Legislation

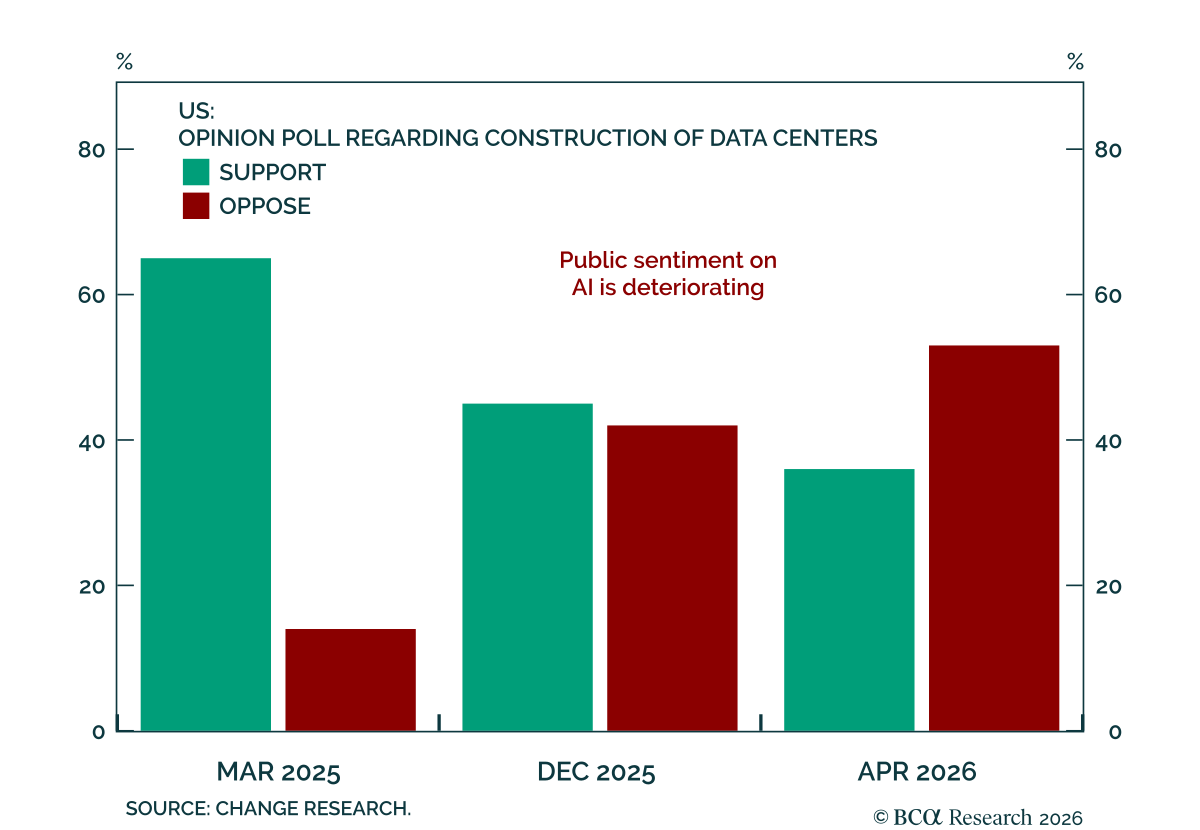

The populist backlash against AI could result in bipartisan regulation in 2027, but is especially likely to prompt tax hikes from 2029.

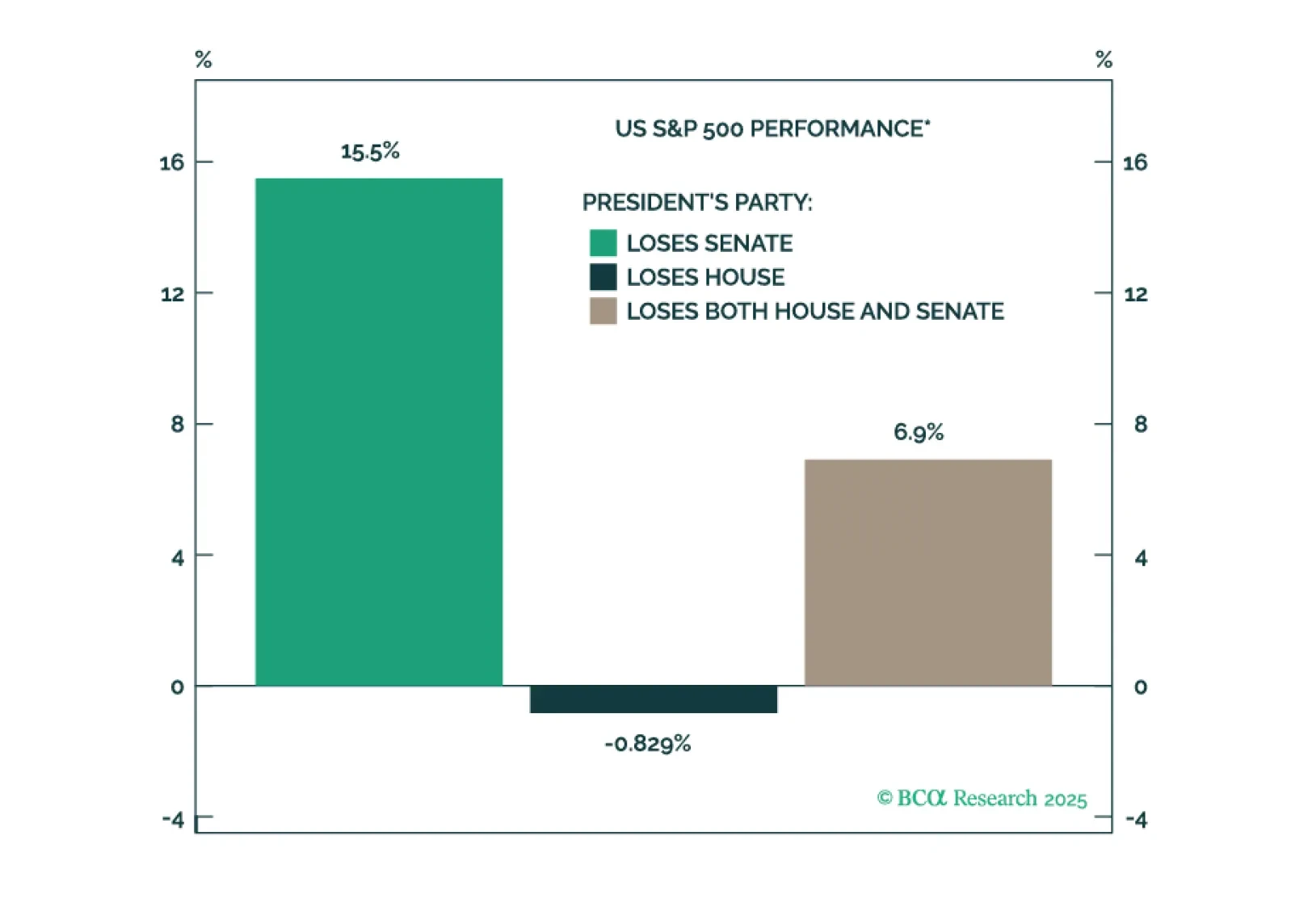

Partisan redrawing of congressional districts will not prevent Democrats from retaking the House in the 2026 midterms. Neither will the Supreme Court's look at the Voting Rights Act.

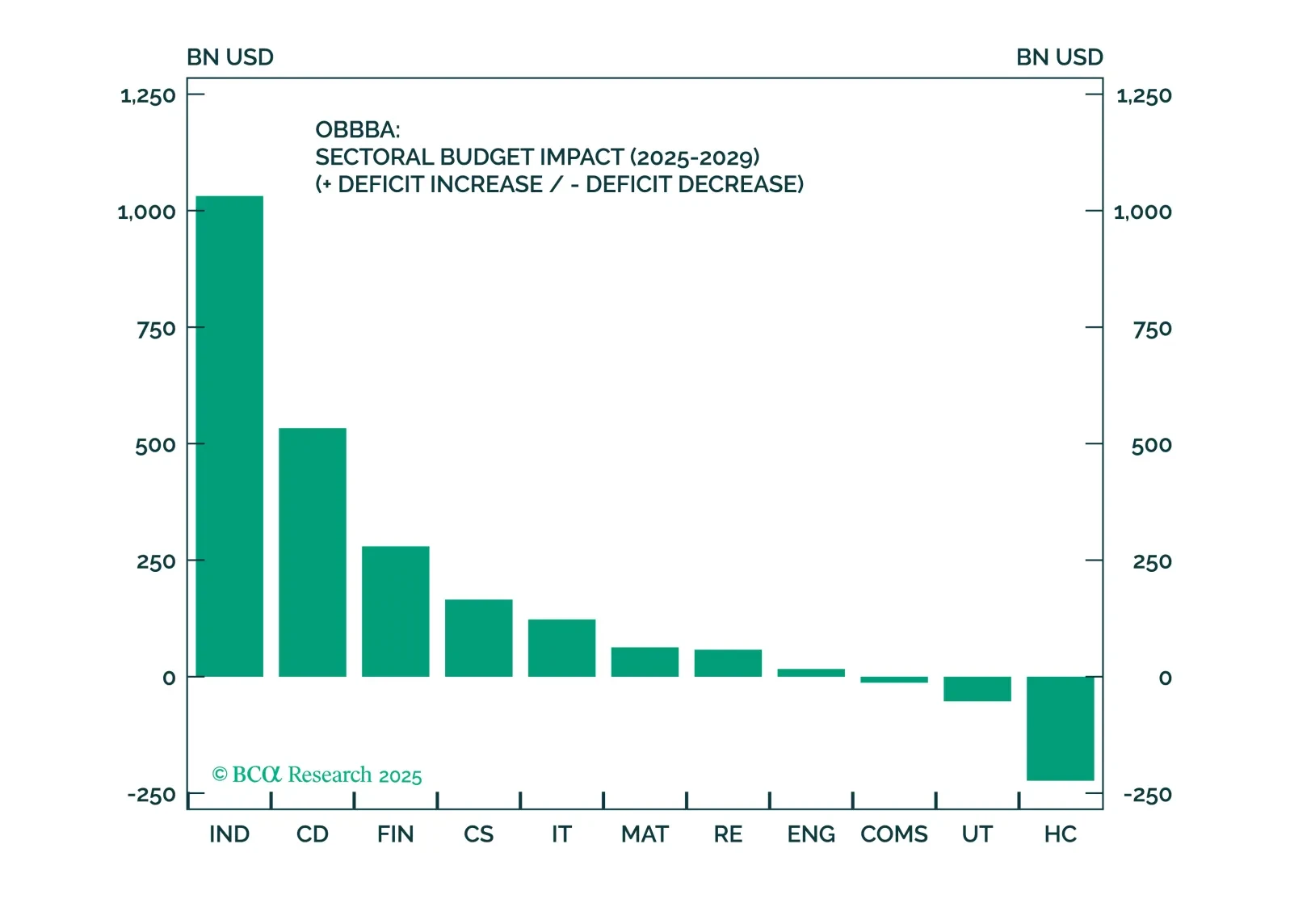

Despite macro headwinds, the OBBBA clearly favors Industrials, Financials, and Consumer Discretionary equity sectors. A carefully constructed, factor-aware basket in these sectors is well positioned to outperform in a fiscal-driven, uncertain environment.

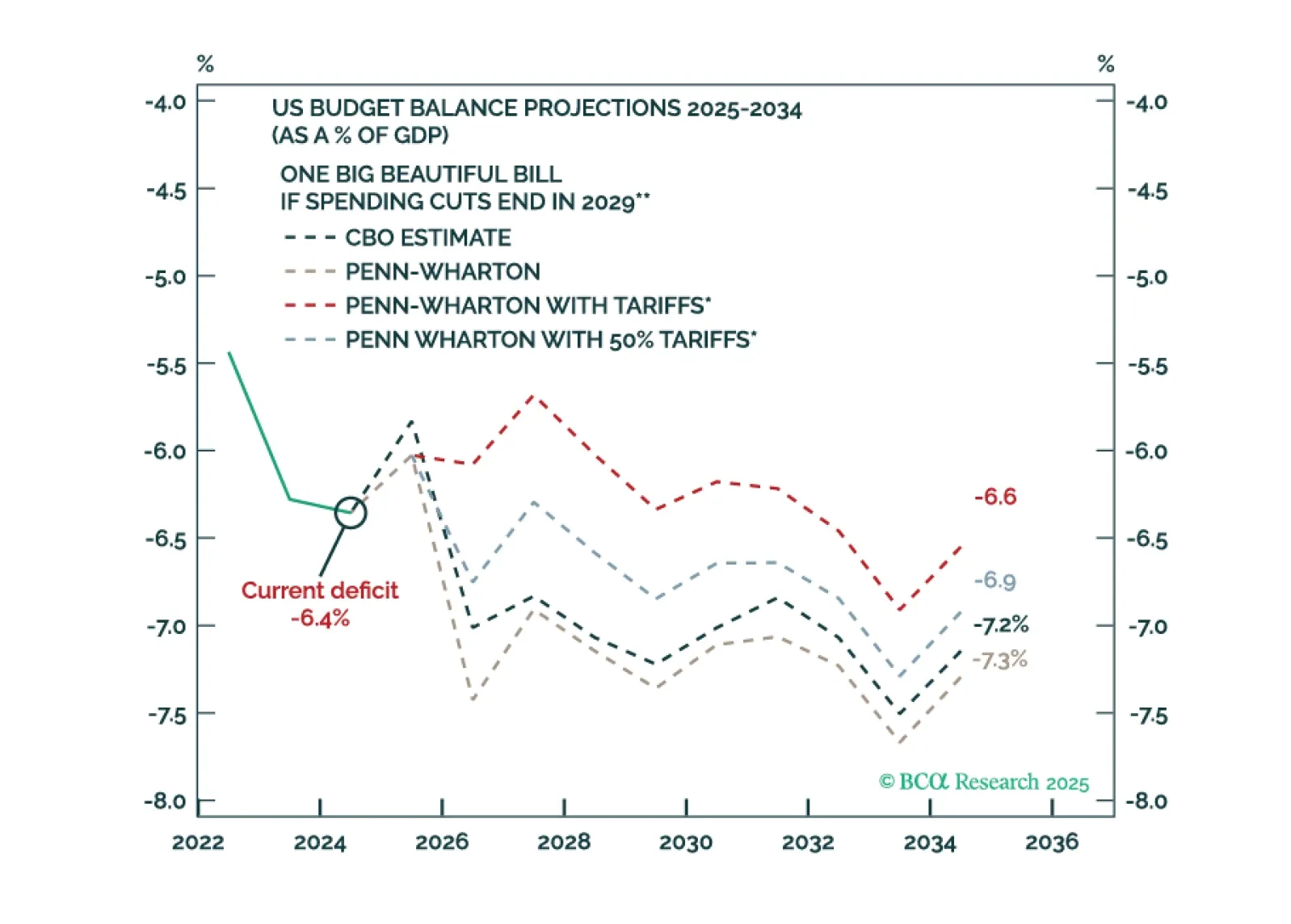

President Trump’s big beautiful bill will pass but faces near-term hurdles and will not tighten the government’s belt. It will combine with renewed tariff implementation to generate near-term risk for both the bond and stock market. The Iran crisis fizzled, saving Trump from a major oil shock that could have derailed his second term.

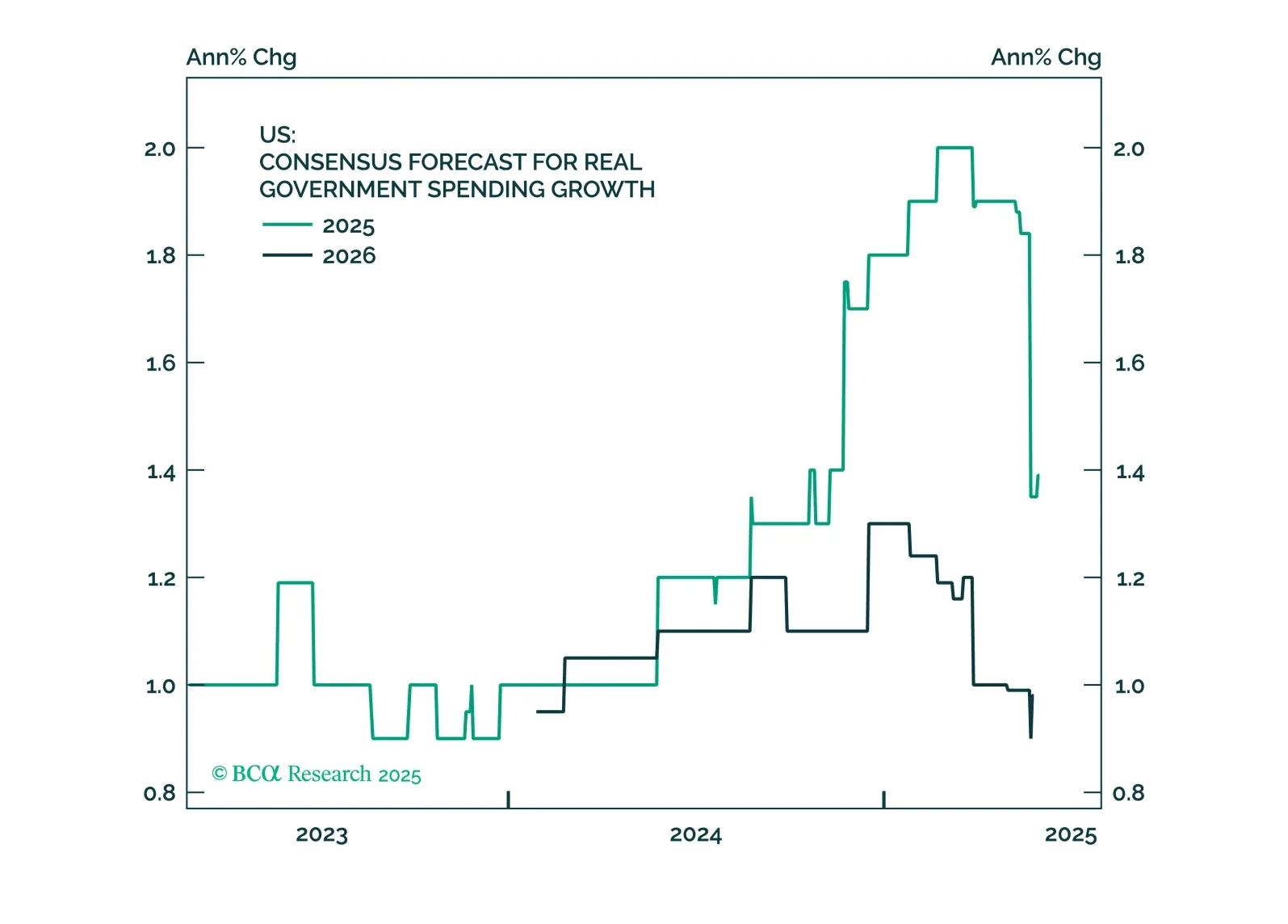

Bond market volatility will spike again in the near term. The Fed is committed to an easing cycle yet the Trump administration’s signature fiscal policy action will stimulate the economy. Tariffs are supposed to keep the budget deficit contained but they are inflationary.

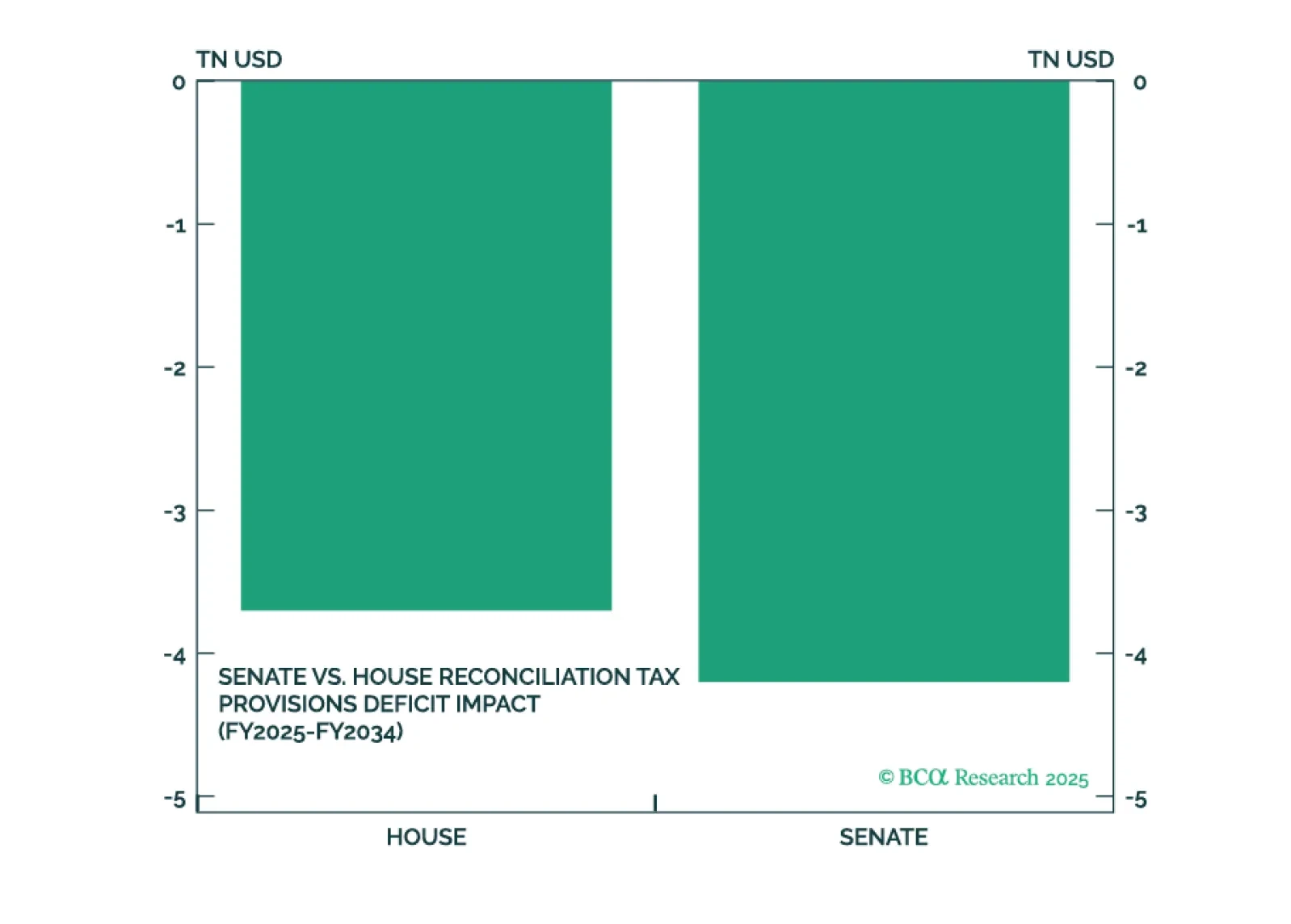

This month, we focus on the One Big Beautiful Bill Act (OBBBA). Our assessment in the Alpha report is that there won’t be any remaining alpha to harvest by shorting duration. The team that coined the “Human Steepener” moniker for President Trump is, effectively, throwing in the towel on looking for more upside to yields. There are many reasons for that view, but the main one is that the OBBBA legislation is just not that profligate, especially not relative to the investors’ expectations in the early days of the Trump 2.0 term.

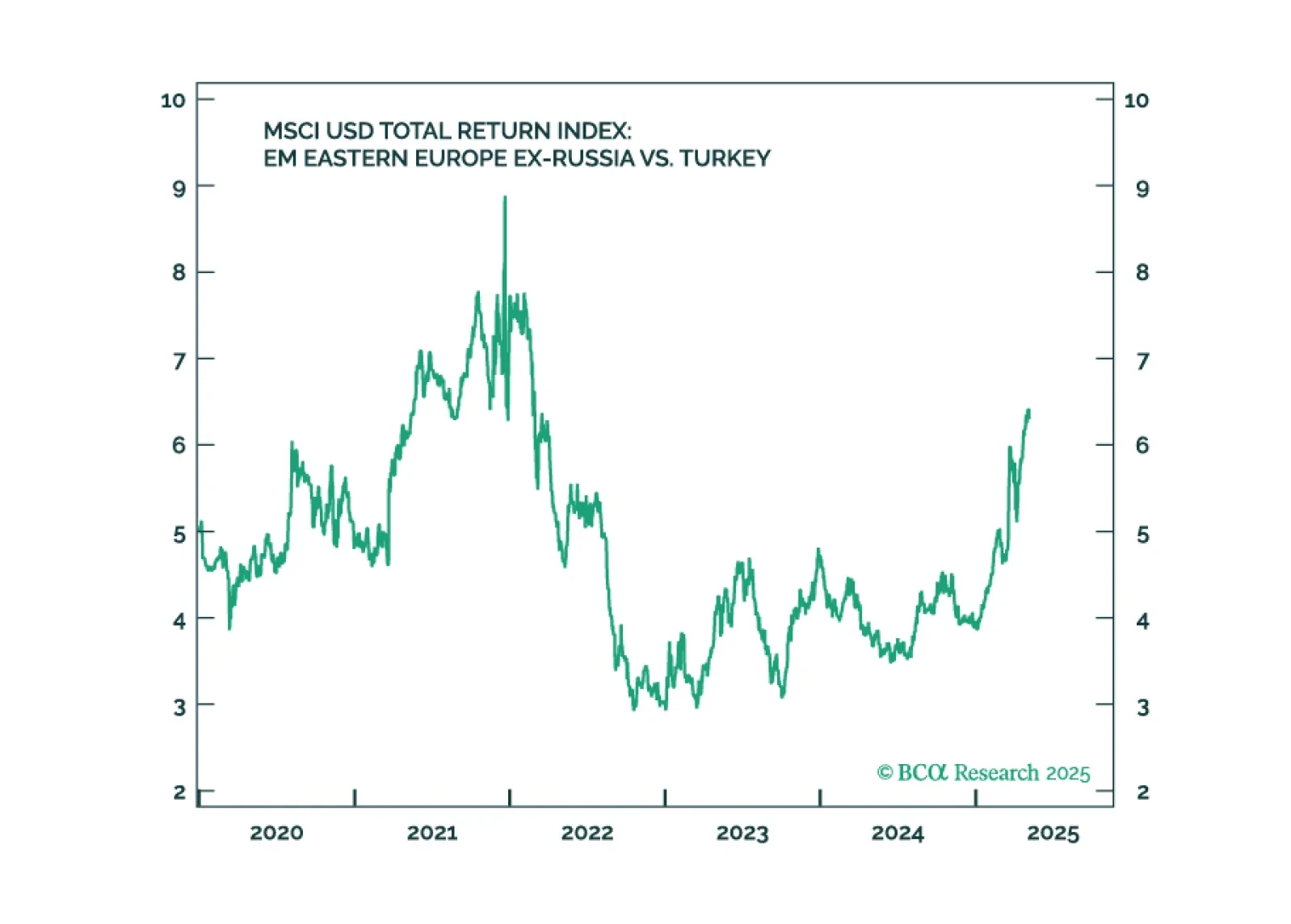

Erdogan's rule continues to decline. Social unrest will persist, governance will erode, and the macro backdrop will deteriorate further. We recommend underweighting Turkish assets.

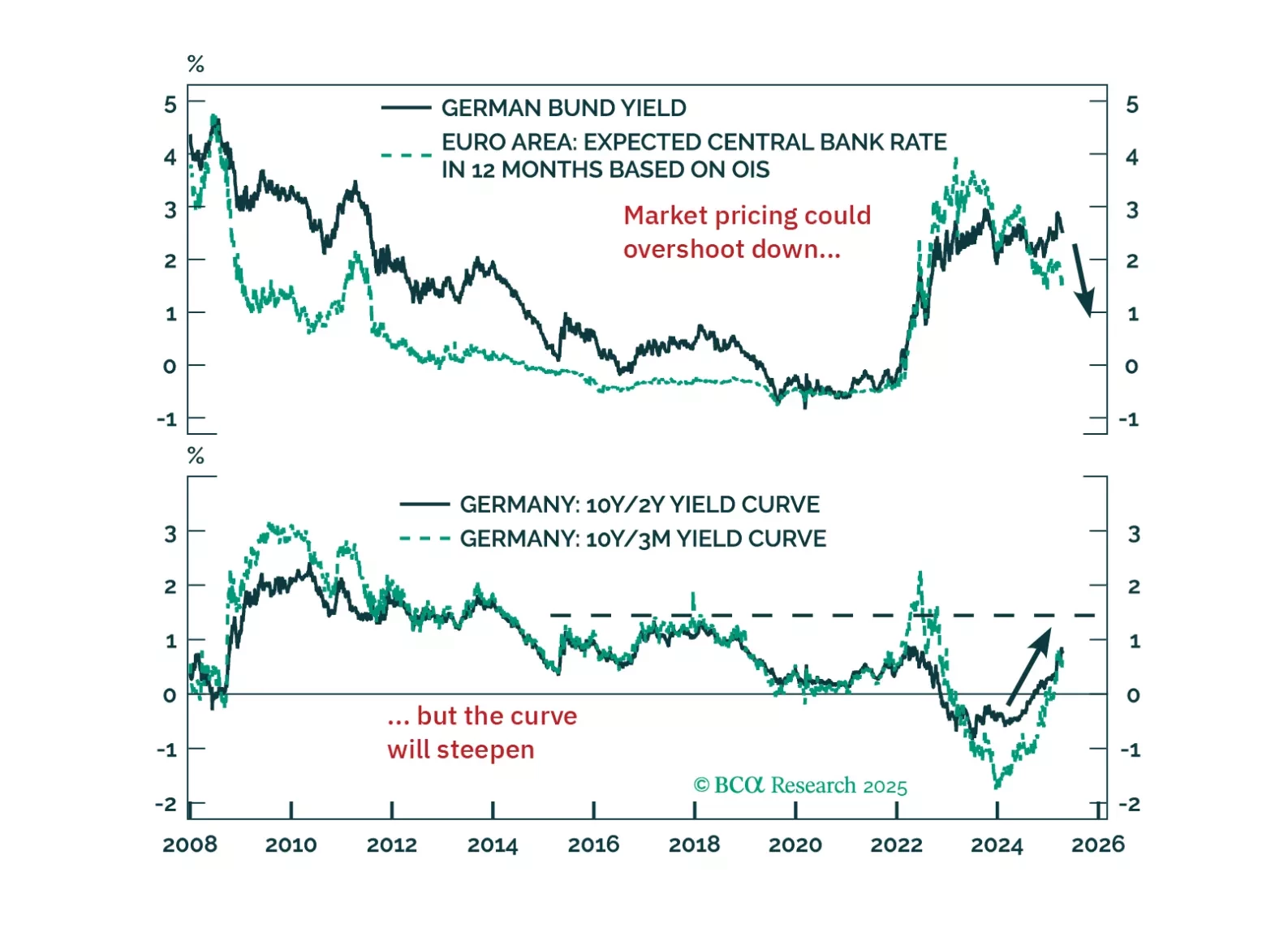

Europe’s deflation problem is getting harder to ignore. This week’s ECB cut is just the beginning — tariffs, the euro’s rally, and softening demand all point to more easing ahead. We explain what it means for yields, equities, and EUR/USD.

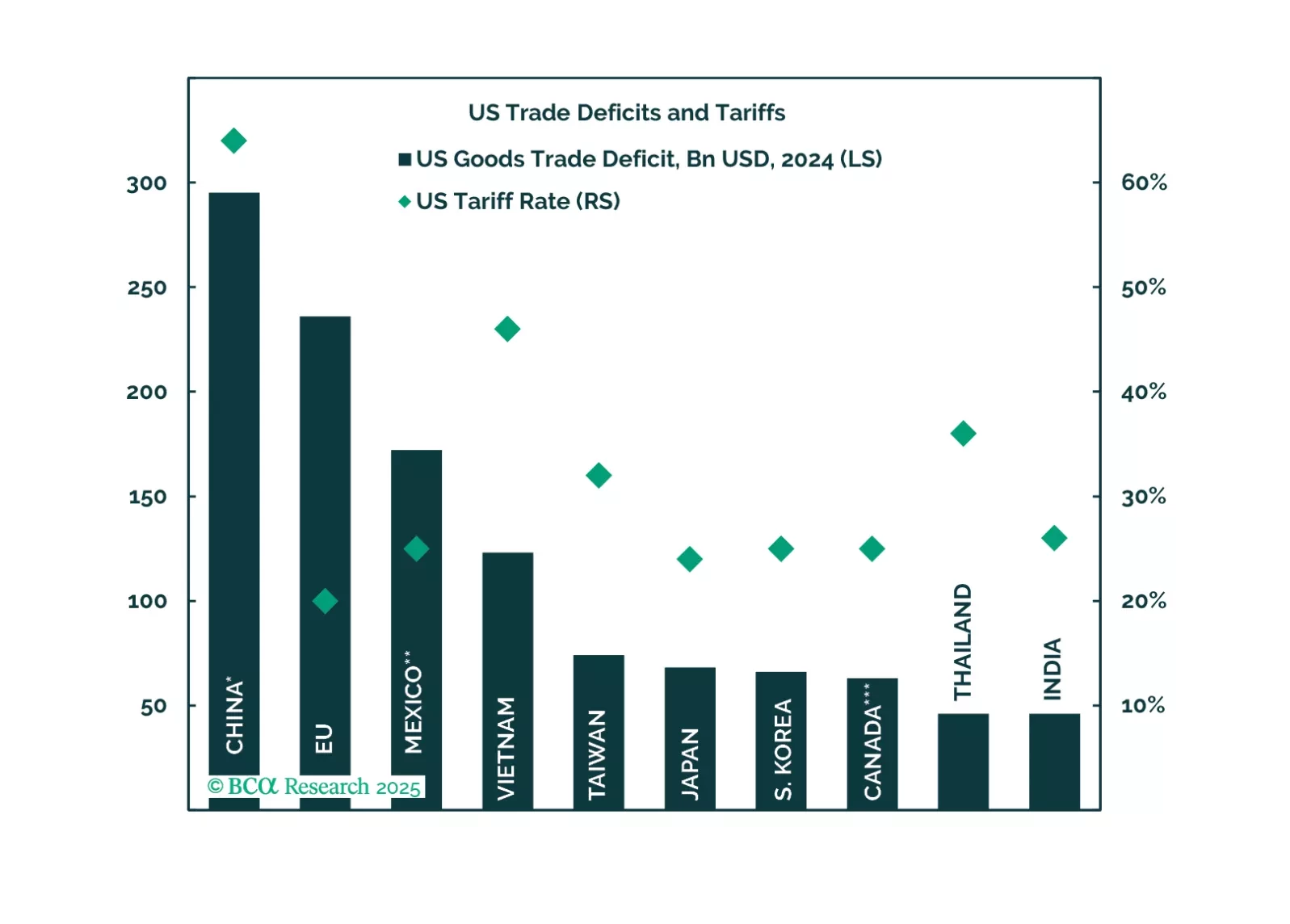

Trump's Tariff D-Day brings a negative surprise to financial markets already anxious over a declining US cyclical economy. Investors should sell risky assets, increase safe havens, and overweight US assets in the near term.