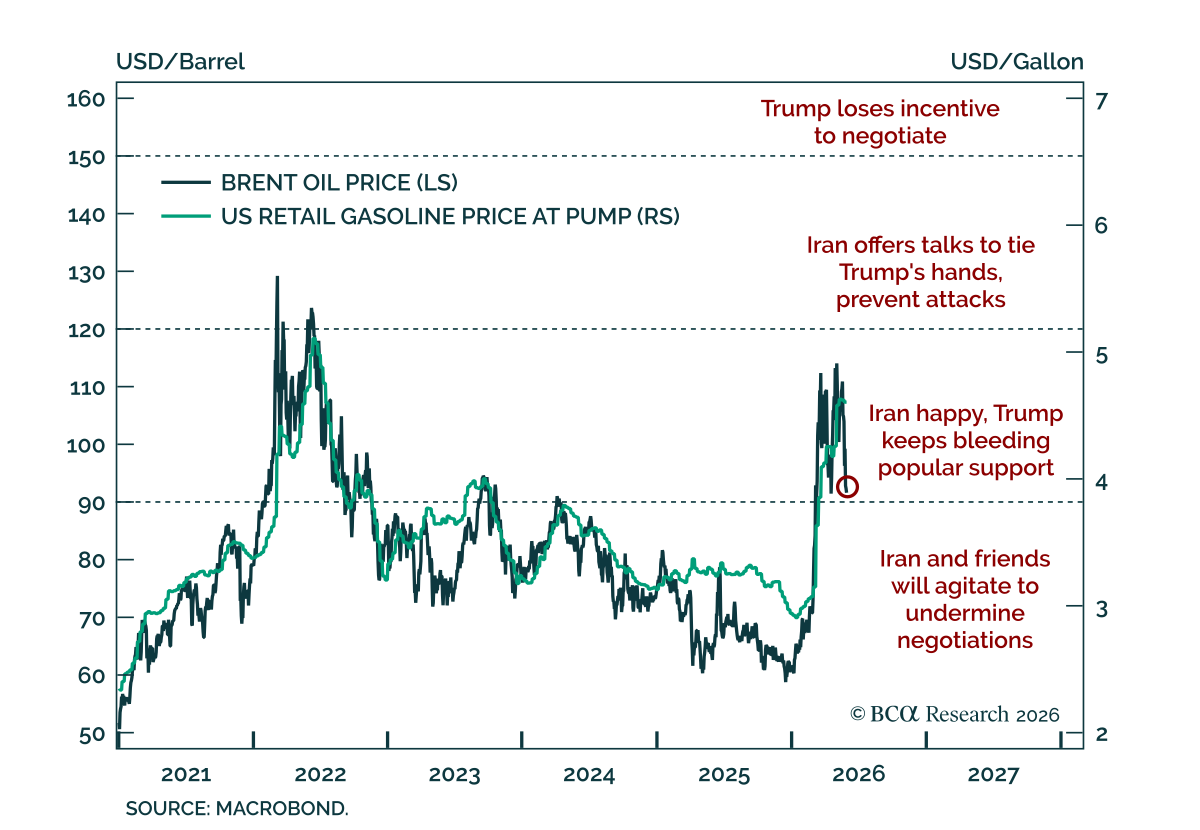

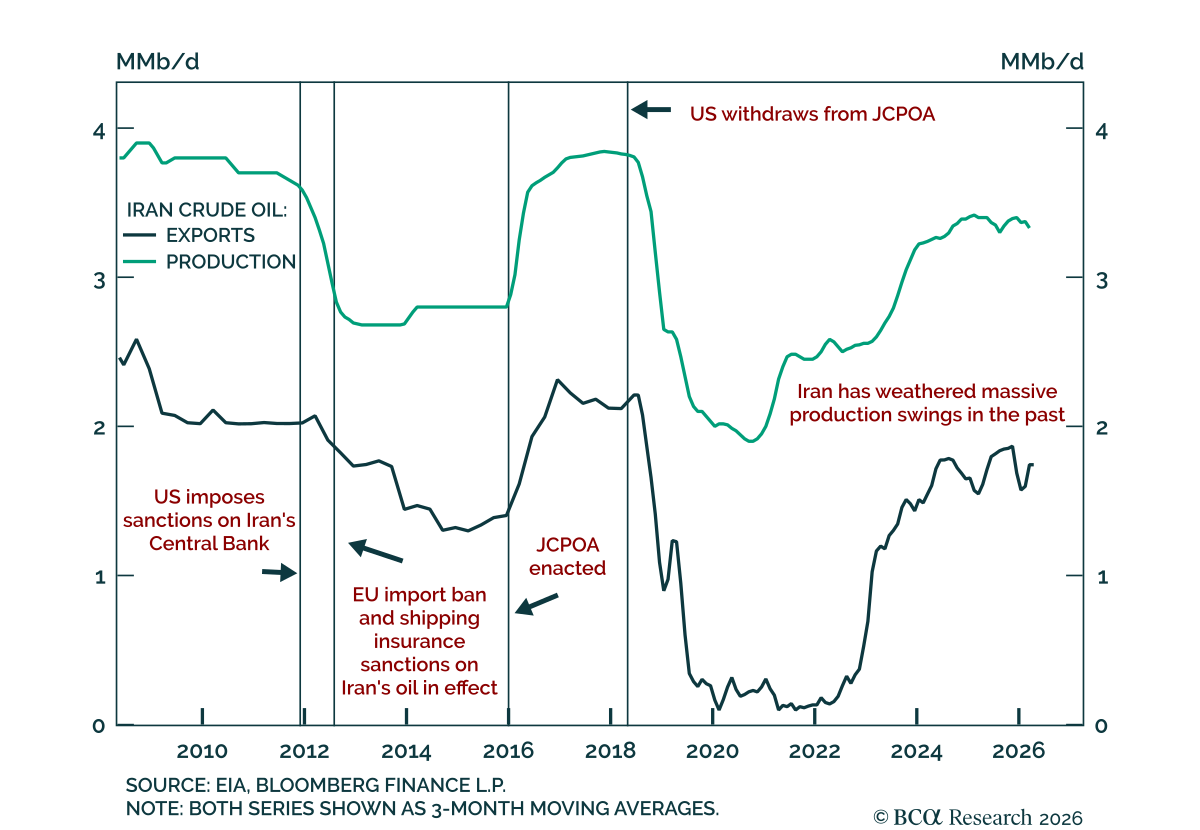

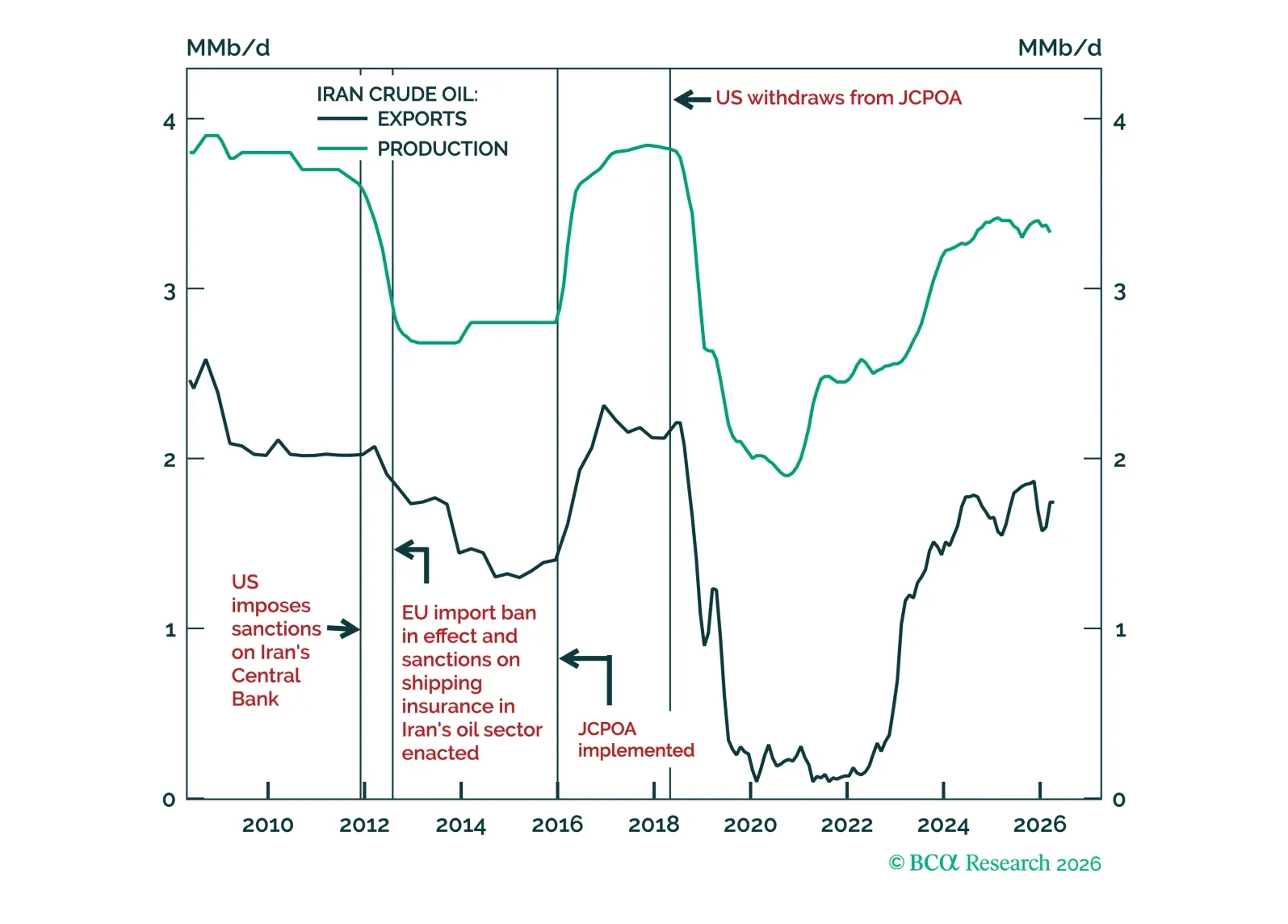

Iran

US-Iran talks are again under strain after Monday’s exchange of fire and Israel’s attacks in Lebanon, but the escalation cycle still remains negotiations-driven and at least a short-term deal that restarts shipping this summer remains likely. Oil rose more…

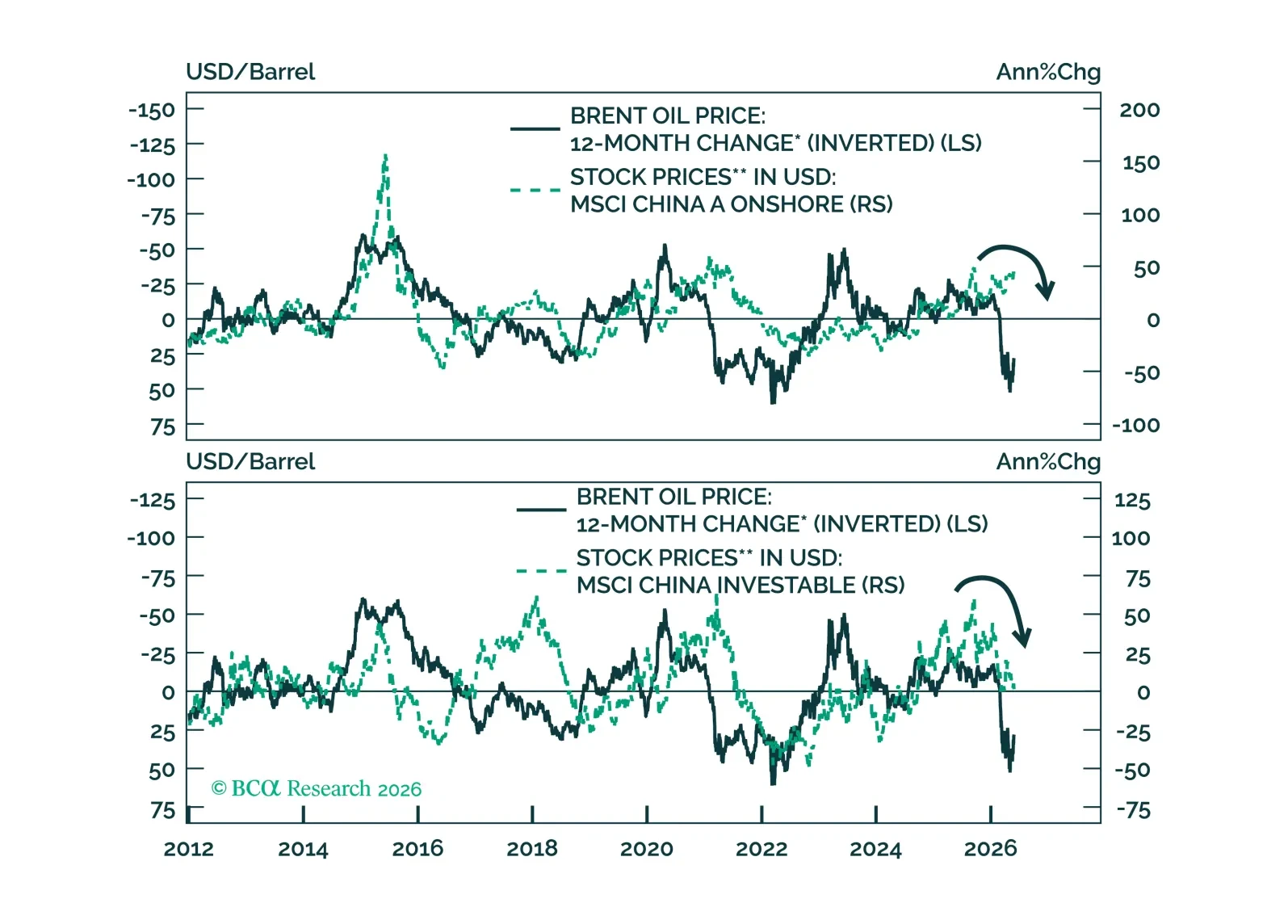

Oil shocks hit economies with a lag. China will feel the delayed pain of surging oil prices, pushing Beijing toward infrastructure spending as its main tool to prop up growth.

A 60-day ceasefire extension would buy the global economy some time, but it would not resolve the underlying supply problem. Oil prices and bond yields fell while equities rallied Tuesday morning after Trump announced…

I spent the last week in London, speaking to a wide array of BCA Research clients. Throughout the early part of the week, well connected friends and sources in the Middle East warned me that a renewed US attack on Iran was imminent (by Friday, May 22, after the market close, bien sûr). Several clients with hefty AUM’s – and thus an impressive geopolitical consulting budget – in London confirmed that the US attack was all but assured.

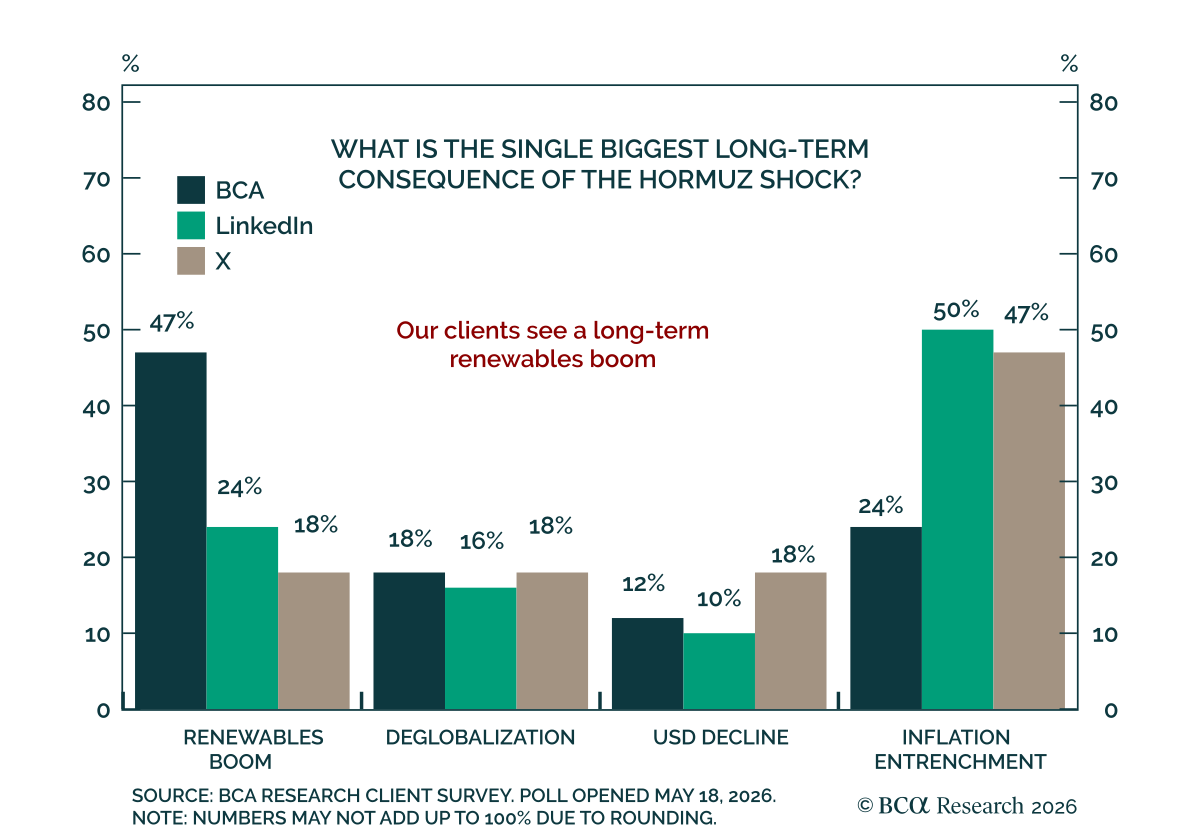

Our clients are split on the Hormuz shock’s long-term consequences. In last week’s poll, we asked what the single biggest long-term consequence would be. BCA clients leaned toward a renewables boom, chosen by 47%, while 24% pointed to inflation entrenchment.…

Our Commodity strategists expect oil prices to move higher as de-escalation hopes fade and Strait of Hormuz supply risks reassert themselves. Recent volatility reflect headline-driven uncertainty, with markets swinging between prospects of an imminent Strait…

Hopes for an imminent Middle East de-escalation have capped oil prices in recent weeks, but that restraint may soon fade.

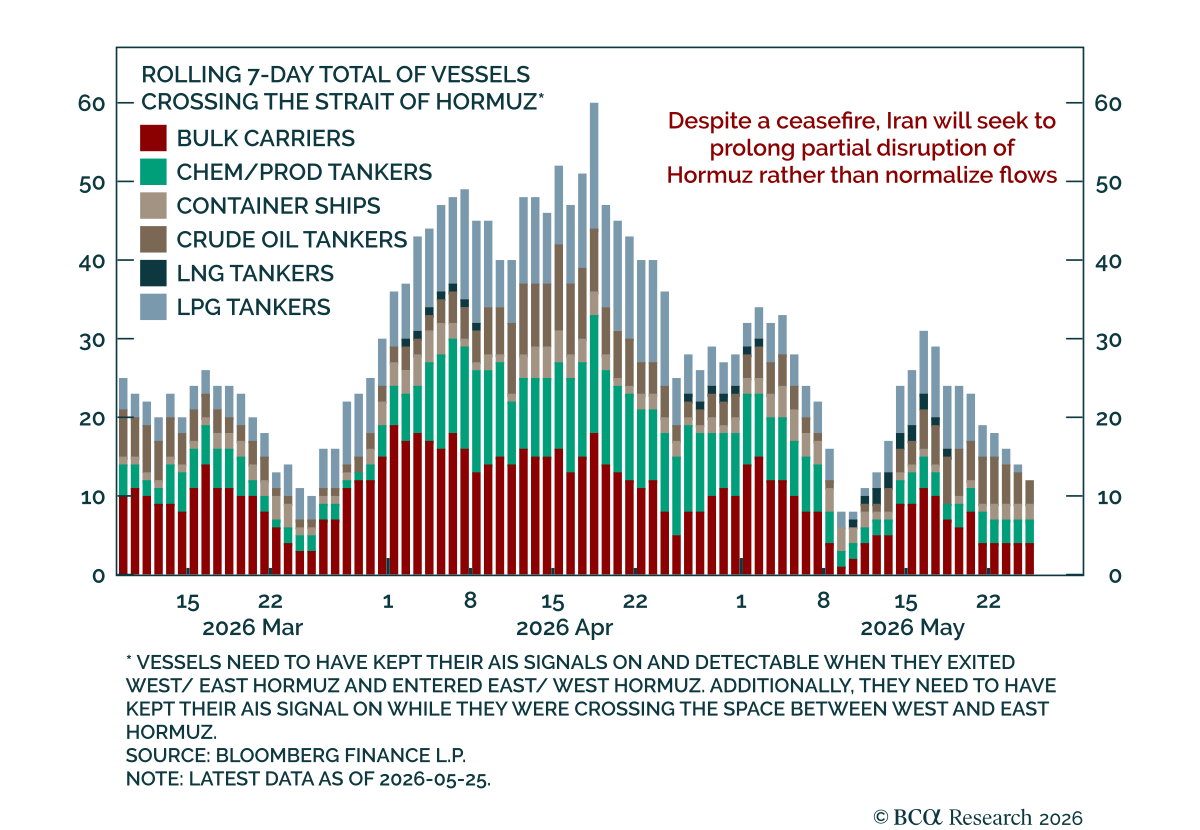

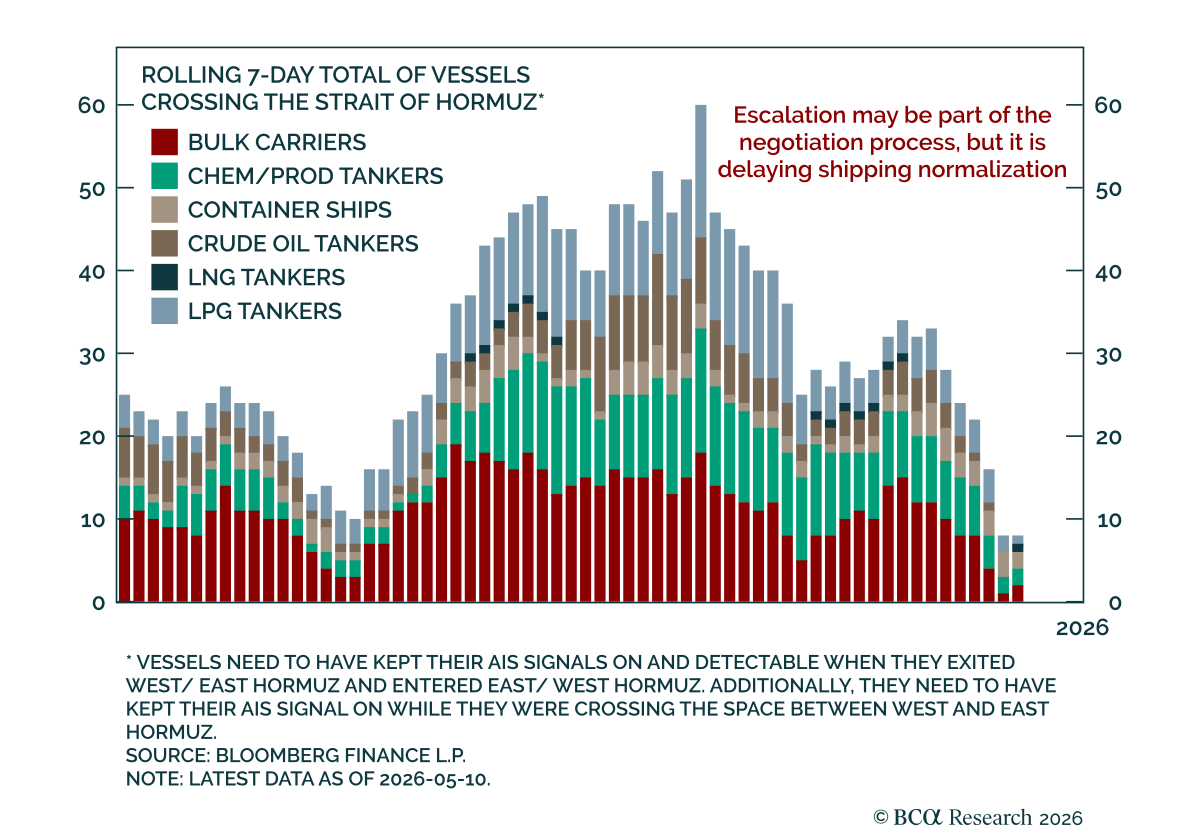

The Middle East returned to the headlines over the weekend, and any normalization of Hormuz shipping now looks delayed. President Trump called Iran’s response to the US peace proposal “totally unacceptable.” Our Geopolitical strategists still see Iran as…

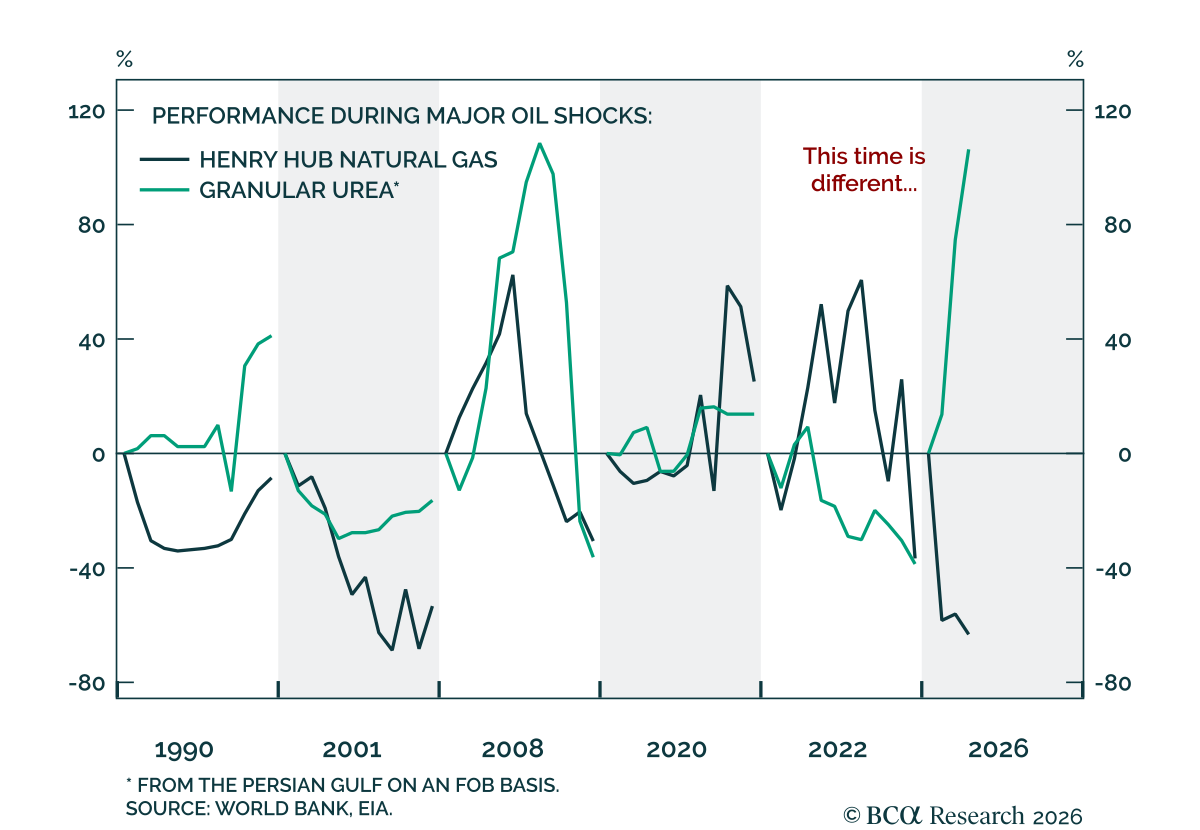

The Hormuz crisis is likely to disrupt urea markets; trade routes and production capacity can only adjust slowly and at meaningful cost. Our Chart Of The Week comes from Jose Yanes, analyst in our GeoMacro team. In the Hormuz crisis, urea sits…

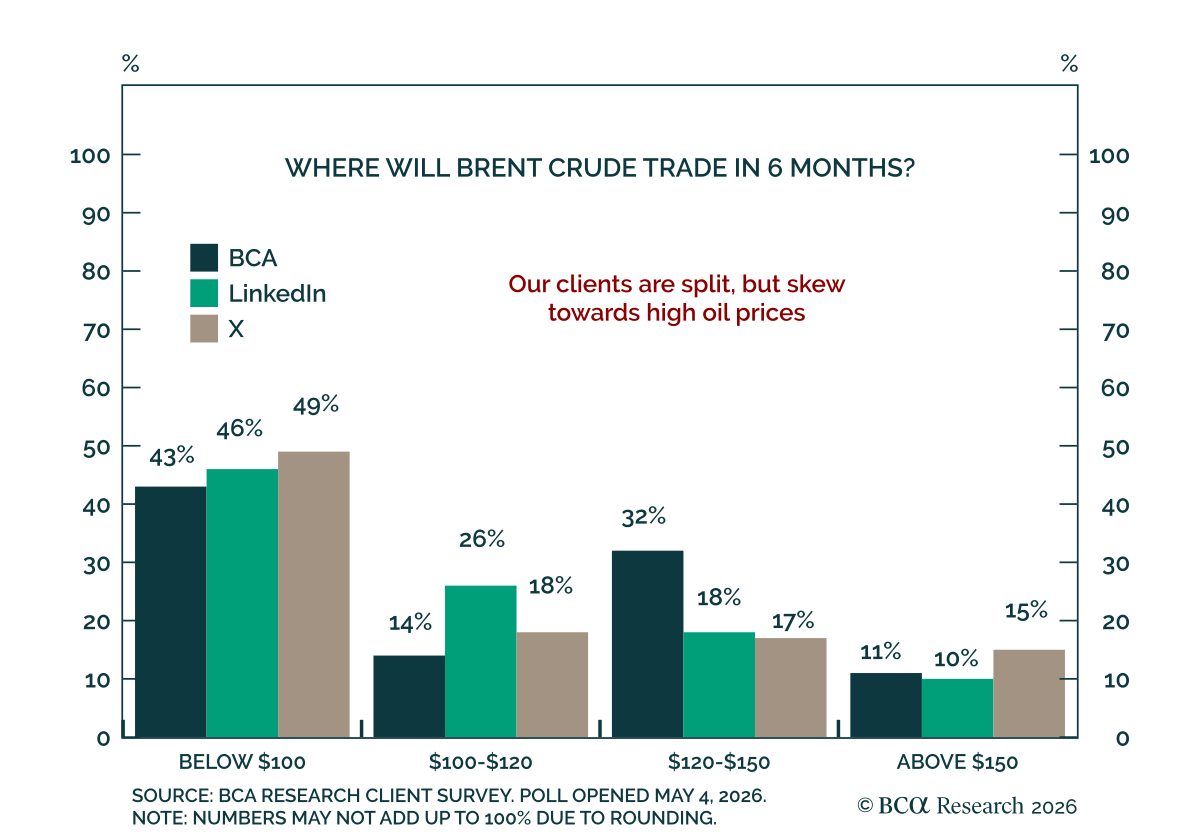

Our clients are split on whether Brent will be below $100 in 6 months. In last week's poll, we asked where Brent crude will trade in 6 months. 43% of BCA clients expect sub-$100/bbl prices, while 32% see Brent in the $120–$150 range, 14% in $100–$120,…