Global

The equity bull market is getting long in the tooth. Bonds should perform well once economic growth begins to slow. The dollar will strengthen over the coming months before resuming its downtrend. While crude has likely found a near-term floor, we favor metals over energy in the long run.

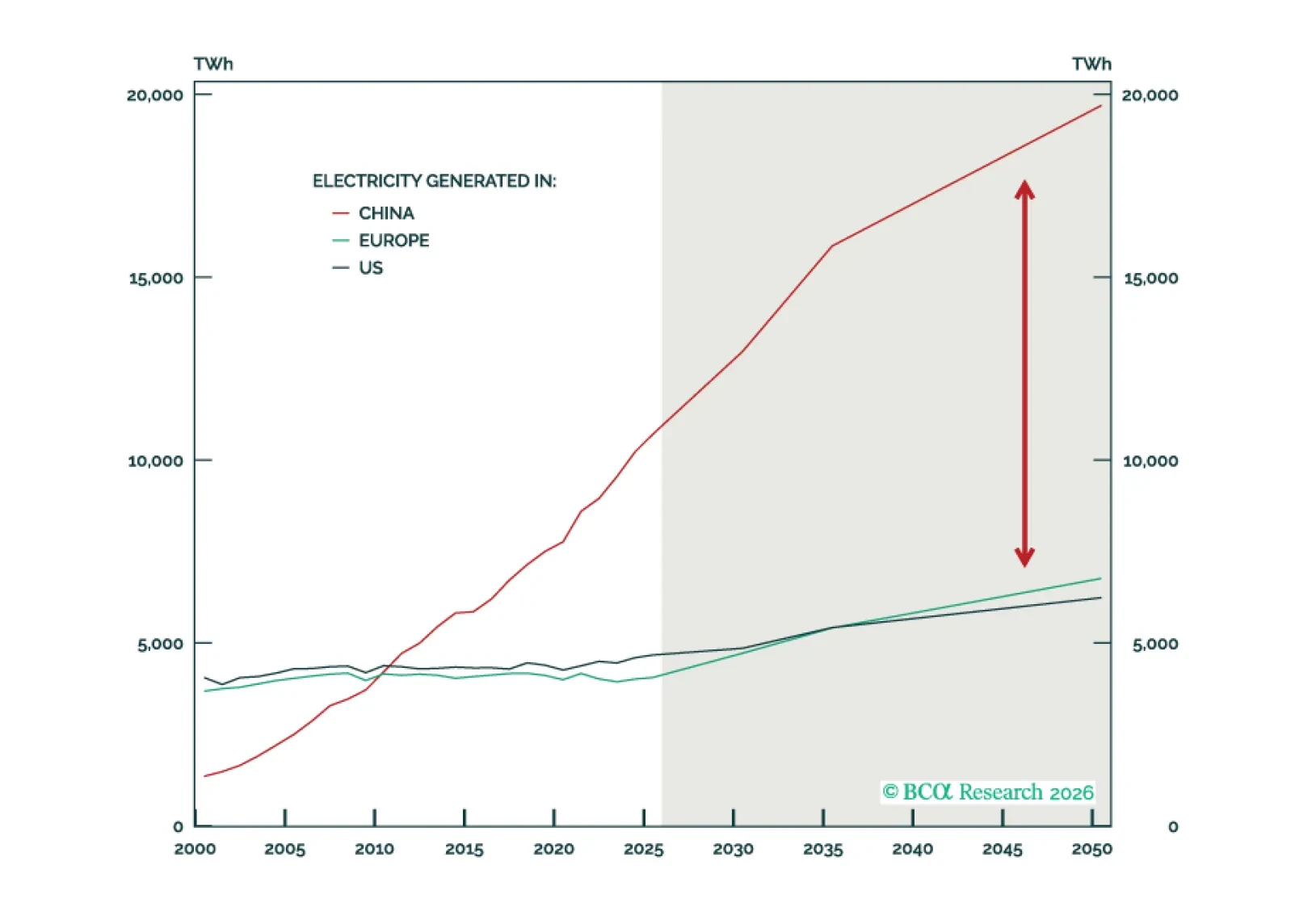

China holds a structural advantage in this "Age of Electricity" by operating the world's largest electricity system. However, this advantage has inherent limits, and the US remains competitive despite its challenges.

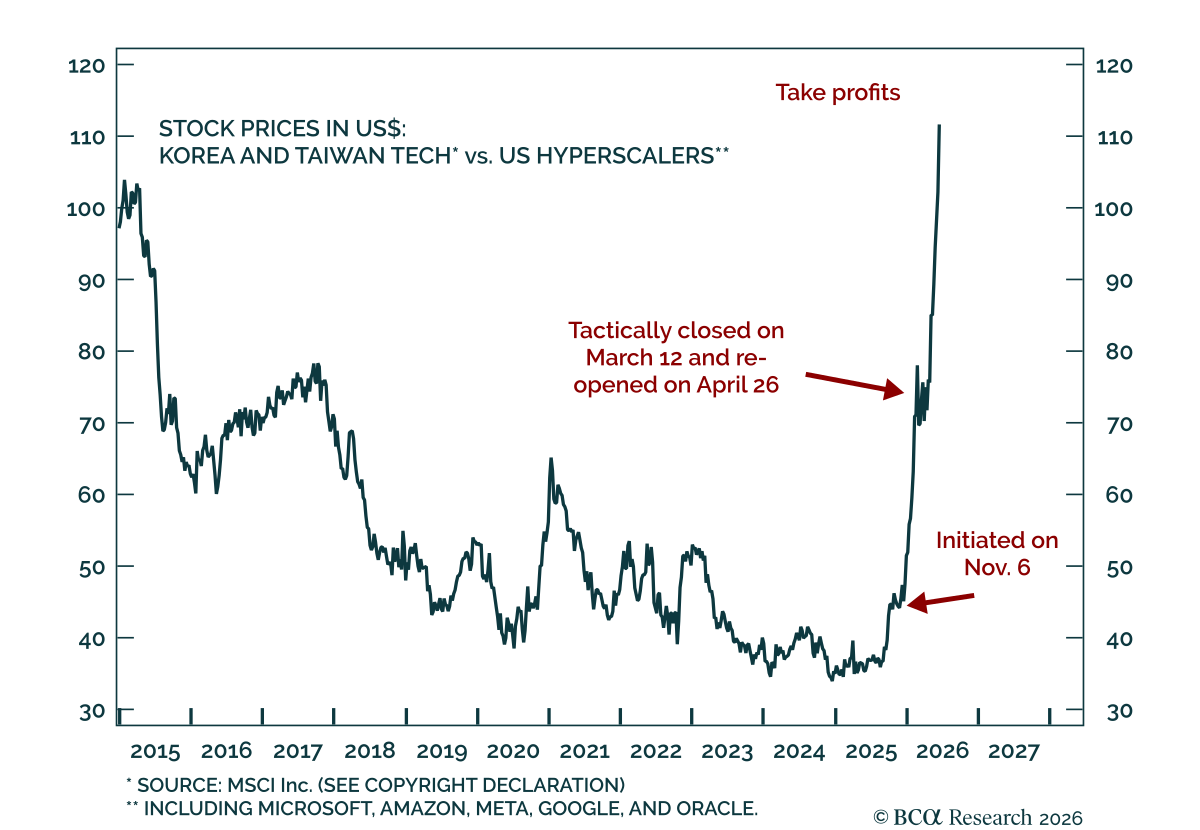

The magnitude of US tech/AI capital spending already rivals past bubble thresholds, threatening hyperscalers’ future returns on capital. There are echoes of previous market tops. Our preferred overlay strategy for equity portfolios remains long semiconductor producers / short hyperscalers.

Downgrade global and US portfolio duration from “above benchmark” to “at benchmark” as the risk of hawkish monetary policy surprises is rising.

Tech companies have historically generated profits from three main sources: 1) economies of scale; 2) network effects; and 3) proprietary technologies. AI threatens to undercut all three sources.

We spent last week meeting investors in Switzerland. This Strategy Insight revisits the most prominent topics we discussed, including repatriation fears, SNB intervention, and Dutch pension reform.