors’ expectations in the early days of the Trump 2.0 term.

Global currency markets have entered a new era. This implies that the framework for analyzing exchange rates must also change. We introduce a new framework for analyzing EM currencies and classify them into resilient and vulnerable categories. Finally, we are adding more EM domestic bonds to our portfolio and making many changes to our currency trades.

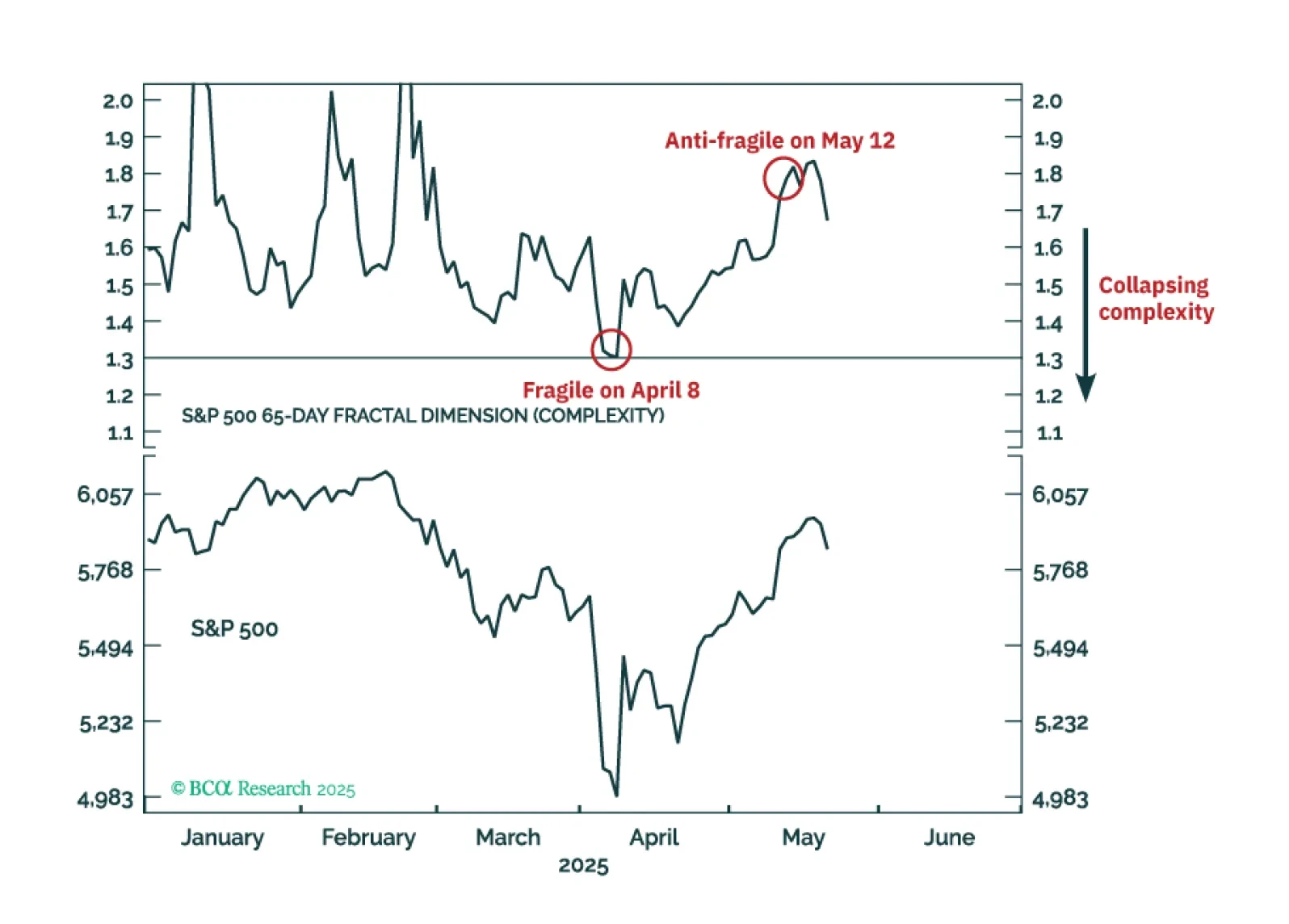

Right now, the major stock and bond markets are more ‘anti-fragile’ than fragile, and the Joshi rule recession indicators signal that a US recession is not imminent. This justifies a neutral, or default, tactical weighting to both stocks and bonds until a major market does become fragile, or until recession risk elevates. The one major price trend that is fragile is the 65-day selloff in the US dollar, which justifies a tactical overweighting to the dollar.

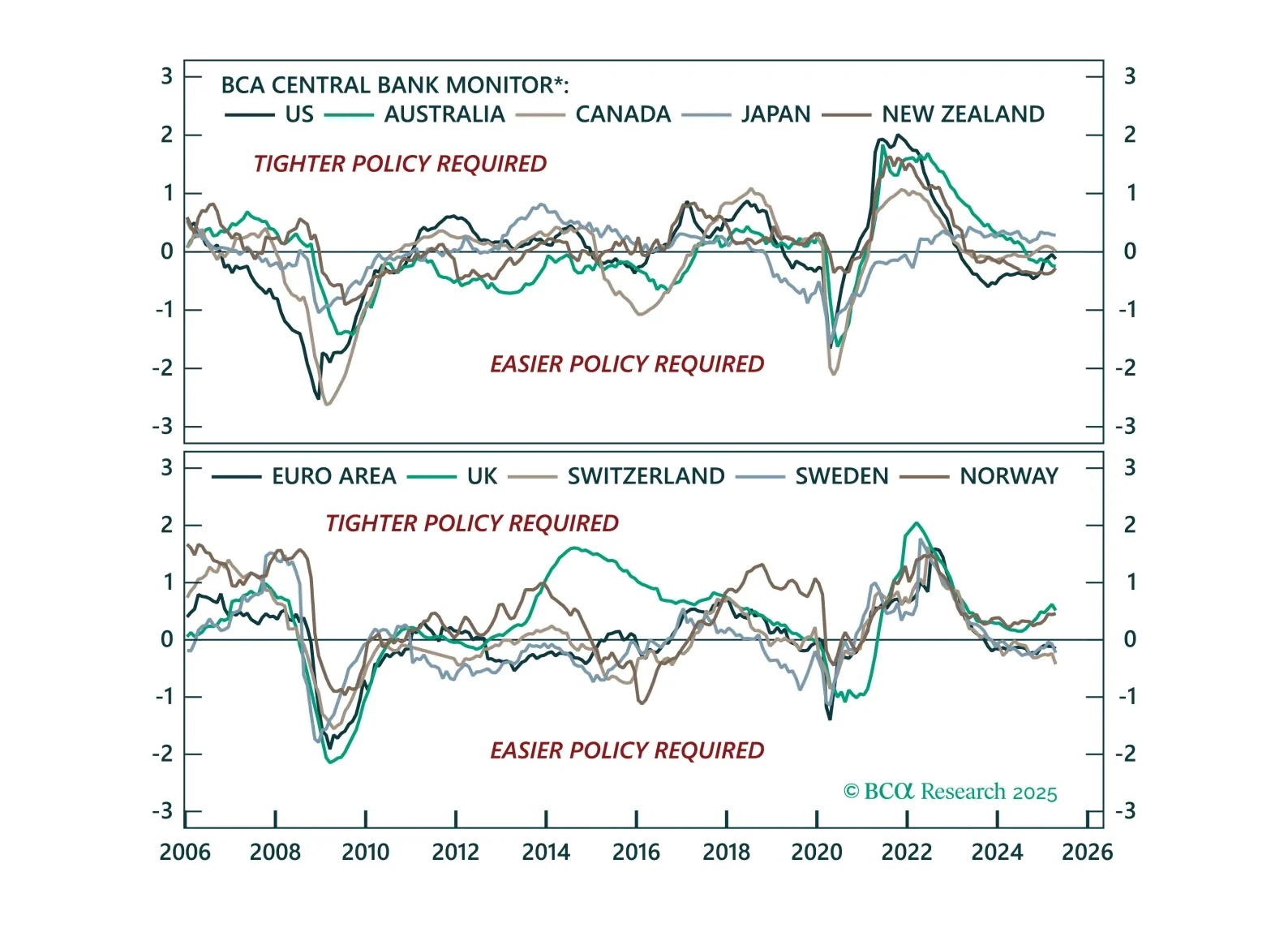

The easing bias remains, but not all central banks are equal. This Central Bank Monitor update reveals who is ready to cut more and who is still pretending not to.

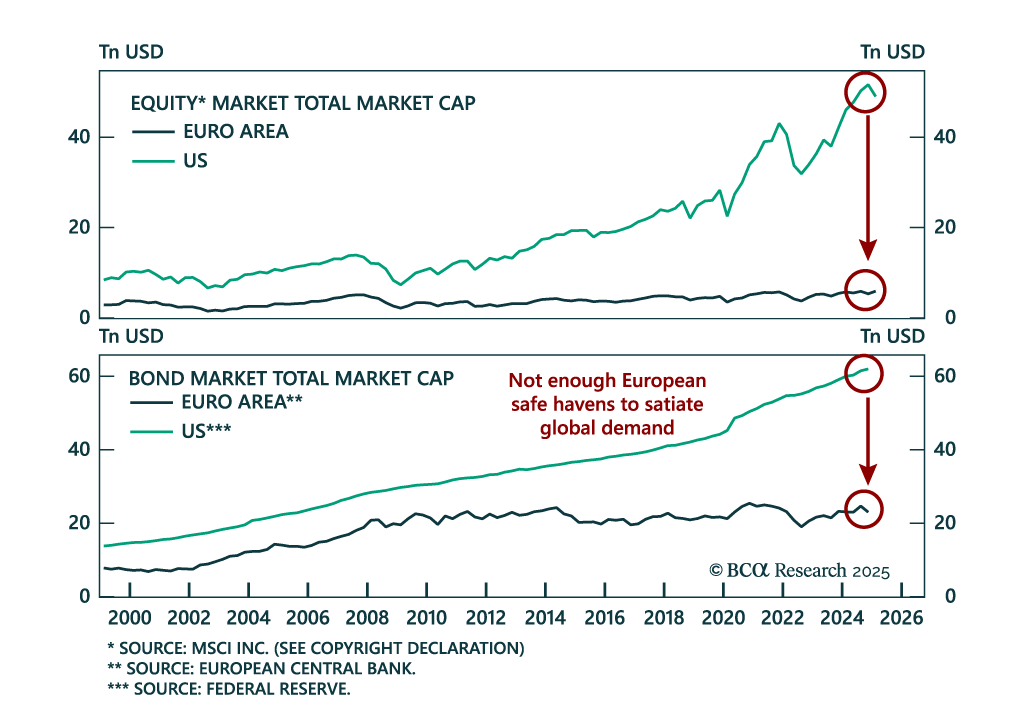

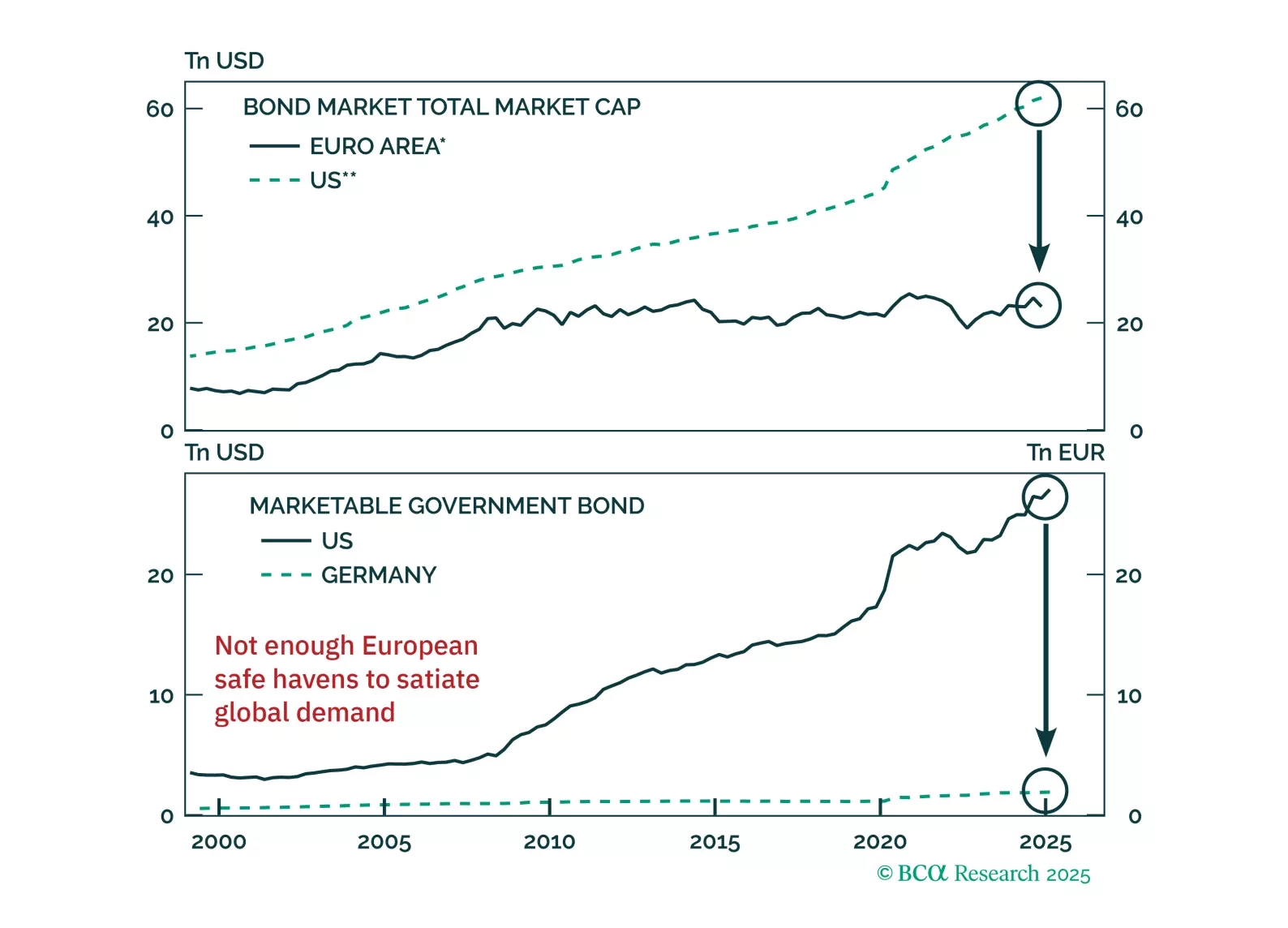

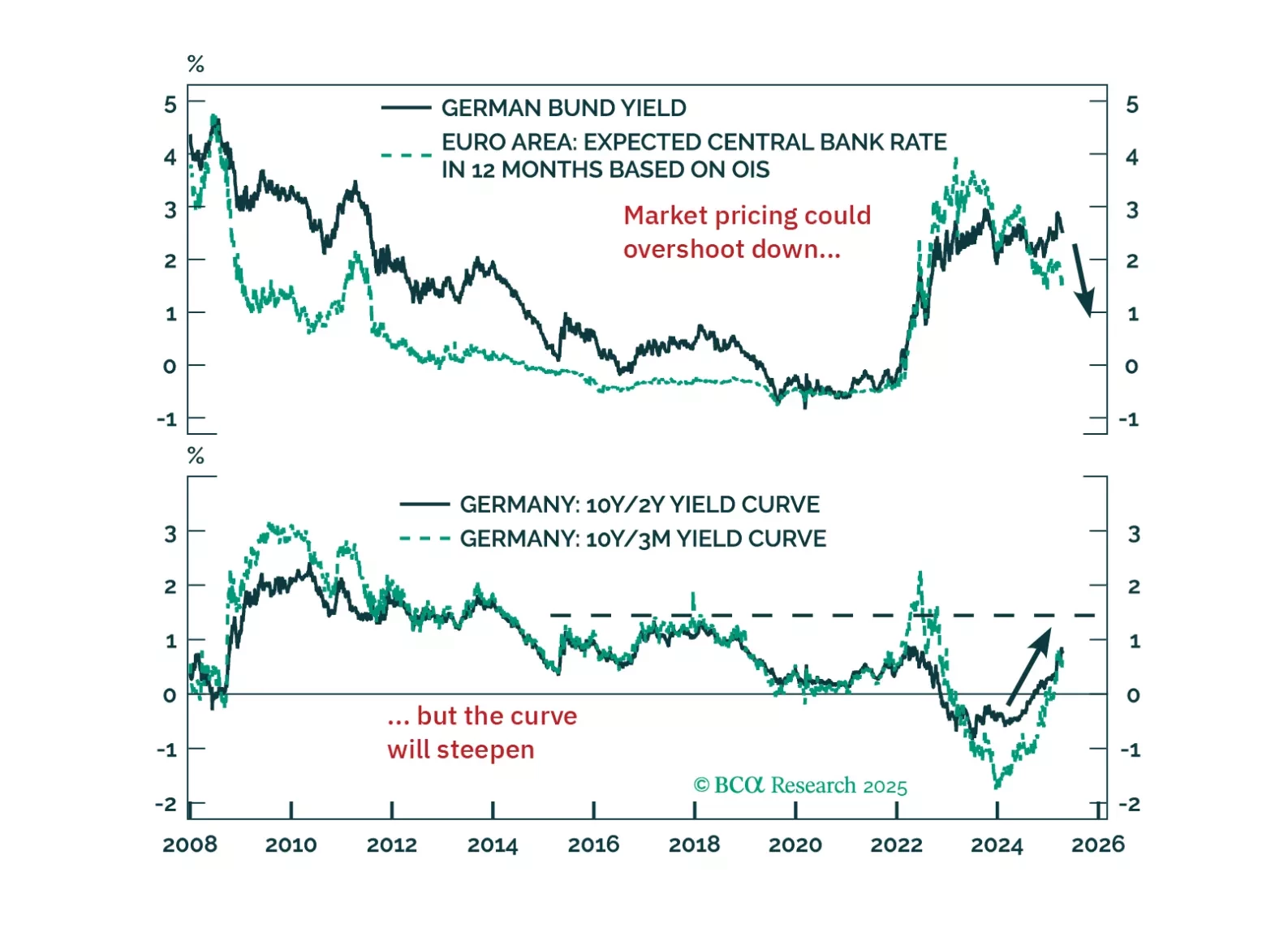

Are bunds the new Treasurys? The euro and German debt are gaining favor as safe havens, but markets may be overplaying the shift. Our latest report dissects what's durable, what's not, and how to trade the dislocation.

Do not play the bounce in US and global cyclical assets as Trump backpedals from the trade war. China will talk, but the pace will be slow and the outcome disappointing. Fiscal stimulus will surprise marginally in the EU, China, and even the US, but still may not rescue the business cycle.

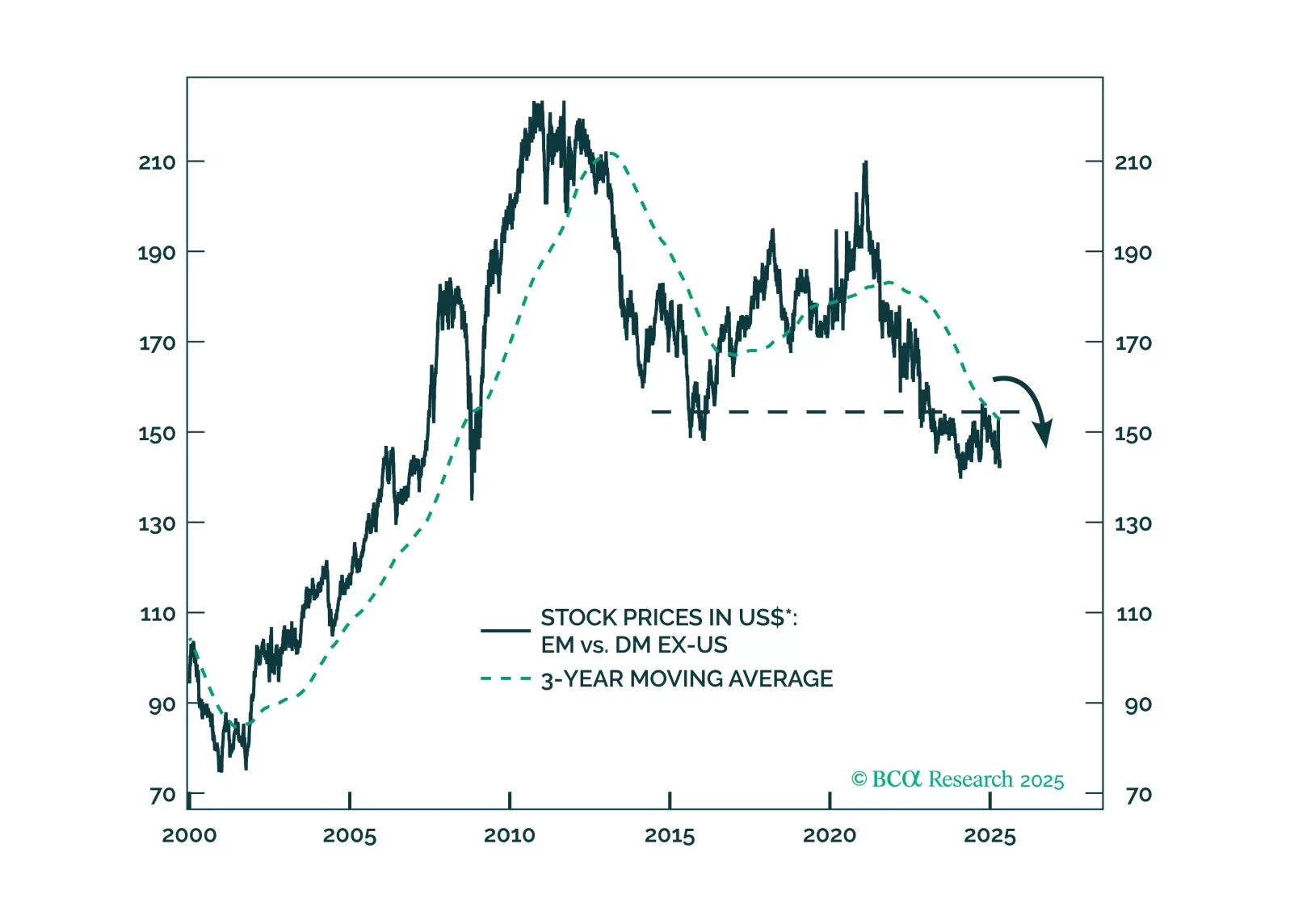

Although the sell-off in the US dollar and relative outperformance of non-US stocks will pause over the coming months as a global recession begins, the fading of US exceptionalism will still cause the dollar to weaken and US stocks to underperform over a multi-year horizon.

Bessenomics has failed so far. The key pillars of Bessent’s policy mix – achieving lower interest rates and robust economic growth – have been severely jeopardized. The US dollar has depreciated for different reasons than Bessent had envisioned and has pushed up long-term US bond yields. A trade deal between the US and China will likely come too late to preclude a major downshift in global growth.

Europe’s deflation problem is getting harder to ignore. This week’s ECB cut is just the beginning — tariffs, the euro’s rally, and softening demand all point to more easing ahead. We explain what it means for yields, equities, and EUR/USD.