Fiscal

On purely macroeconomic terms, the US economy appears to be heading towards a recession. But the whole point of our framework – GeoMacro – is to forecast the interplay between politics, geopolitics, and macro. The White House is taking control of the Fed in 2026 and, together, they will look to re-lever the US consumer.

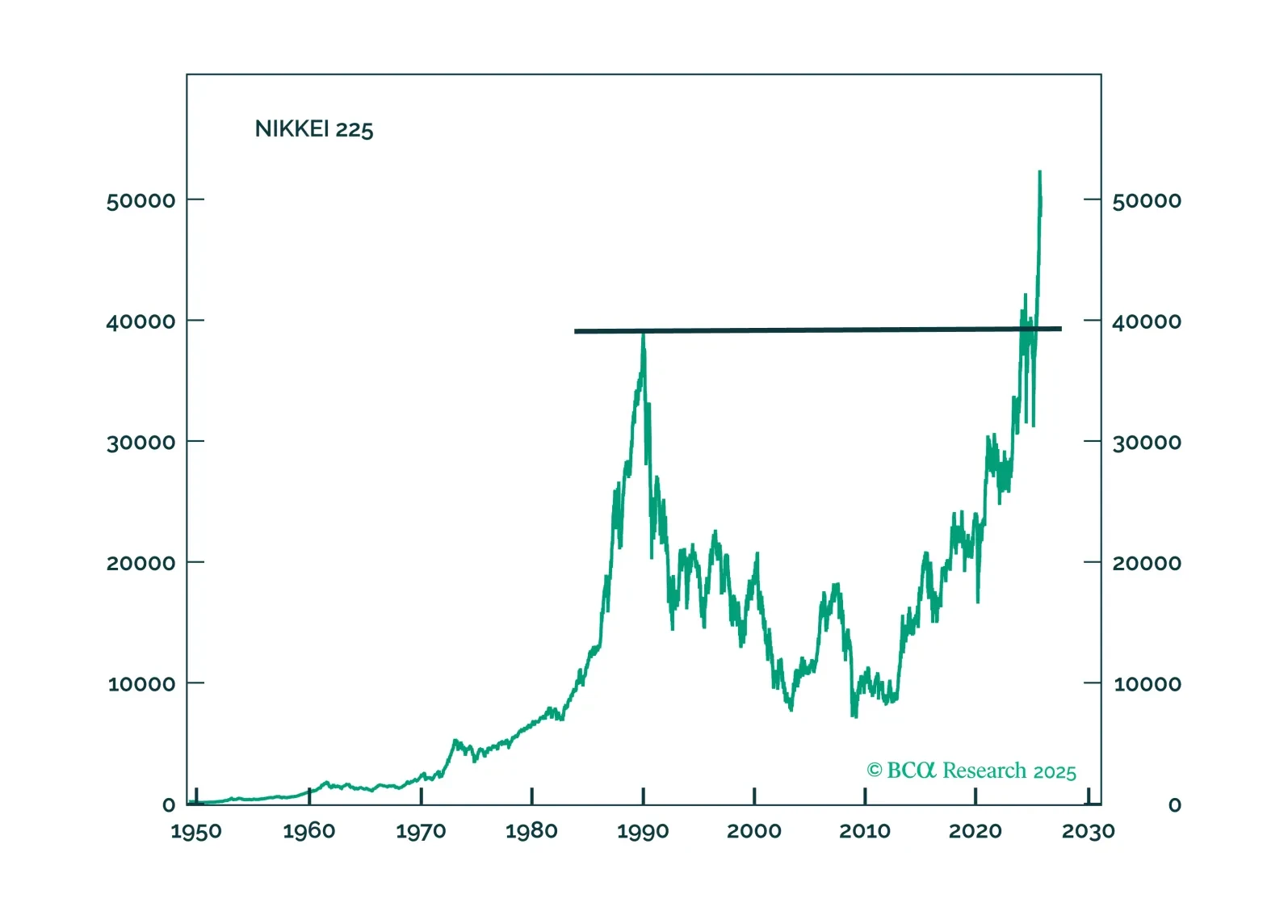

Japanese financial assets will finally have unfettered access to outsized returns. This performance will come in fits and starts, but we are comfortable laying our cards down on buying the yen, and Japanese industrial stocks.

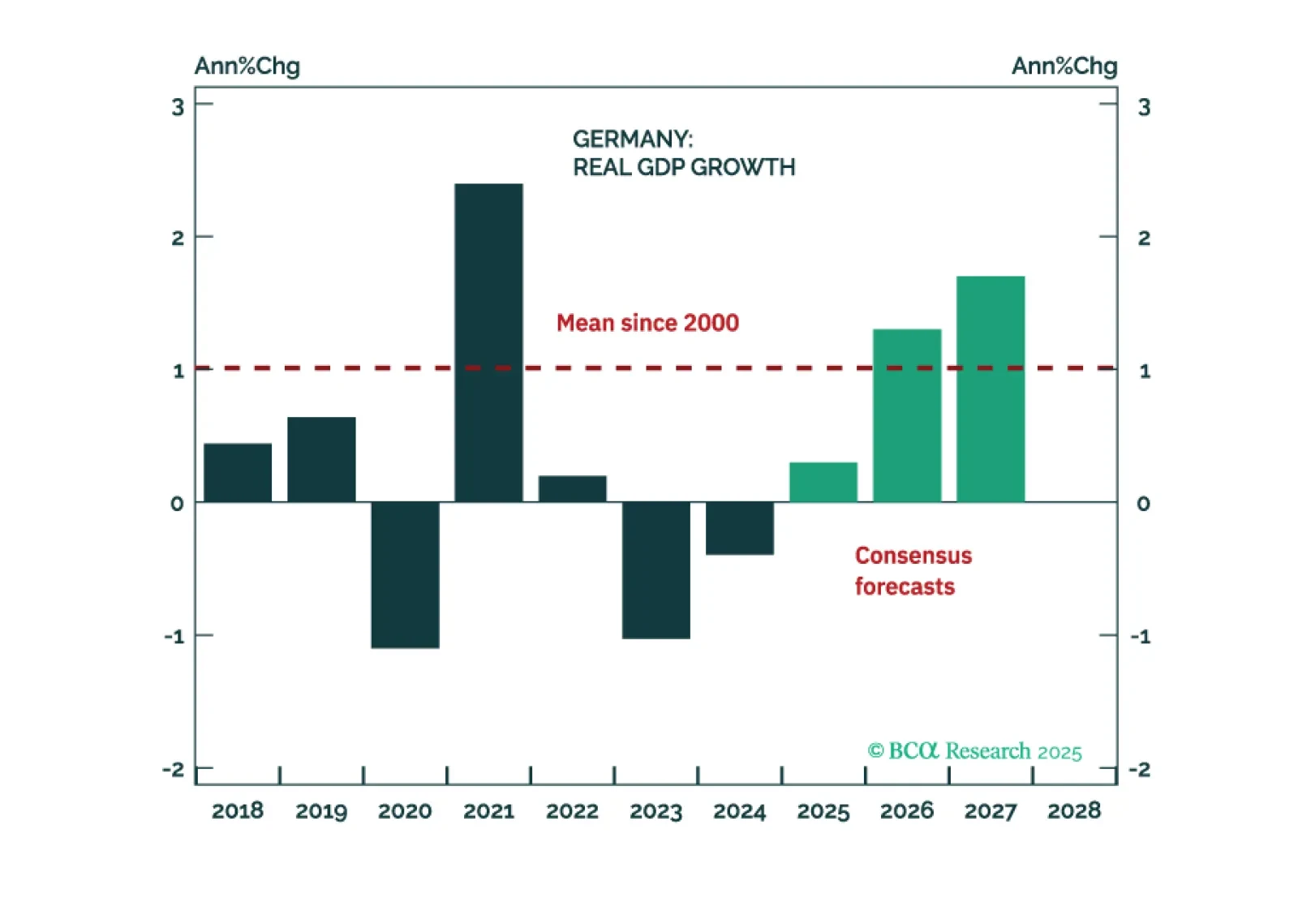

Germany’s economy is regaining momentum after nearly two years of recession. Despite the ongoing cyclical rebound and fiscal stimulus, political gridlock and deep-seated structural challenges threaten to limit the country’s long-term growth potential. Investors should be underweight German Bunds and favor Eurozone equities over German equities.

In this Q4 Strategy Outlook, we discuss where we stand on our recession call, the outlook for stocks and bonds in various scenarios, why investors are misunderstanding the impact of AI on corporate profits, whether the US dollar has entered a structural downtrend, our perspective on the yen, gold and other commodities, and much more.