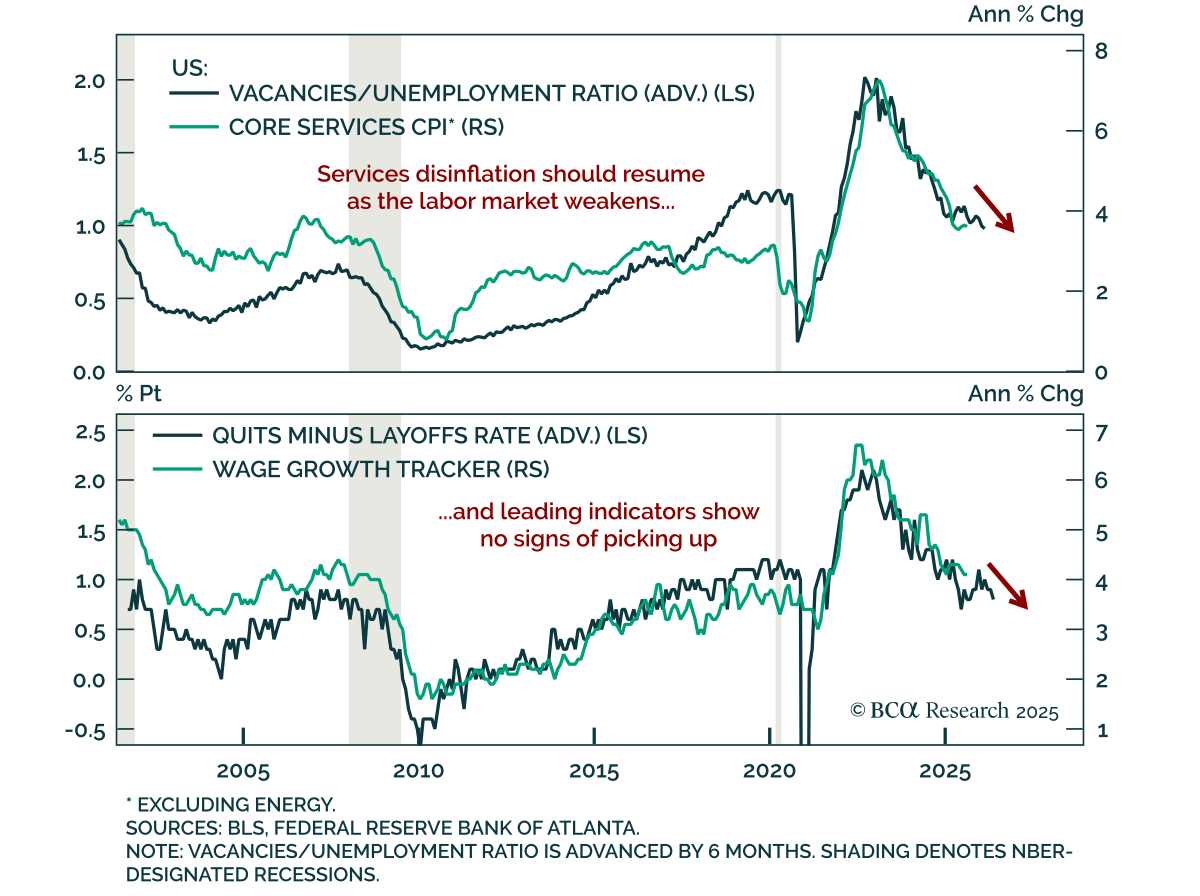

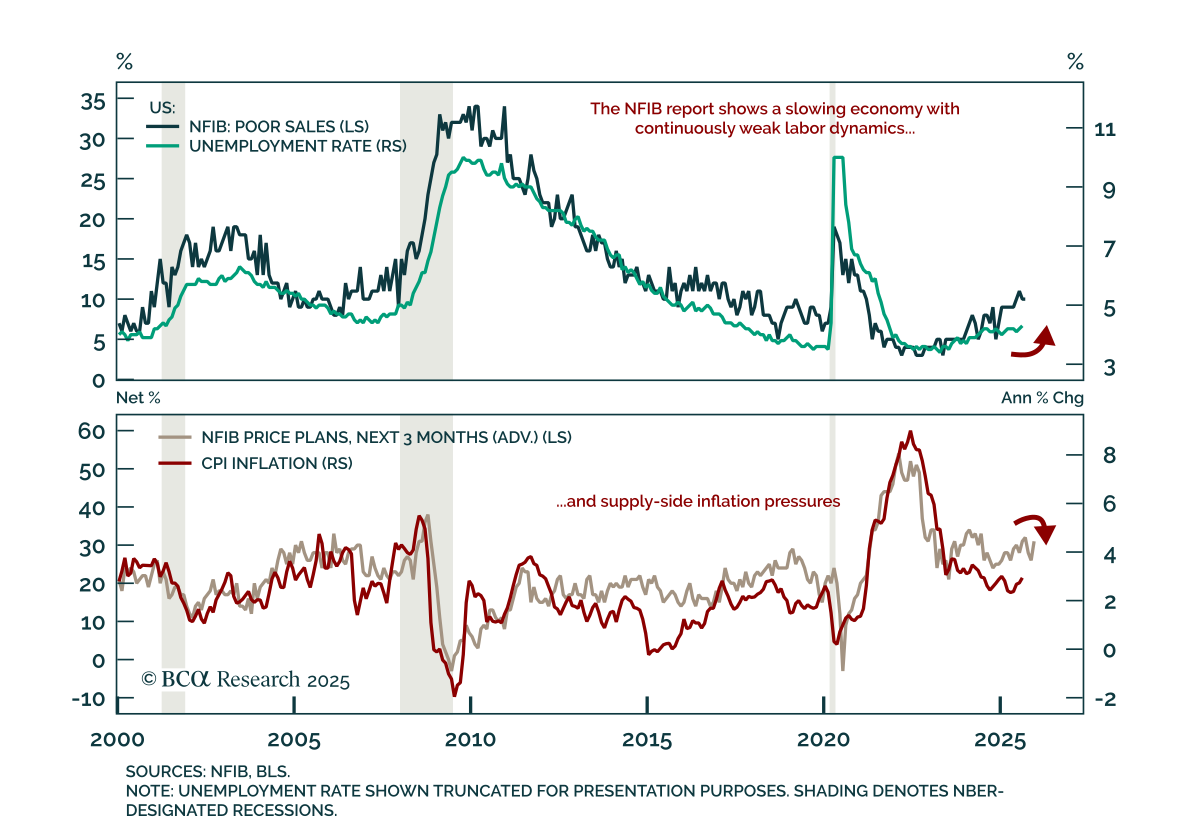

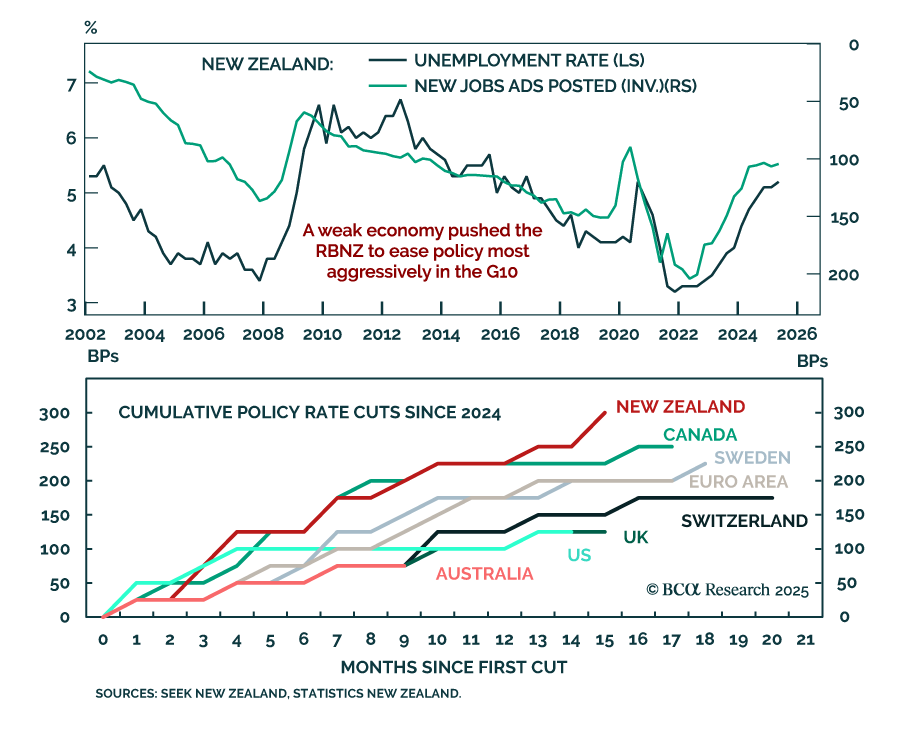

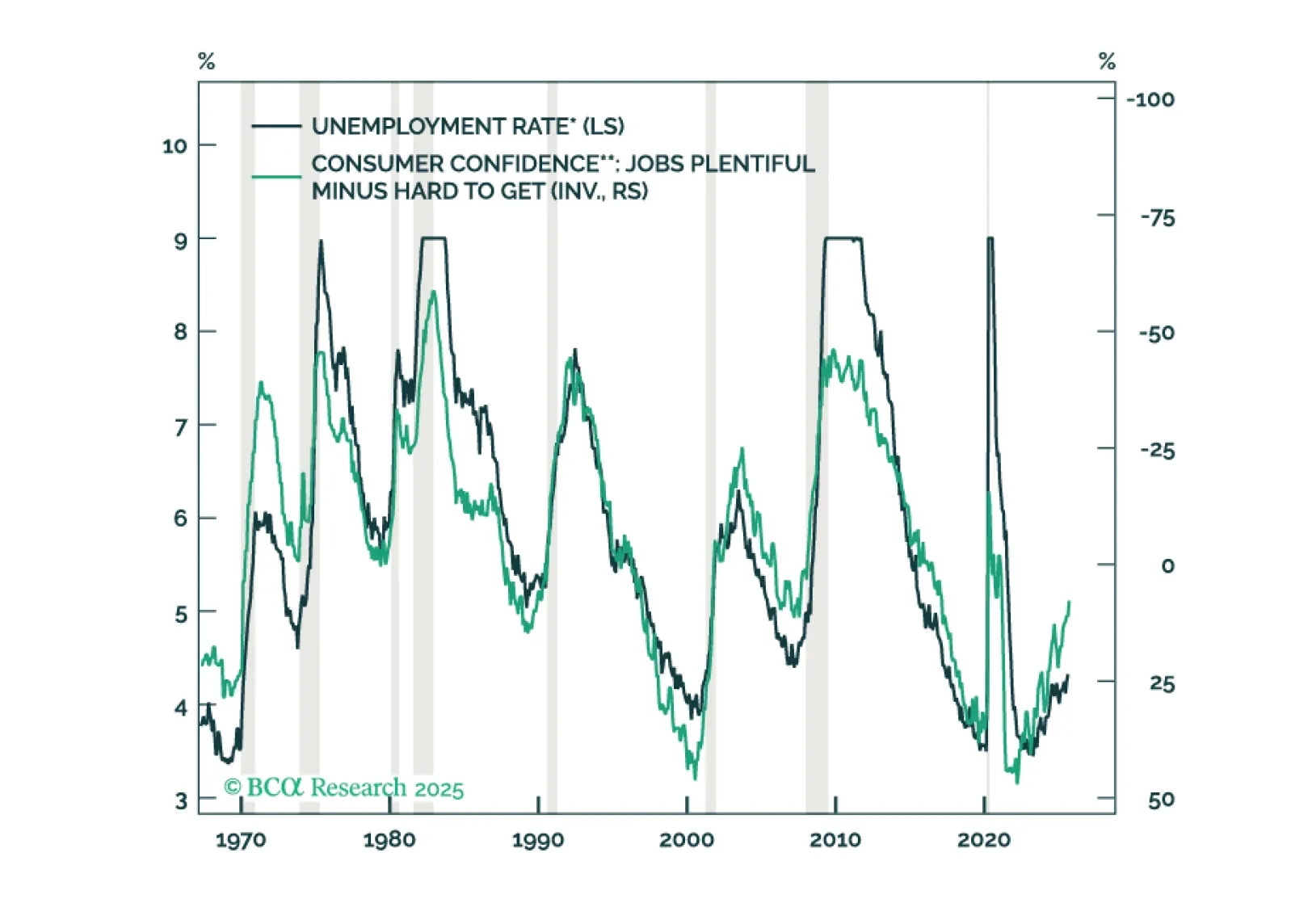

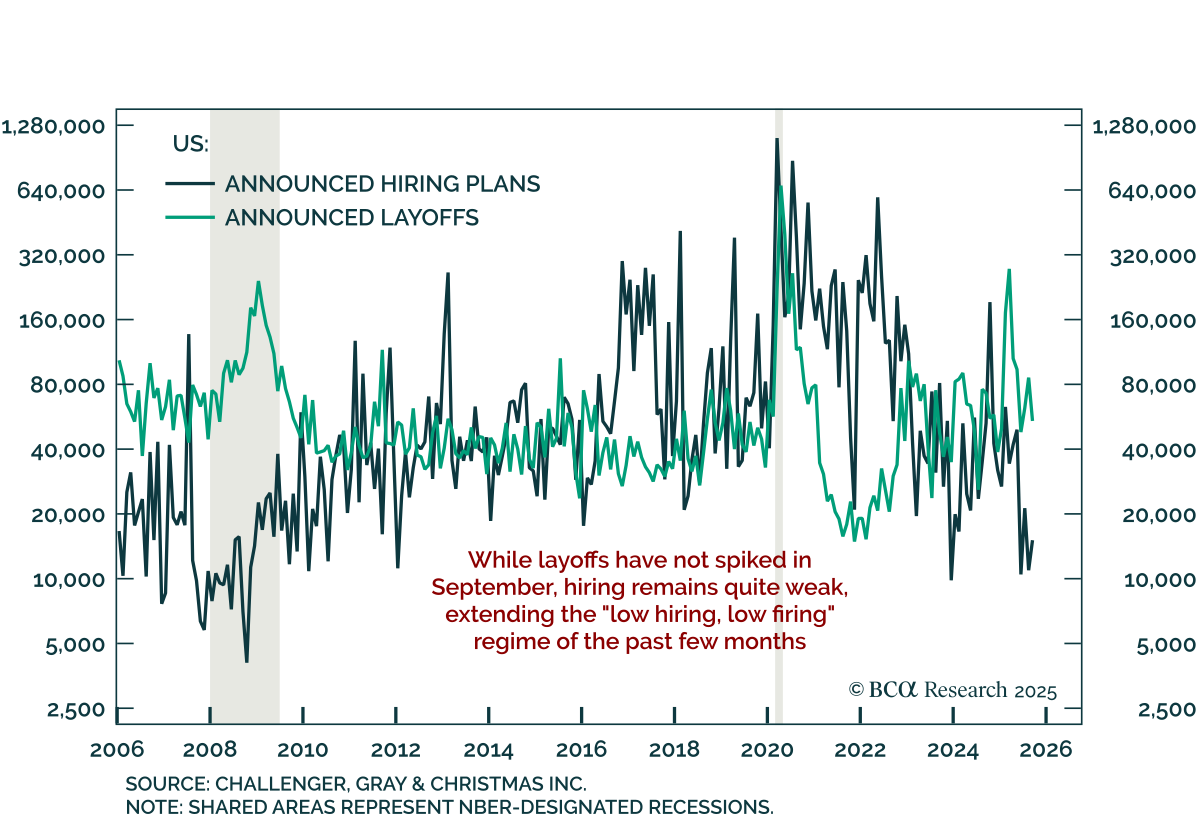

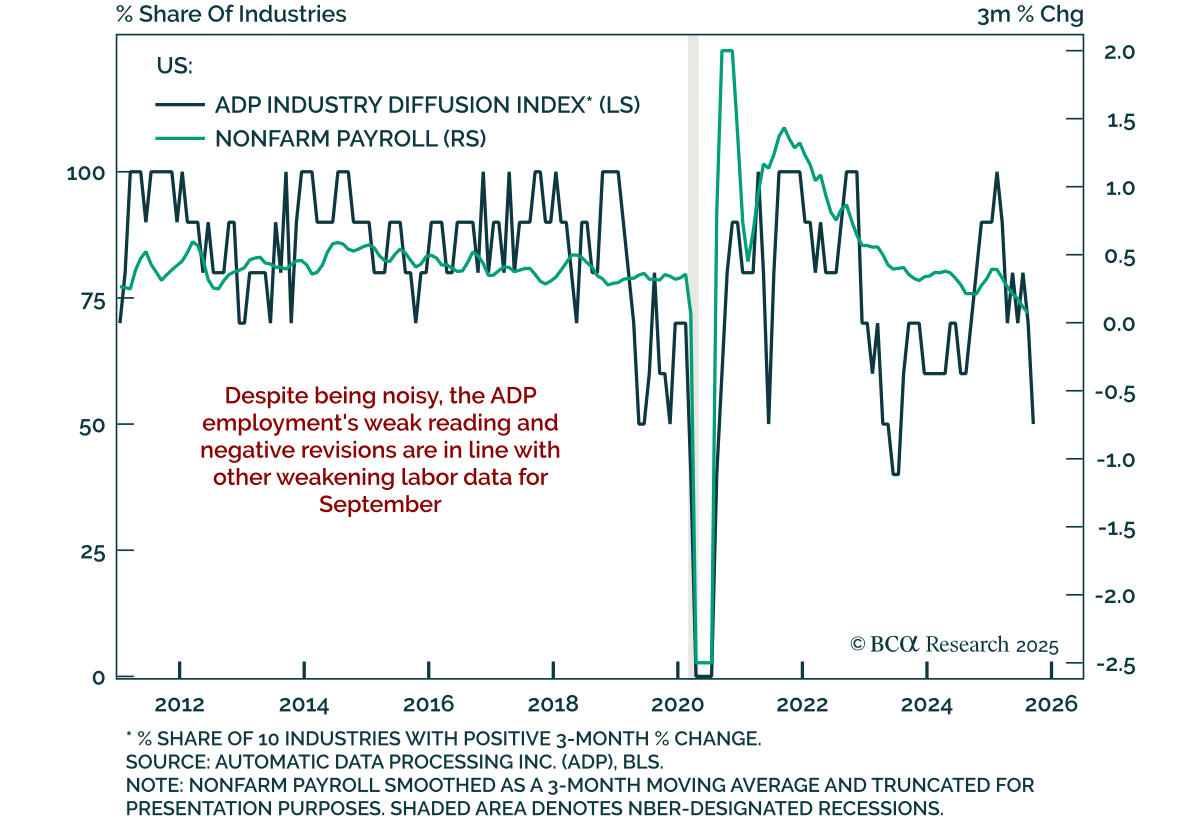

Labor Market

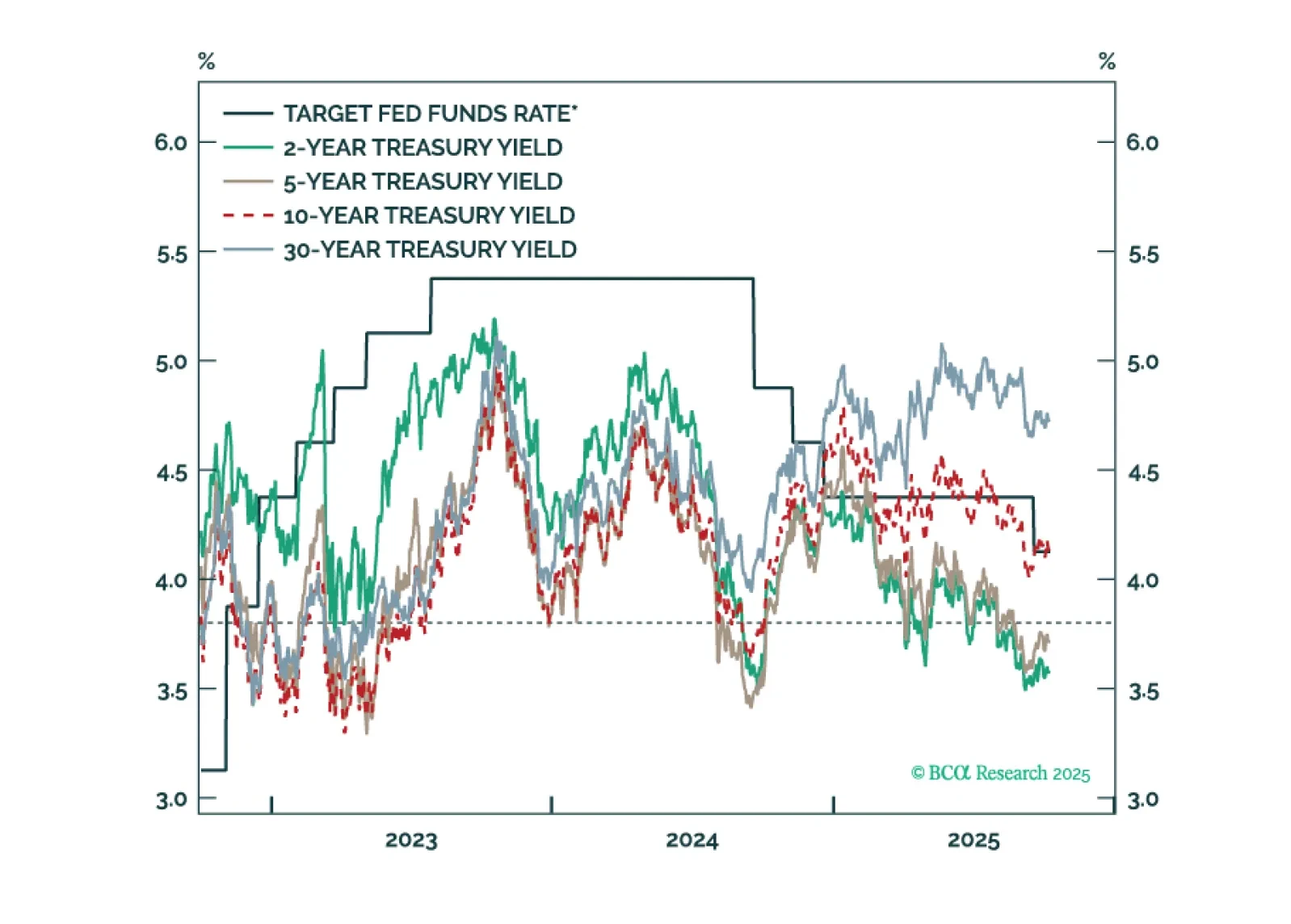

Treasury yields are generally following the pattern of past interest rate cycles, but with a larger term premium keeping the curve steeper than usual.

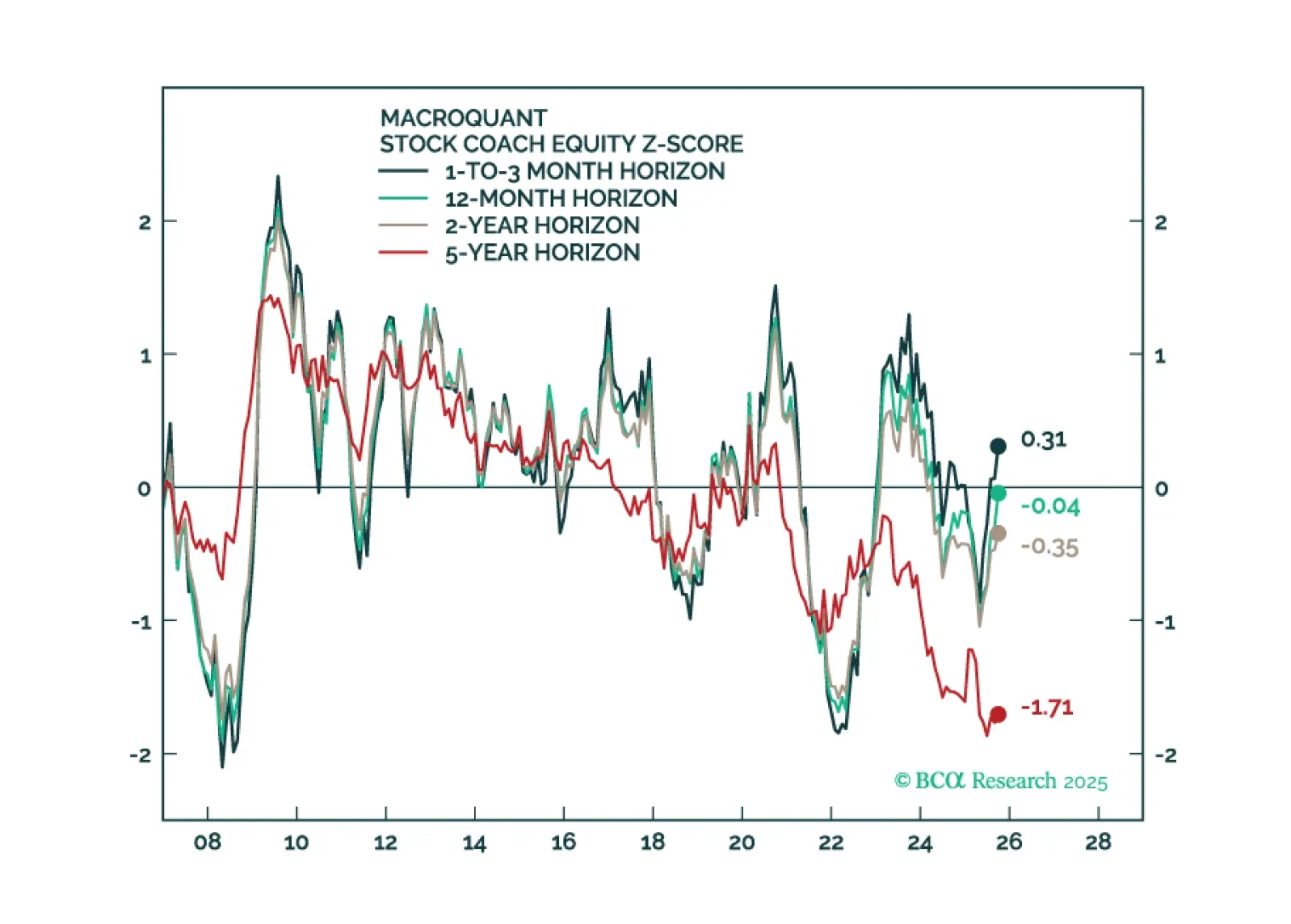

In this Q4 Strategy Outlook, we discuss where we stand on our recession call, the outlook for stocks and bonds in various scenarios, why investors are misunderstanding the impact of AI on corporate profits, whether the US dollar has entered a structural downtrend, our perspective on the yen, gold and other commodities, and much more.

Our Portfolio Allocation Summary for October 2025.

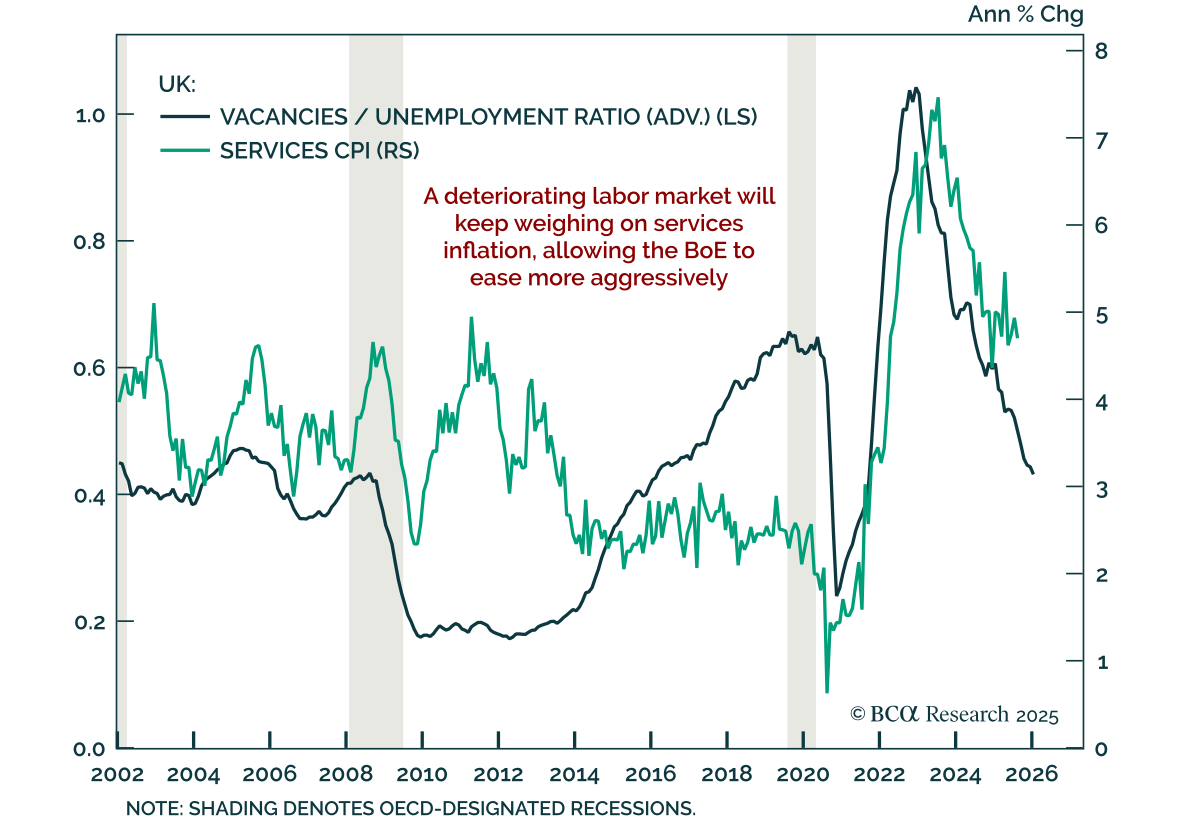

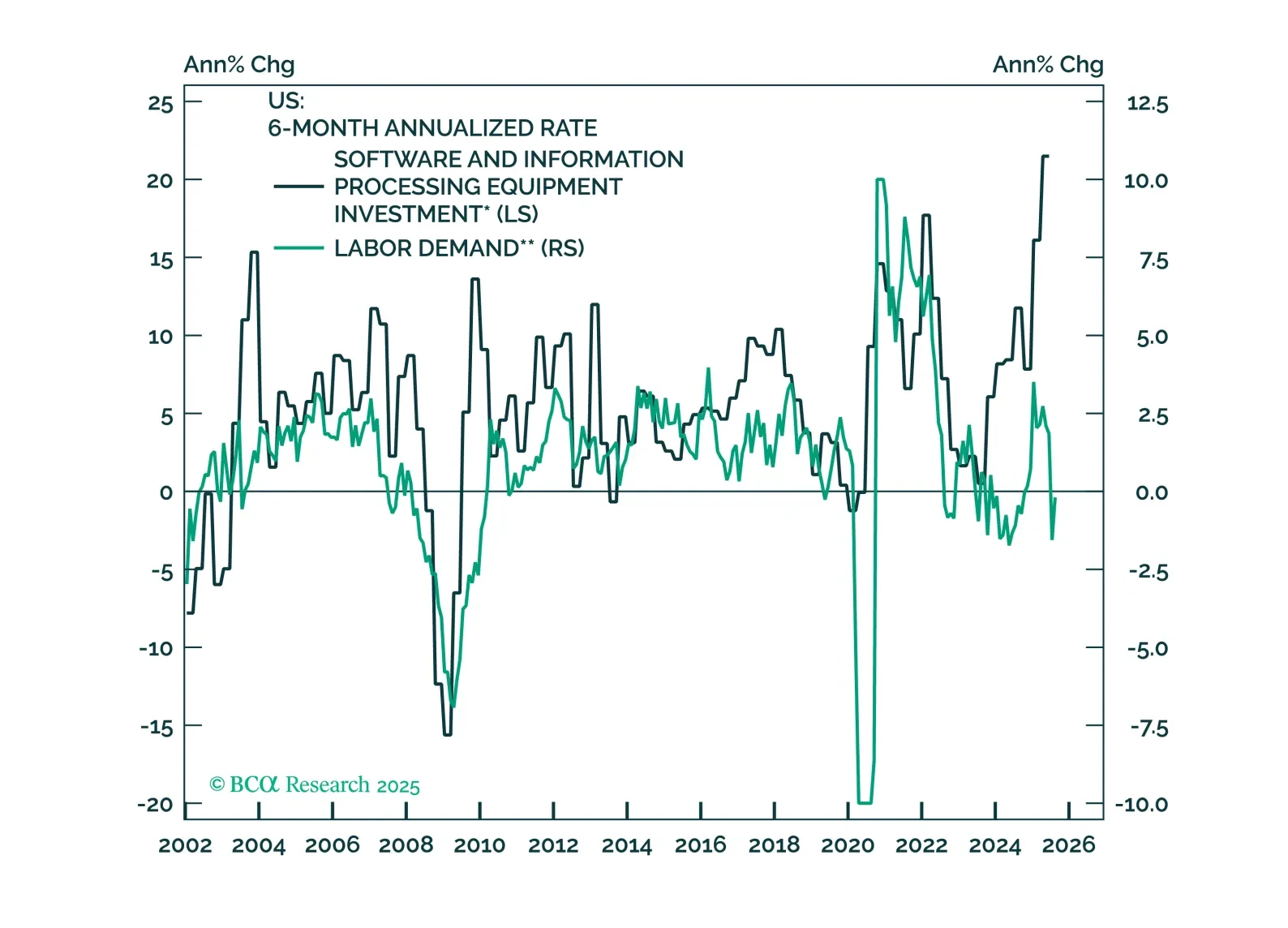

Big Tech and the Trump administration are engineering an industrial boom that favors American hardware over American workers. Economic growth will be robust in the US but the labor market will stay relatively sluggish. Adopt an overweight stance on both equities and fixed income and underweight on cash. Upgrade Canadian equities and downgrade the UK. Upgrade Industrials and downgrade Consumer Staples. Upgrade EM Debt. Downgrade Private Credit.