Latest from BCA Research

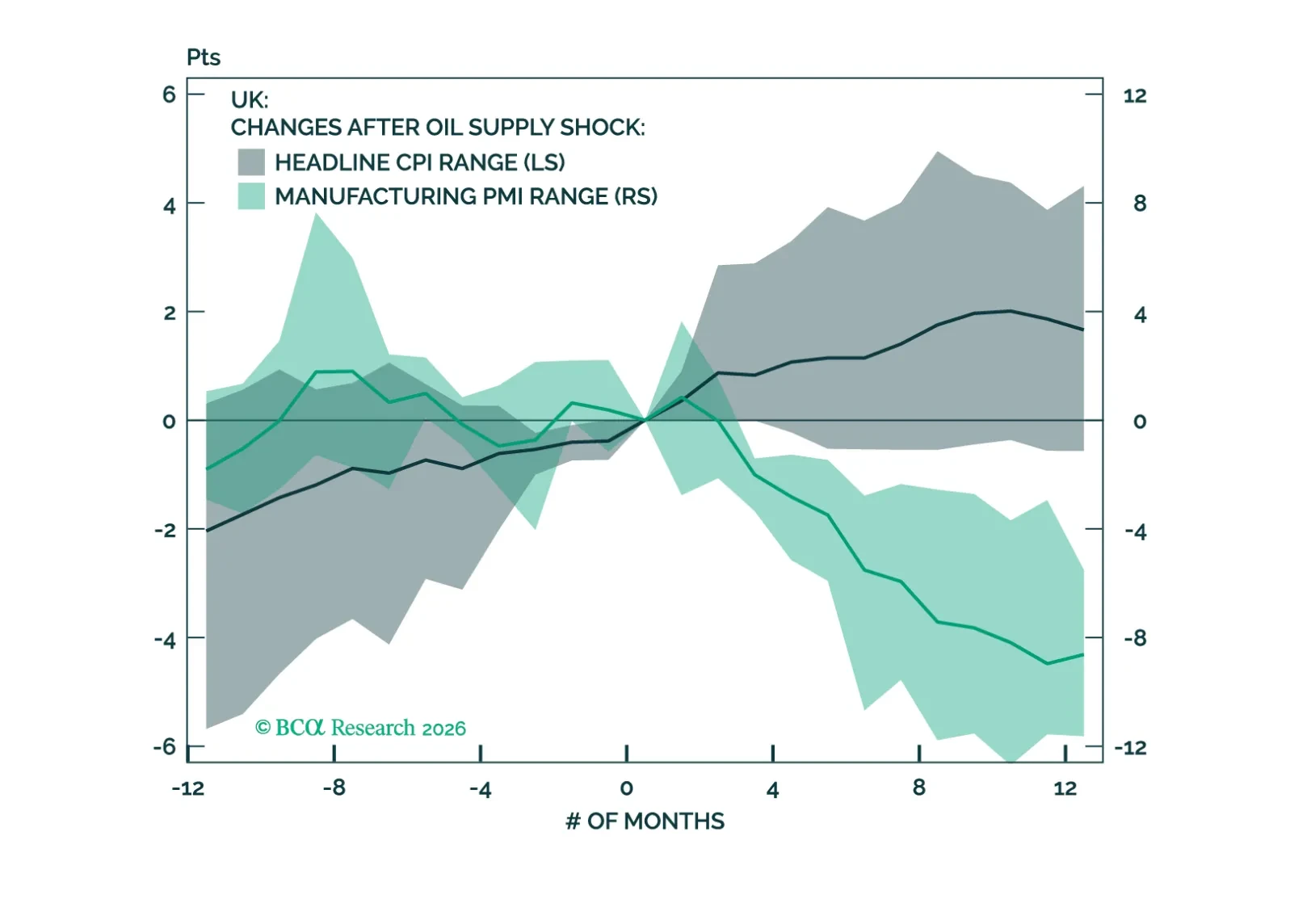

The UK economy is becoming increasingly fragile, but the investment outlook is improving. Slower growth and a more dovish BoE will support gilts, while UK equities will likely benefit from a favorable sector mix and a weaker pound.

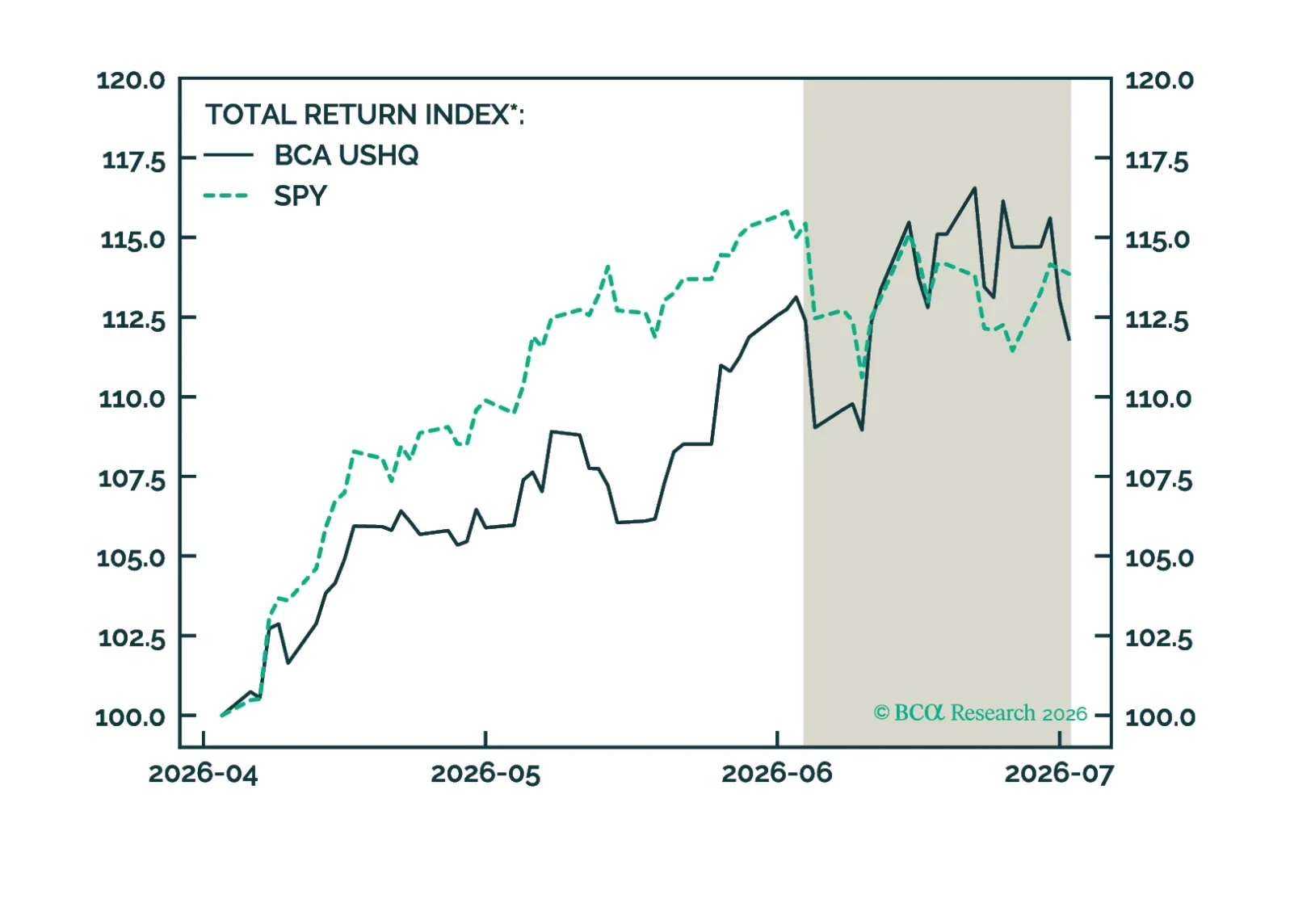

The US High Quality (USHQ) portfolio outperformed its benchmark through June, returning -0.50%, while its SPY benchmark returned -1.37%. On a trailing three-month basis, the USHQ portfolio’s performance was weaker than the benchmark, with USHQ underperforming by approx. 205bps.

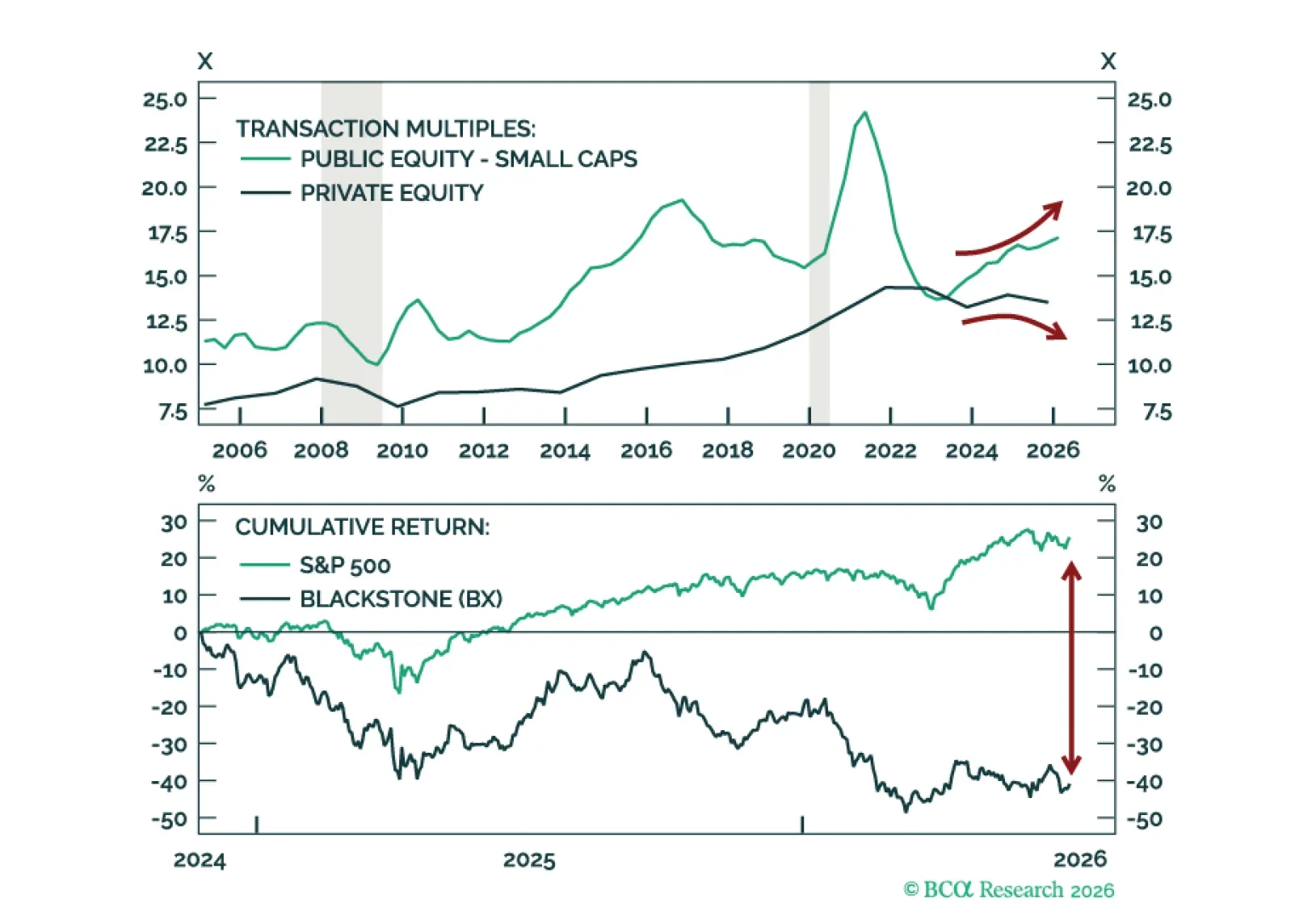

Beginning with this Quarterly report, The Global Asset Allocation and Private Markets teams are combining our quarterly outlooks into a single, unified framework, reflecting a more integrated approach to portfolio construction. In this joint outlook we upgrade Private Equity to overweight. Sentiment has soured, LPs are starved of distributions, flows have collapsed, valuations are trending lower, Secondaries are outperforming Primaries, and GP stocks are experiencing their worst underperformance on record. All signs of a durable bottom.

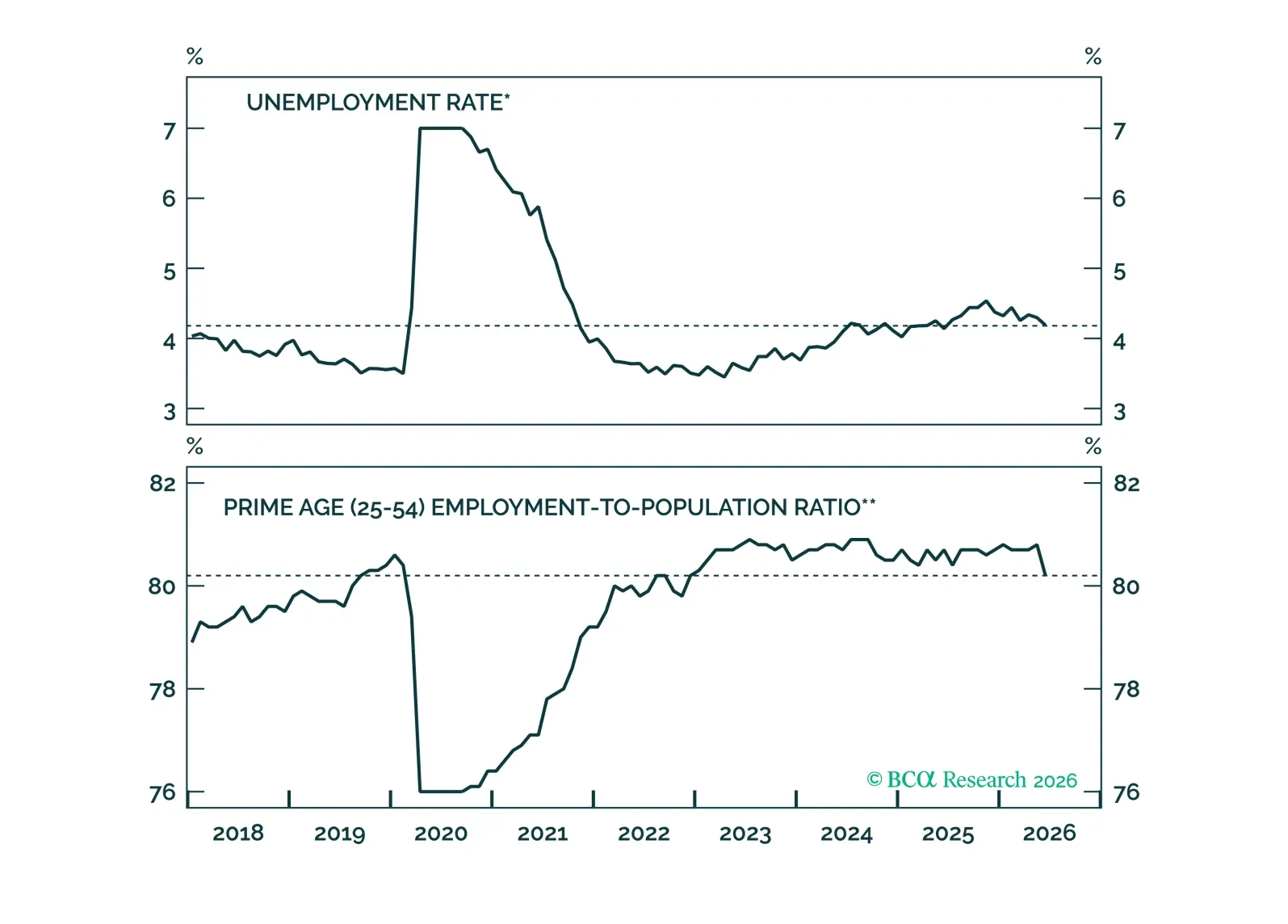

MacroQuant recommends underweighting equities and adopting a benchmark duration stance in fixed-income portfolios. The model is very positive on the US dollar, bearish on gold, neutral on copper, and bullish on oil.

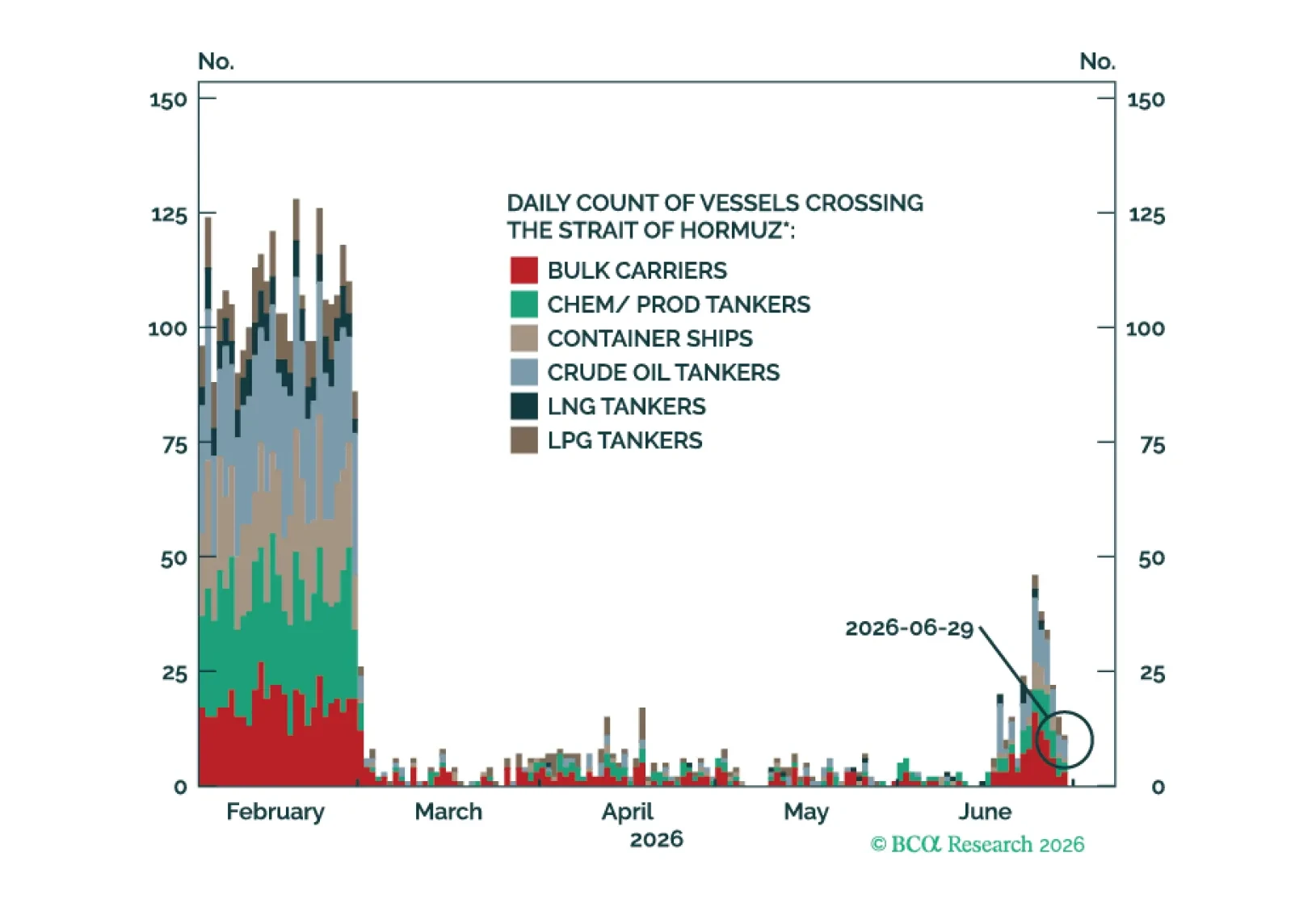

Geopolitical risk may rotate to Russia/Ukraine in Q3, while the Middle East could reignite in Q4.

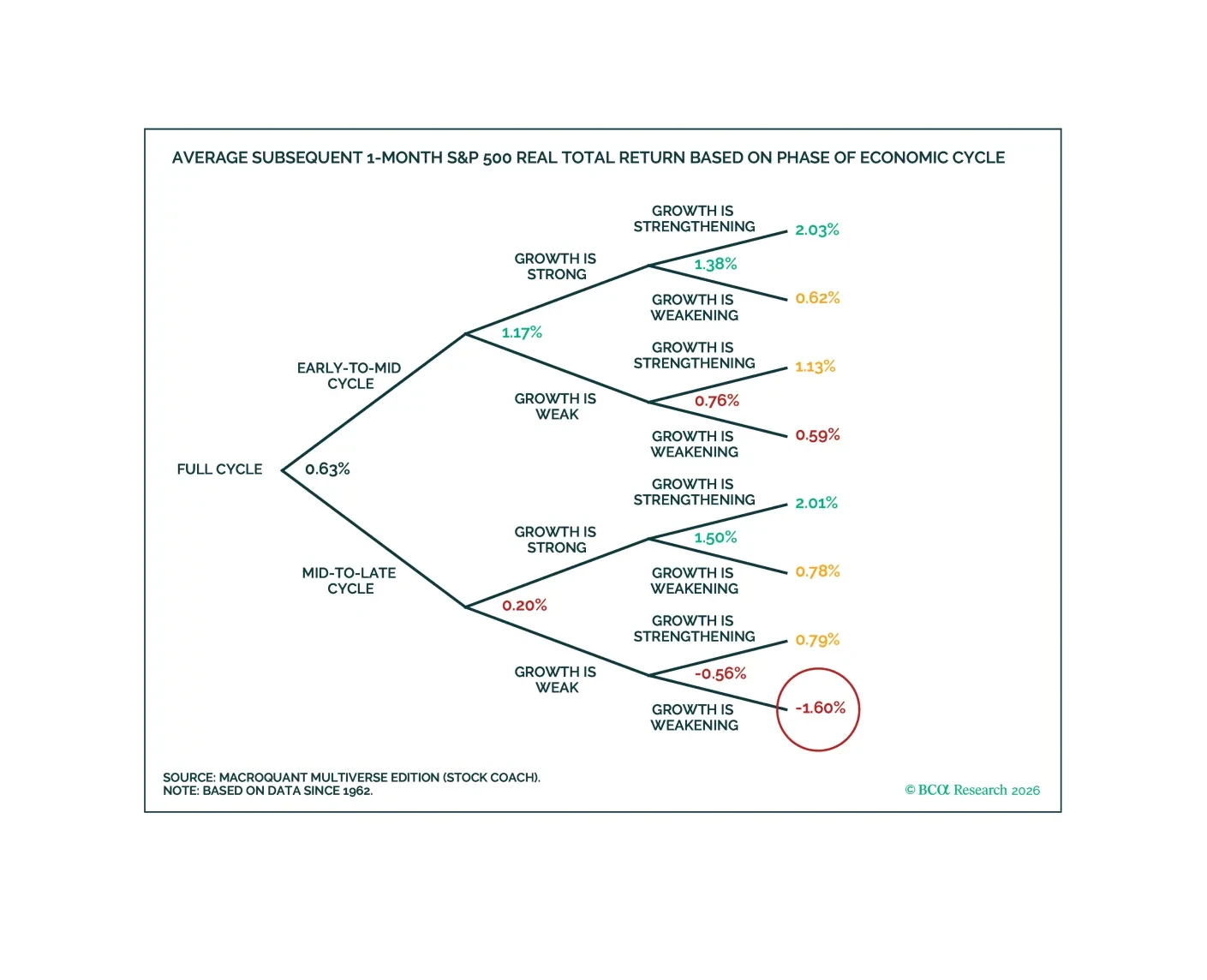

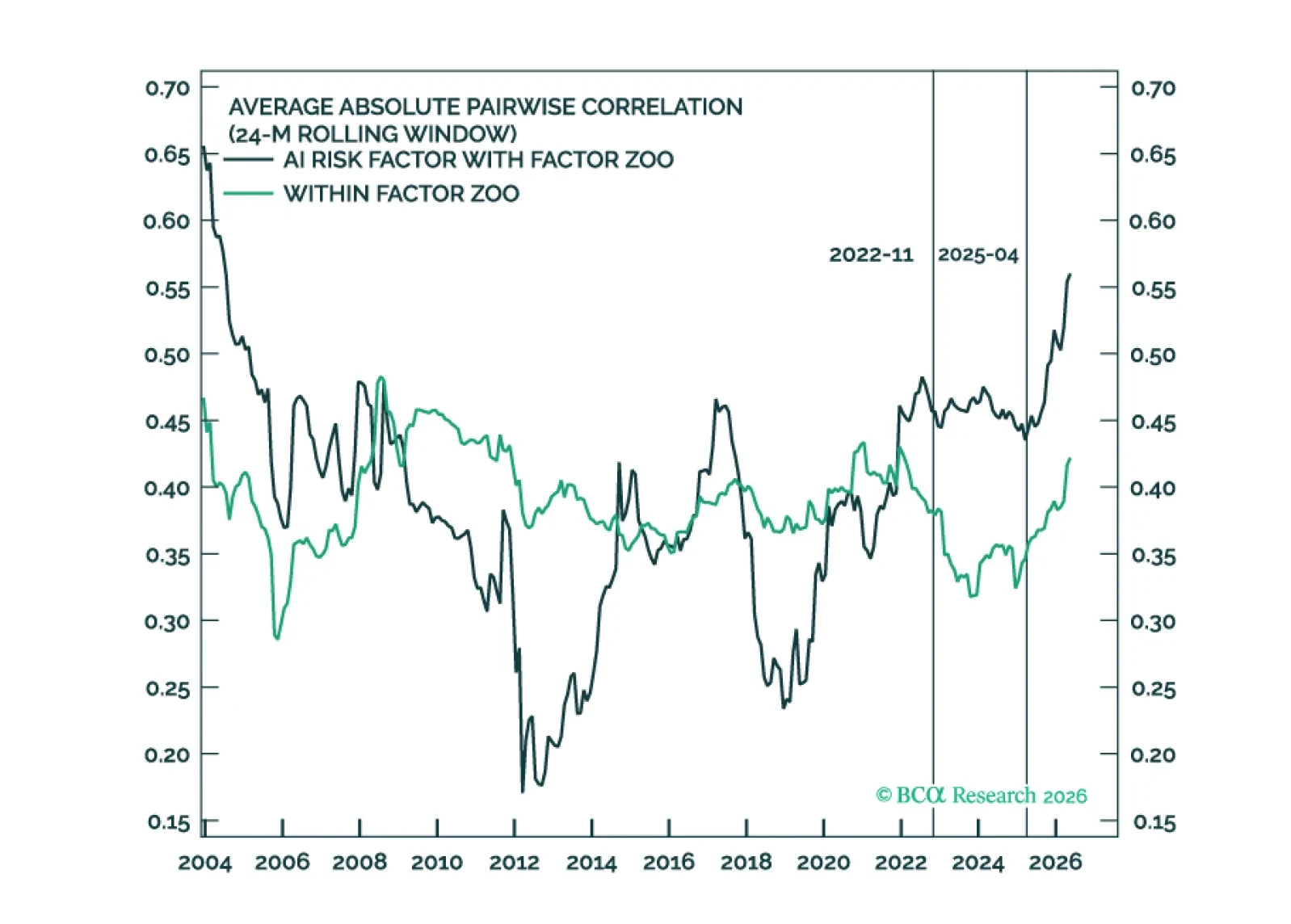

The S&P 500 has become increasingly concentrated. We know that. But the critical question is not how many stocks are driving the market; it is how many factors are driving stocks. We define an AI risk factor to test whether AI has become the dominant common exposure throughout much of the factor zoo.