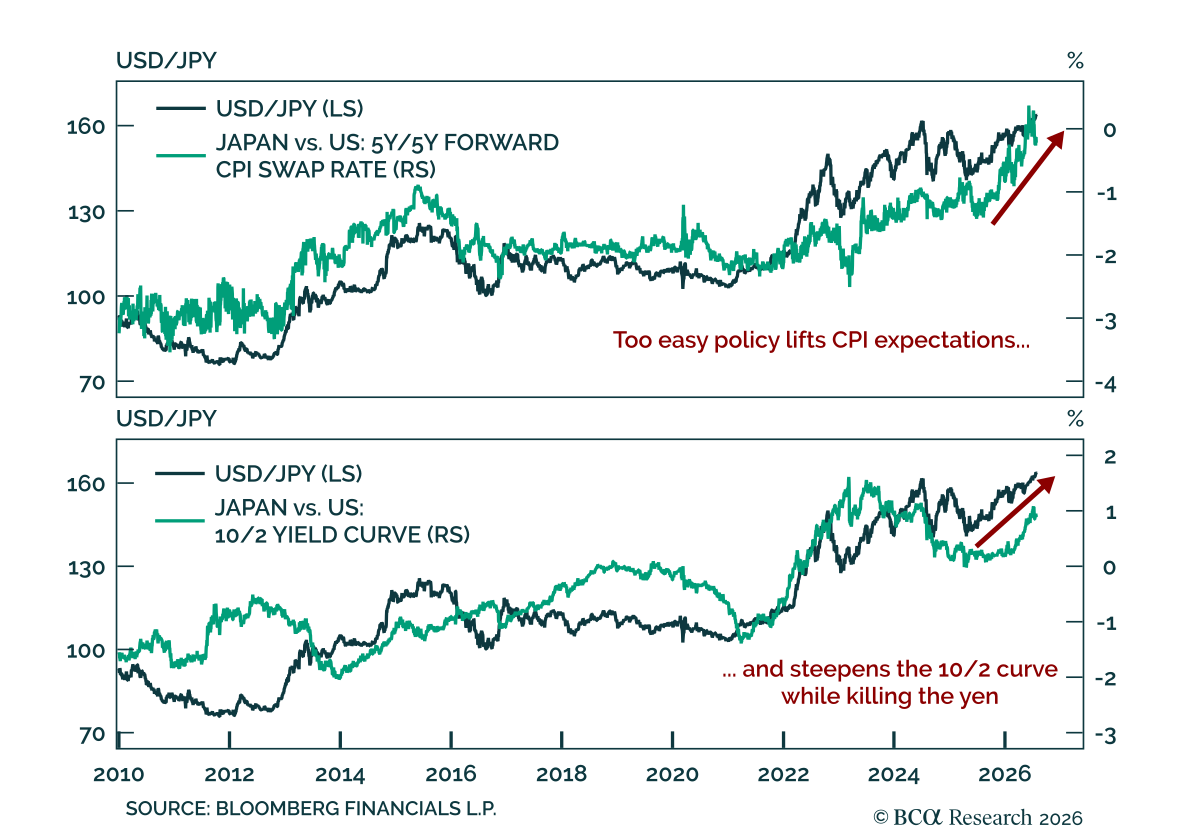

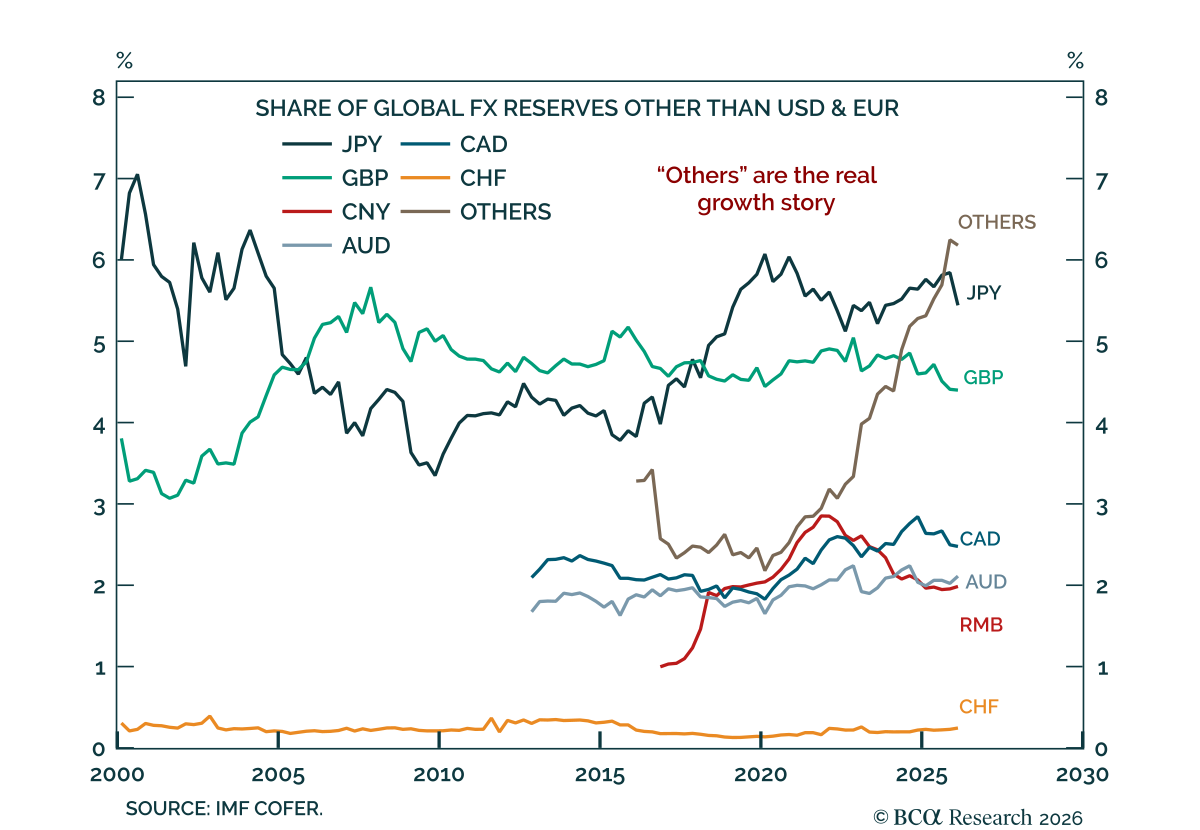

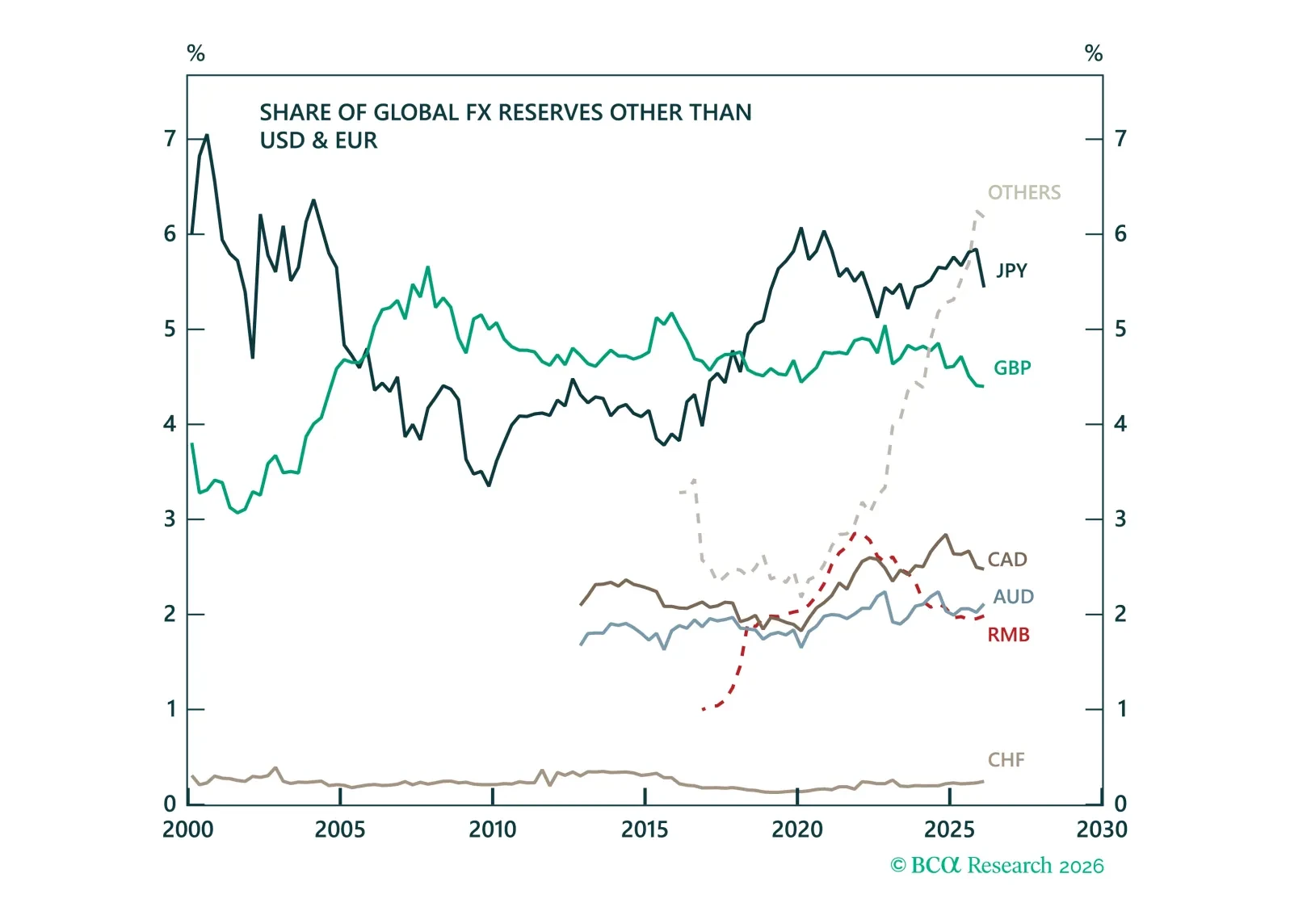

Currencies

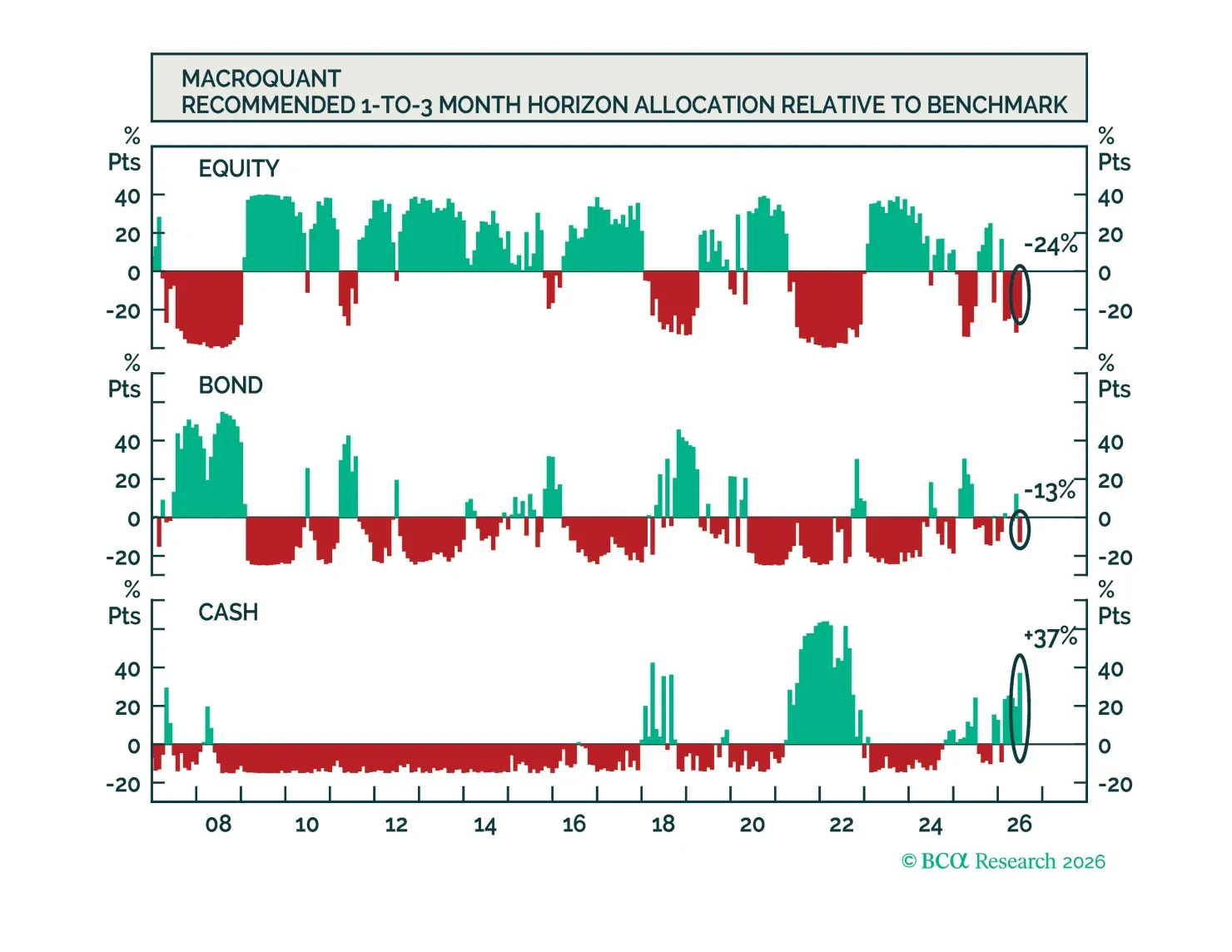

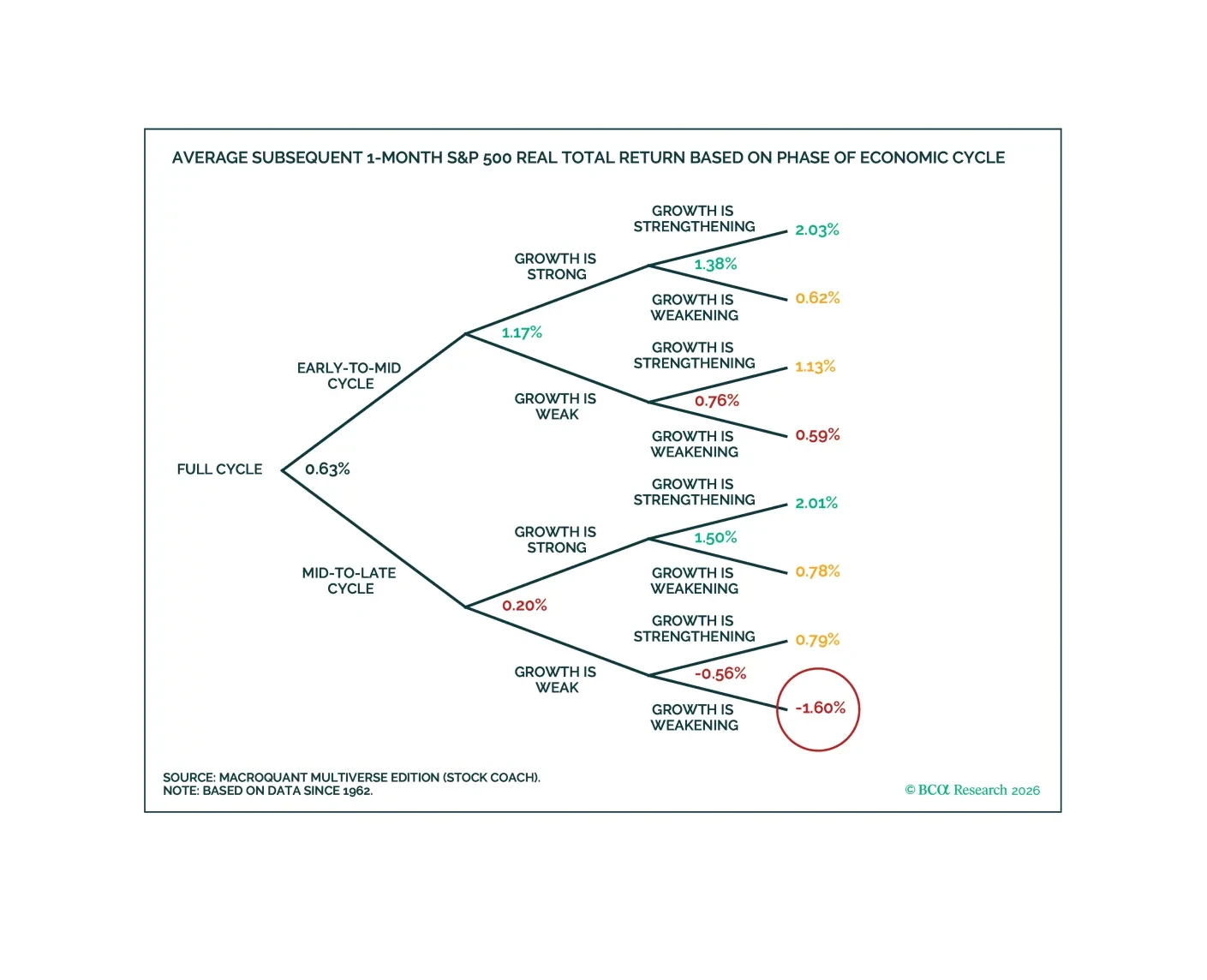

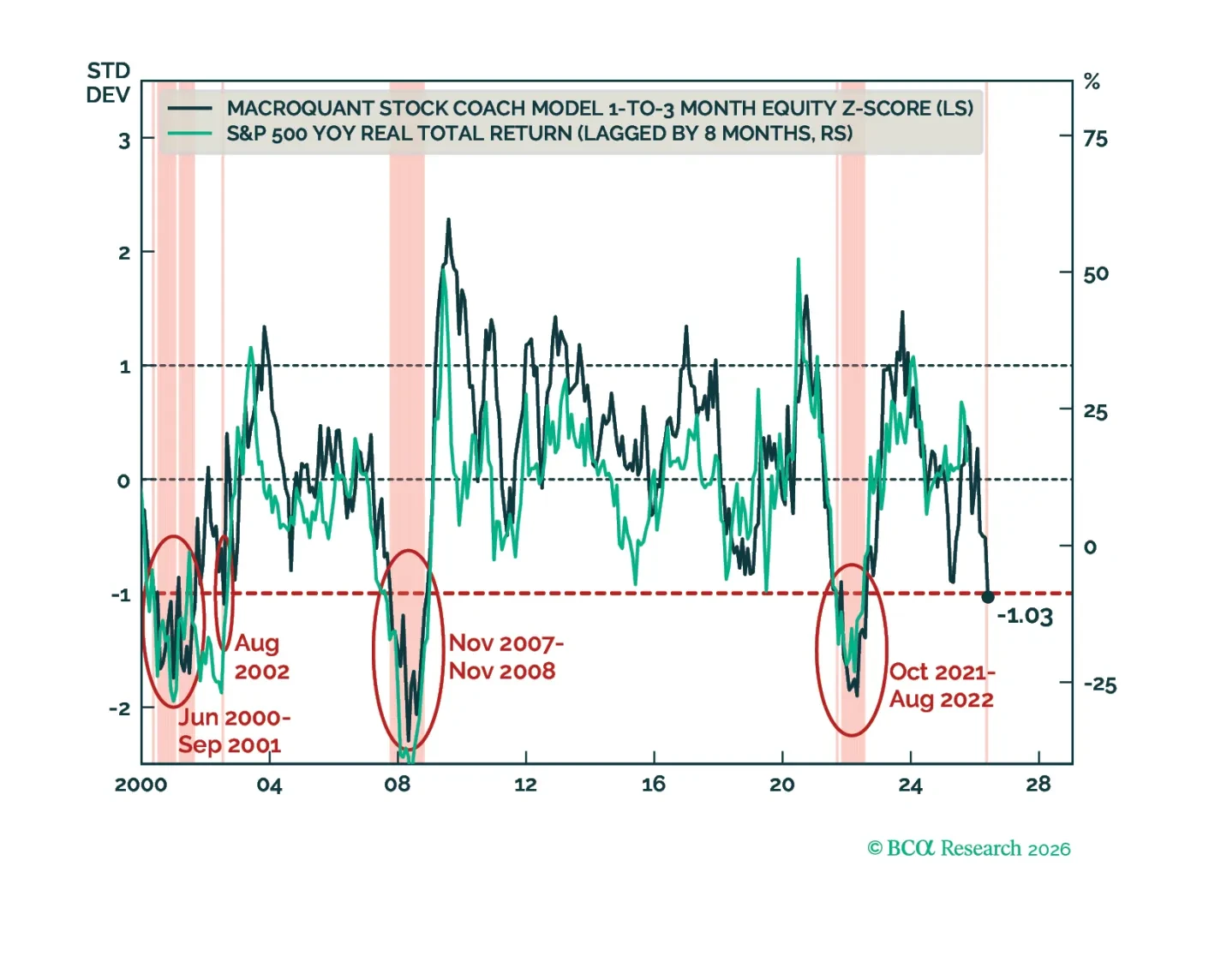

MacroQuant recommends a slight underweight position in equities, and favors a below-benchmark duration stance in fixed-income portfolios. The model is very positive on the US dollar, neutral on gold, constructive on copper, and very bullish on oil.

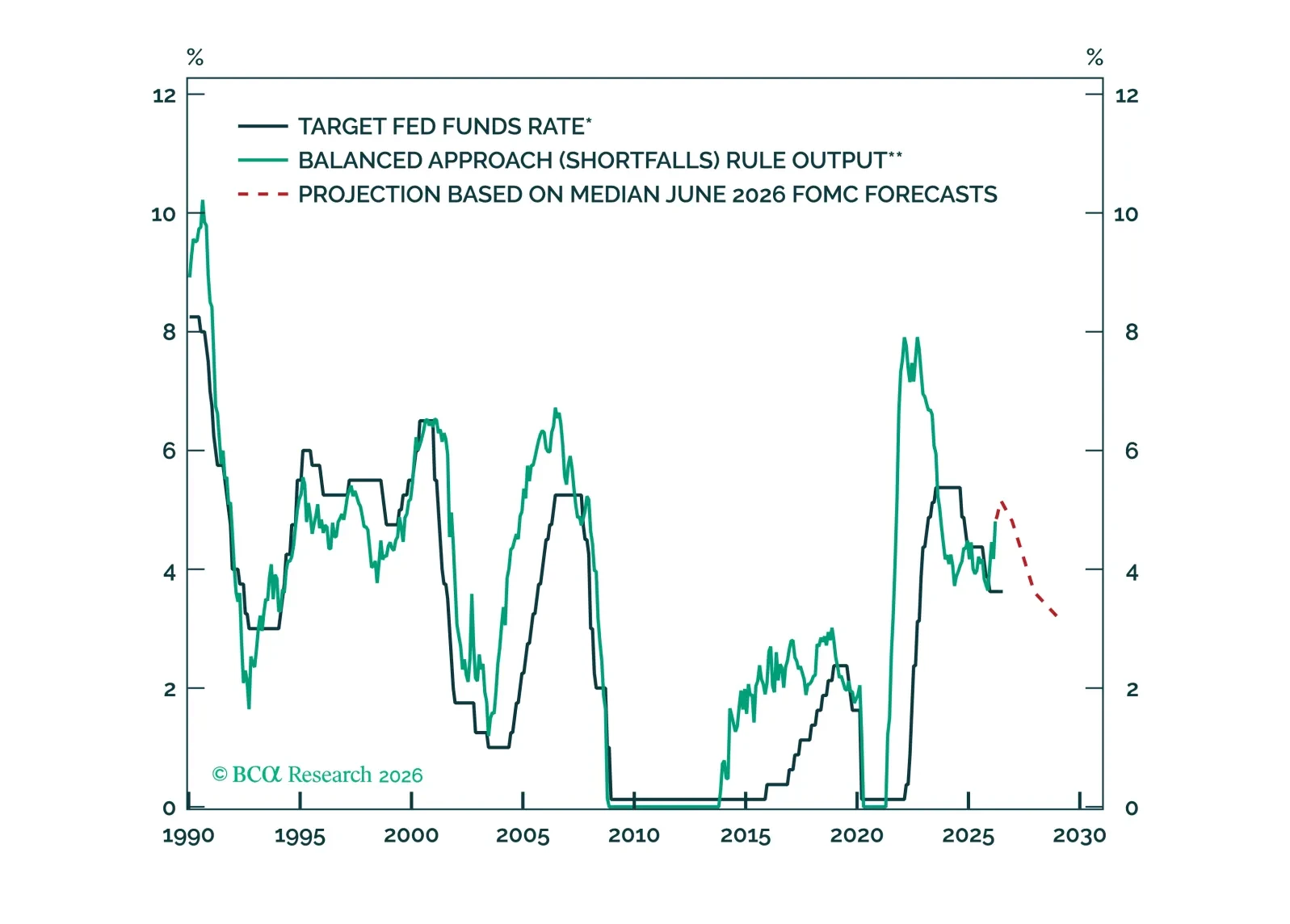

Goldilocks, with fault lines underneath. Our first joint FICC outlook lays out where growth, inflation, and policy are headed this quarter and where the calm could crack.

The dollar is not being replaced by a single rival, it is being diluted by a rising cast of “other” reserve currencies. This report identifies the hidden winners of reserve diversification and why they may matter more than investors think.

MacroQuant recommends underweighting equities and adopting a benchmark duration stance in fixed-income portfolios. The model is very positive on the US dollar, bearish on gold, neutral on copper, and bullish on oil.

The equity bull market is getting long in the tooth. Bonds should perform well once economic growth begins to slow. The dollar will strengthen over the coming months before resuming its downtrend. While crude has likely found a near-term floor, we favor metals over energy in the long run.

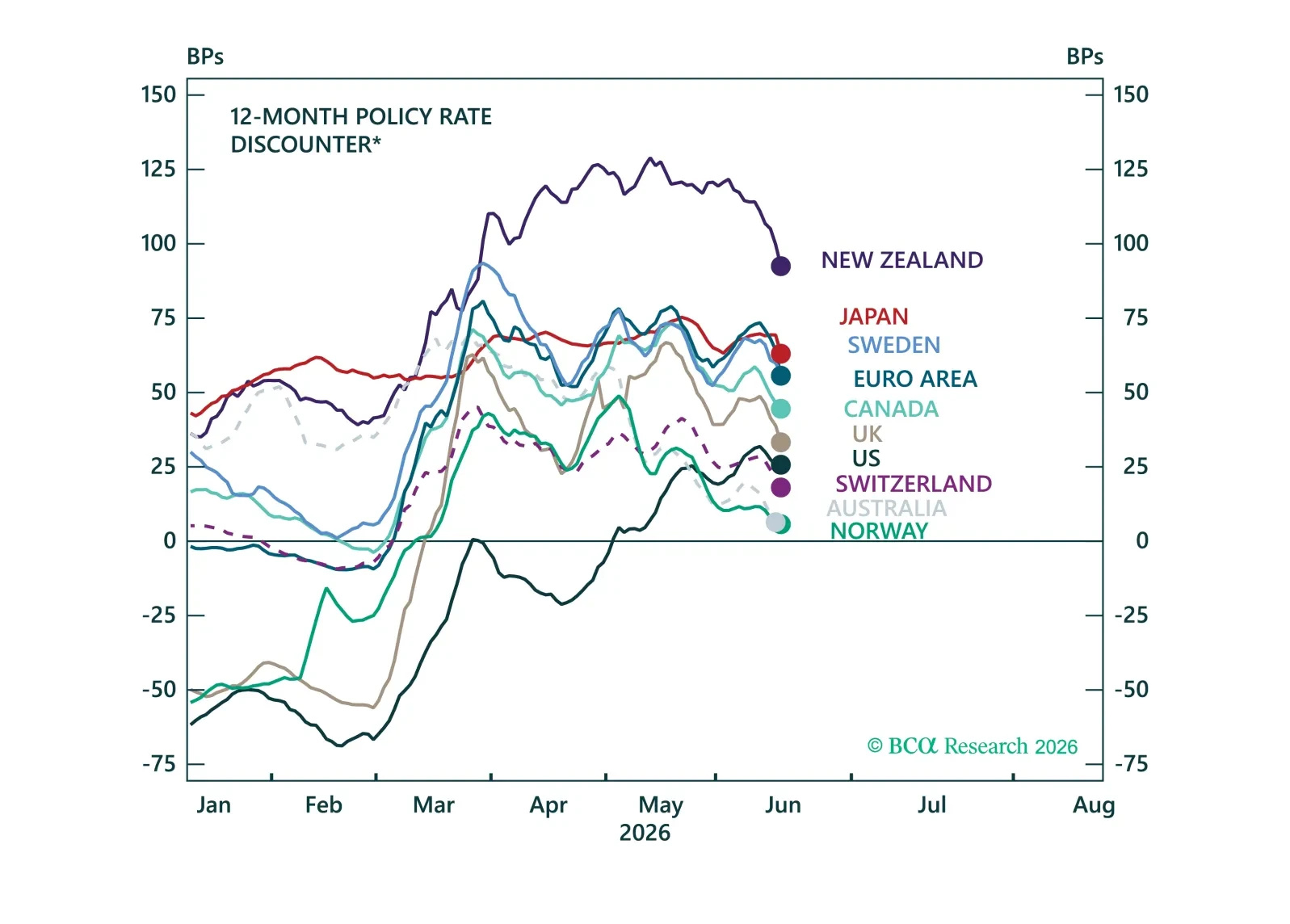

We react to DM central bank meetings this week and highlight the opportunities emerging across global fixed income and currency markets.